(Wednesday Market Open) The June Consumer Price Index (CPI) came in much hotter than expected, and equity index futures tumbled before the open.

Potential Market Movers

Analysts were forecasting a month-over-month (MOM) CPI increase of 1.1% and got 1.3%. The year-over-year (YOY) forecast was 8.8% but arrived at 9.1%. After removing food and energy prices, monthly core inflation was also a hotter-than-expected 0.7% MOM and 5.9% YOY, above respective forecasts of 0.6% and 5.7%.

In the past, analysts and investors focused on core inflation because of the volatility of food and energy prices. However, the Federal Reserve’s recent comments indicate that ignoring headline CPI could come at your own peril. Remember, during the June interest rate announcement, Fed Chairman Jerome Powell said that the Fed was focused on all inflation numbers and, especially food and energy. It’s a wider view.

Investors are trying to determine if the Fed will change its rate-hiking plans later in the month. As of this morning, the CME FedWatch Tool increased its probability of a 75-basis-point hike in July to 58.4% with a 41.6% chance of a 100-basis-point hike.

The 2-year Treasury yield, which tends to be most tied to the fed funds rate, jumped to 3.19% this morning while the 10-year Treasury yield (TNX) moved up to 3.049%—driving an even larger inversion between the 2s10s spread. These new CPI numbers put the Fed in an even bigger pickle as the central bank weighs its next rate hike. Any increase they make would likely drive the 2-year yield higher, widening the inversion in the yield curve and increasing the likelihood of recession.

At the open, investors appeared disappointed in their search for signs that inflation had finally reached a peak. The Cboe Market Volatility Index (VIX) rose more than 3.7% and is back above 28.

Adding insult to injury, a few early earnings announcements this morning were few misses. Industrial and construction supplier Fastenal (FAST) missed on revenue but beat on earnings and slid more than 6% in premarket trading. The company saw sales increase due to price increases in the first quarter but cited “significant inflation” and cited supply chain problems as reasons for its rising inventory costs.

Delta Air Lines (DAL) hit on revenue but missed on earnings, prompting it to slide 3.47% ahead of the opening bell. DAL struggled to overcome rising fuel, labor, and re-booking costs, but issued a positive outlook, saying that there’s a lot of “pent-up demand” for travel.

Two of the biggest banks in the country, JPMorgan Chase (JPM) and Morgan Stanley (MS), will report earnings tomorrow. Investors will be looking for how much money banks will be setting aside for loan losses. According to FactSet, banks set aside a significant amount for potential loan defaults in 2020 but reduced those amounts through 2021. However, in Q1 2022 they started increasing provisional money for loan losses once again. While provisional loan loss money doesn’t hurt revenues, FactSet data shows an inverse relationship between the amount of money set aside for loan losses and bank earnings.

Provisional loan losses could also provide insight into how banks view the housing market. The Mortgage Bankers Association of America reported this morning that the number of mortgage applications fell again last week. CNBC also reported that the demand for big mortgages is decreasing, noting that the average mortgage in June was $415,000 which is significantly lower than the record set back in March of $460,000.

However, the supply chain may be getting a big boost as China reported a big increase overnight in its June trade surplus of $97.9 billion. Exports picked up as Shanghai reopened and shippers were able to move their backlog of cargo. However, Shanghai residents are expressing concern and bulk- buying supplies, according to Bloomberg. And recent double-digit growth in COVID-19 cases in the city is fanning fear that the city could lock down again.

Meanwhile, new data indicates the Chinese economy appears to be weaker as imports into the country rose only 1%, reflecting low Chinese consumer demand.

Reviewing the Market Minutes

Despite flirting with positive territory several times throughout the day, the major indexes all closed lower yesterday. The Nasdaq ($COMP), S&P 500 (SPX), and the Dow Jones Industrials ($DJI) respectively fell 0.95%, 0.92%, and 0.62%. Mega-cap stocks were a drag on the major indexes as the CRSP U.S. Mega-Cap Index dropped 1% on the day and 2.37% over the last three days.

Investors appeared cautious ahead of the today’s CPI report with many turning to the safety of bonds and pushing prices higher. The 10-year Treasury yield (TNX) finished lower at 2.95%.

All sectors closed in the red with energy at the bottom of the heap. The Energy Select Sector Index fell 2.05% pressured by plummeting oil prices. The WTI crude oil, natural gas, and unleaded gasoline futures all settled lower falling 8%, 4.6%, and 5.9% respectively. The moves may be a good sign for inflation, but many see it as a sign the market is still anticipating a recession.

