Zinger Key Points

- Volatility returns as investors navigate Israel-Hamas conflict, Powell's remarks.

- Rising bond yields led to declines in major stock indices, with the SPY down 2.3% and QQQ down 3% for the week.

- 9 Out of the Last 10 Summers this "Power Pattern" Delivered Winners - Get The Details Now.

Volatility notably returned to the markets this week as investors navigated the escalating conflict between Israel and Hamas, remarks from Federal Reserve Chair Jerome Powell and mixed earning reports from leading U.S. corporations.

Powell Says Fed Can Proceed ‘Carefully,’ Warns Of Further Hikes If Data Remains Strong: During an event organized by the Economic Club of New York, Fed Chair Jerome Powell emphasized the need for a "careful" approach by the Federal Reserve that considers economic data. He also hinted that if the economy’s strength and inflation resurgence continue to surprise, further interest rate hikes may be on the horizon. It was a week marked by significant volatility in Treasuries, with yields reaching 5% on 10-year bonds.

Rising bond yields pressured major stock indices, with the SPDR S&P 500 ETF Trust SPY down 2.3% and the tech-heavy Invesco QQQ Trust QQQ down 3% for the week.

Among sectors, only the Energy Select Sector SPDR Fund XLE and the Consumer Staples Select Sector SPDR Fund XLP have remained unscathed, showing marginal gains.

US Retail Sales Continue To Surpass Expectations, Defying Inflation, Interest Rates: In September, U.S. retail sales marked the sixth consecutive month of increases, underscoring consumers’ remarkable resilience despite rising inflation and higher interest rates. On an annual basis, retail sales surged by 3.8%, up from the upwardly revised 2.9% recorded in August, marking the most substantial year-over-year gain since February 2023.

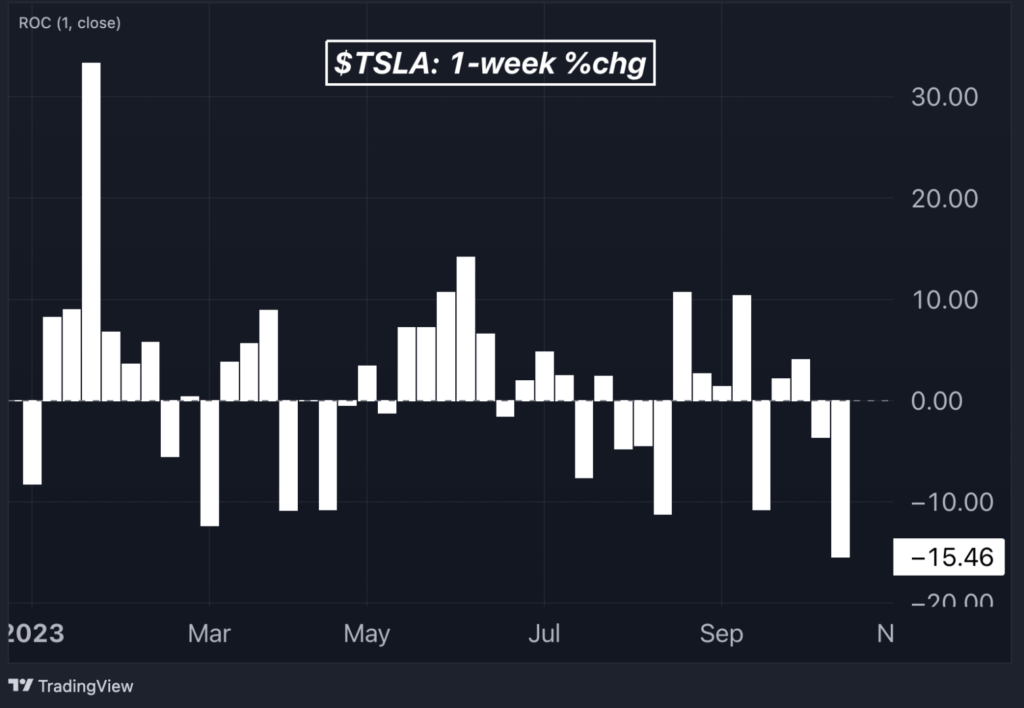

Tesla Reports Lower-Than-Expected Q3 Results, Stock Faces Worst Week Of 2023: Tesla Inc. TSLA reported third-quarter earnings and revenue below expectations. Revenue reached $23.35 billion, a 9% increase from the previous year but falling short of the Street’s $24.38-billion estimate. Adjusted earnings per share came in at 66 cents, also missing predictions. The company announced plans to commence deliveries of the new Cybertruck in November. Tesla’s stock experienced a 15.2% decline for the week, marking its worst weekly performance this year.

Today's Best Finance Deals

Chart: Tesla Faces Worst Weekly Performance In 2023

Netflix Surpasses Expectations With Q3 Report: Netflix Inc. NFLX achieved a remarkable earnings and revenue beat in the third quarter, reporting earnings of $3.73 per share compared to the expected $3.49. As a result, Netflix shares saw double-digit gains for the week, making it one of the S&P 500’s top weekly performers.

Gold Attracts Haven Demand, Miners Outshine Other Sectors: Gold has emerged as one of the top-performing assets since the onset of the conflict in Israel, with the SPDR Gold Trust ETF GLD showing a nearly 10% increase, solidifying its position as a safe haven investment. Silver has also risen in harmony. Among equities, gold mining stocks, as tracked by the VanEck Gold Miners ETF GDX have outshone all other industries, capitalizing on the surge in precious metal prices.

What To Watch In The Week Ahead: On Thursday, the highly anticipated GDP data for the third quarter will be released, with economists predicting a robust 4.1% annualized growth rate. Friday will bring the release of the Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditure (PCE) index, for September. The headline PCE index is expected to show a decline from 3.7% year-on-year to 3.6%.

Upcoming Corporate Earnings to Watch: Tuesday features a lineup of major companies including Microsoft Corporation MSFT, Alphabet Inc. GOOGL GOOG, Visa Inc. V, The Coca-Cola Company KO, Danaher Corporation DHR, Texas Instruments Incorporated TXN, Verizon Communications Inc. VZ, General Electric Company GE and Raytheon Technologies Corporation RTX.

Wednesday will bring earnings reports from Meta Platforms, Inc. FB, Thermo Fisher Scientific Inc. TMO, T-Mobile US, Inc. TMUS, International Business Machines Corporation IBM, ServiceNow, Inc. NOW, The Boeing Company BA, Automatic Data Processing, Inc. ADP and CME Group Inc. CME.

Thursday includes Amazon.com, Inc. AMZN, Mastercard Incorporated MA, Merck & Co., Inc. MRK, Comcast Corporation CMCSA, Intel Corporation INTC, Caterpillar Inc. CAT, United Parcel Service, Inc. UPS, Honeywell International Inc. HON and Bristol-Myers Squibb Company BMY.

Friday will wrap up the week with reports from Exxon Mobil Corporation XOM, Chevron Corporation CVX and AbbVie Inc. ABBV.

Now read: Hamas Releases 2 American Hostages Amid Escalating Tensions: Calls For Ceasefire Grow

Photo via Shutterstock.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.