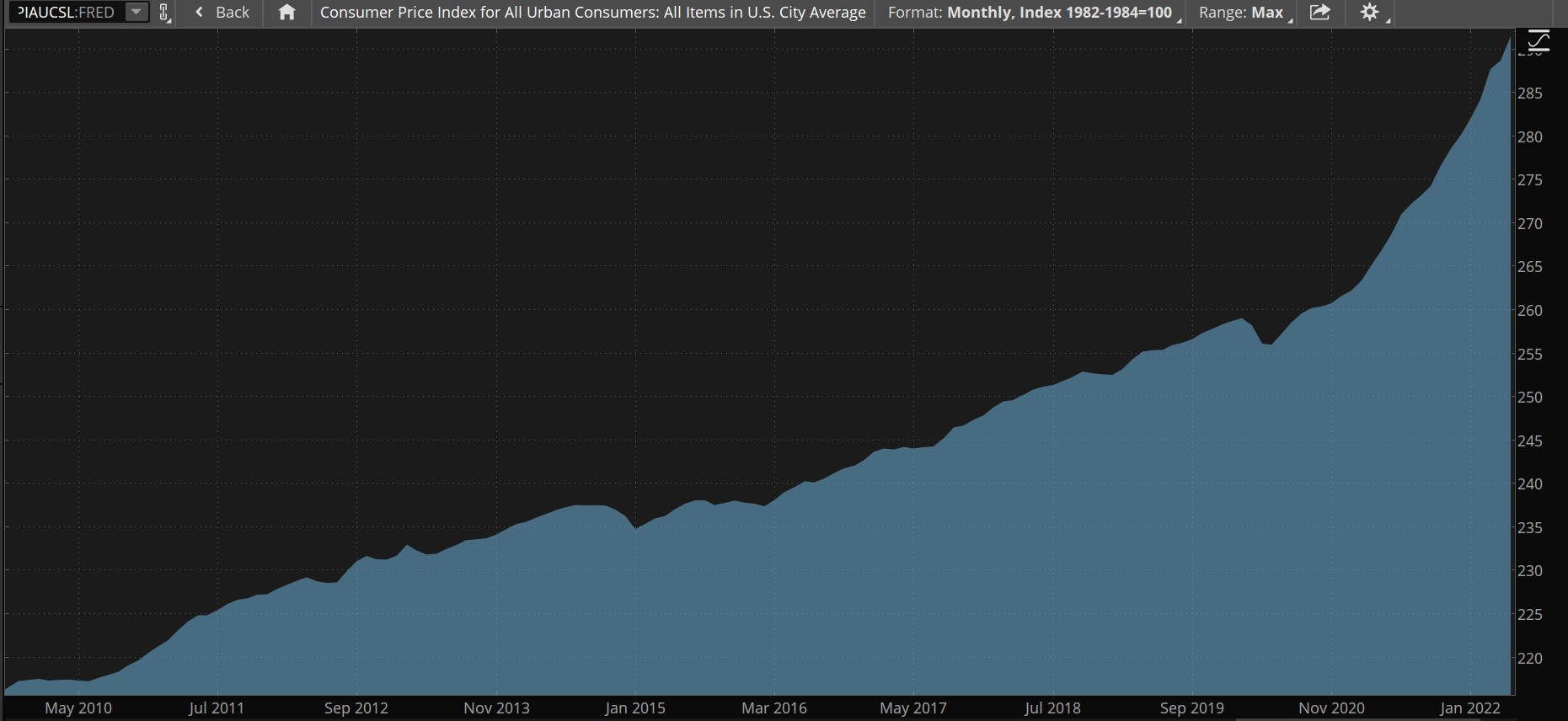

CHART OF THE DAY: EXPONENTIALLY EXPENSIVE. The Consumer Price Index for all urban consumers for all items FRED went from a relatively linear projection to almost parabolic from the start of 2021. This graph doesn’t include today’s data. FRED® is a registered trademark of the Federal Reserve Bank of St. Louis. The Federal Reserve Bank of St. Louis does not sponsor or endorse and is not affiliated with TD Ameritrade. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Inflation Origination: People and economists have studied inflation for hundreds of years. In the 16th century, Spanish theologian Martin de Azpilcueta observed that when Spanish ships returned from the New World with gold, the price of goods and services rose in Spain more than France, which hadn’t seen a similar influx of precious metals. The economist Milton Friedman explained, “Inflation is always and everywhere a monetary phenomenon…”

All prices are a function of supply and demand—even the price of money. An increase in the supply of money makes existing money worth less, which creates price inflation. Price inflation as measured by the CPI is almost always rising, just not always at the same rate. In 2020 and 2021, the Fed and Congress greatly expanded the money supply through lower rates and increased borrowing due to the pandemic.

As it usually does, the increased money supply caught those who sell goods off-guard. Unfortunately, many companies weren’t able to ramp up production to meet the new demand because of COVID-19 restrictions and a worker shortage made price inflation even worse. So, the impact of all that money in the system has led to CPI rising at a near exponential rate over the last 18 months.

Banking on Bonds: Bank of America (BAC) reported that a net $7.8 billion moved into bond funds last week creating the largest inflow in two months. With the Fed pulling out of the Treasury and mortgage-back securities markets, the new trend could provide some much-needed liquidity for bonds.

The move reflects at least two developments. First, the rate of return on bonds is now high enough that investors find them appealing—or at least more appealing than other investments. Second, investors are also concerned about the state of the U.S. and global economies and are looking for more secure investments to protect their assets.

Slippery Slope: The International Energy Agency (IEA) is warning that the energy crisis isn’t over. The IEA said that the Russia-Ukraine war hasn’t affected the supply of oil much but with the 27-nation European Union pledging to phase out 90% of Russian oil imports by the end of the year, things could get tough—particularly for Europeans who get 60% of their oil from Russia.

Higher energy prices are another factor pushing Europe towards recession.

Notable Calendar Items

July 14: Producer Price Index (PPI) and earnings from Taiwan Semiconductor TSM, JPMorgan Chase JPM, Morgan Stanley MS, Cintas CTAS, and ConAgra CAG

July 15: Retail sales, preliminary University of Michigan consumer sentiment, and earnings from UnitedHealth UNH, Wells Fargo WFC, BlackRock BLK, Citigroup C, and U.S. Bank USB.

July 18: Earnings from Bank of America BAC, IBM IBM, and Goldman Sachs GS

July 19: Building permits, Housing starts, and earnings from Johnson & Johnson JNJ, Lockheed Martin LMT, Netflix NFLX, Haliburton HAL, JB Hunt JBHT, and Hasbro HAS

July 20: Existing home sales and earnings from Tesla TSLA, Abbott Labs ABT, Kinder Morgan KMI, Biogen BIIB, and Baker Hughes BKR

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.