While equity index futures are still pointing to a lower open on Wednesday, they did trim some losses after the ADP Nonfarm Employment report showed strong gains in December. More than twice as many workers as expected found jobs last month, particularly in leisure and hospitality, trade, transportation, and utilities. Much of these gains may have occurred before the Omicron variant really hit the scene so we’ll have to wait and see if they stick.

Later today, the FOMC Meeting Minutes will be released and investors will have insight into what the Fed has been discussing, particularly related to tapering and future interest rate hikes.

The Nasdaq-100 Futures (/NQ) are leading the slide on Wednesday once again. The Cboe Nasdaq-100 Volatility Index (VXN)—also known as the Vixen—is the Nasdaq-100 (NDX) equivalent of the VIX (Cboe Market Volatility Index), which is related to the S&P 500 (SPX). The Vixen rose 5.43% on Tuesday as investors sold tech stocks. While this may signal trouble for some tech companies, the fact that the VIX was relatively unchanged could be a good sign for the majority of stocks in the near term.

One company that struggled to grow on Tuesday was Scott’s Miracle-Gro SMG. Scott’s fell 2.79% after providing guidance saying it would maintain its full-year earnings outlook, but its Hawthorne cannabis division expects a 40% decline in sales. The company cited the slowdown in the cannabis market and issues with the supply chain.

The ISM Manufacturing PMI was lower than expected, suggesting that manufacturers are seeing fewer orders. December was the 19th straight month of increases, but the slowdown may actually be a welcomed reprieve because it may provide relief to an already strained supply chain.

The JOLTS report also showed a decrease in job openings in November. The Great Resignation continues as the “quits” rate remained high. In the light of Wednesday’s ADP report, it may be that workers were simply quitting one job to take another job. Friday’s Employment Situation report could provide greater insights to these job market developments.

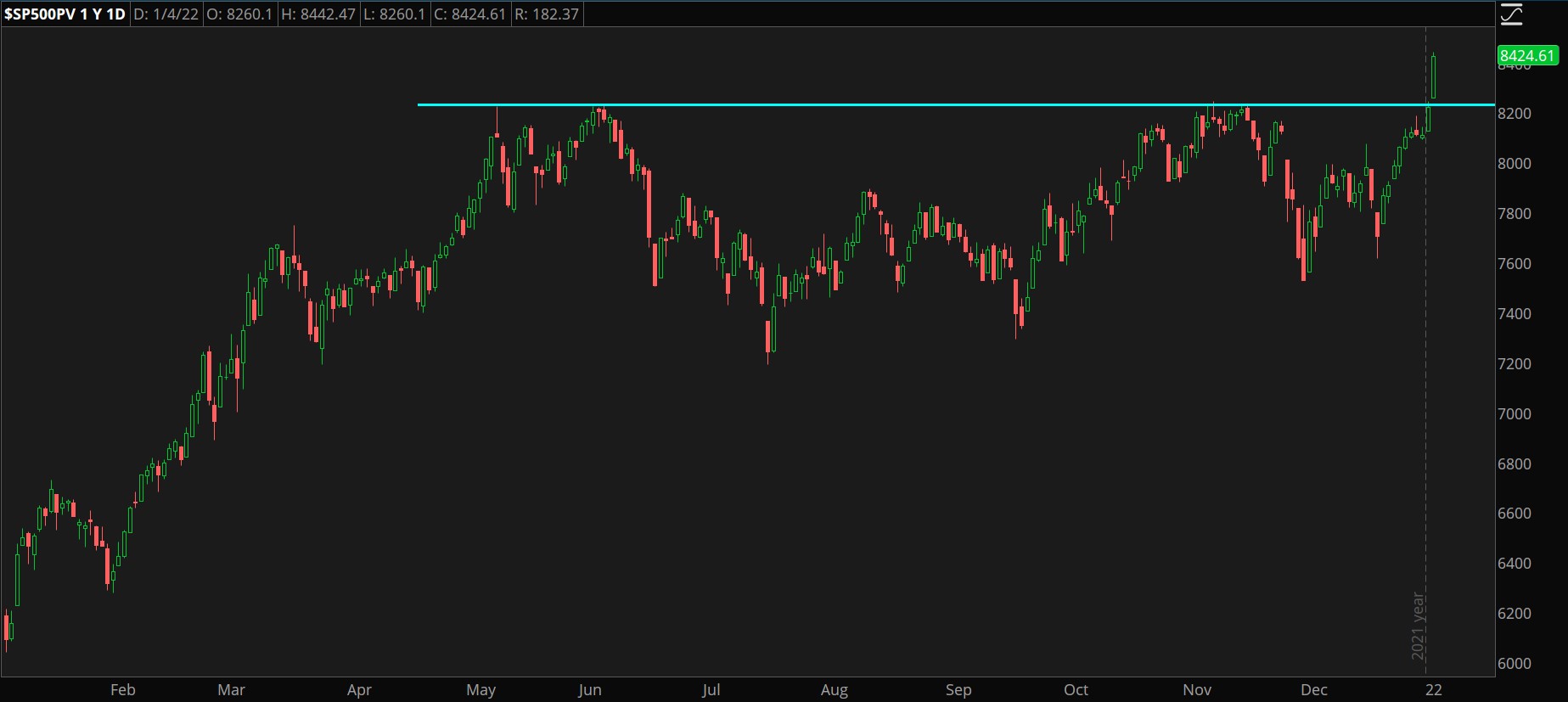

Many stocks turned bearish after the manufacturing and job opening announcements; the S&P 500 (SPX) was positioned for a new all-time high, but it turned negative after the reports came out. Once again, investors were focusing on value stocks prompting the S&P 500 Pure Value Index ($SP500PV) to rally 2.26% on the day.

It was a tale of two cities on Tuesday with investors buying energy stocks and selling technology stocks. Energy stocks led all sectors for the second day in a row, followed by financials and industrials. Caterpillar CAT, Dow DOW, and Chevron CVX were the top performers in the Dow Jones Industrial Average ($DJI), rising 5.35%, 2.71%, and 1.82% respectively.

Vaccine stocks are kicking off the new year in a bad way as Pfizer PFE fell 1.83% on Tuesday creating a two-day losing streak of about 8%. BioNTech BNTX fell 3.35% and has racked up two-day losses of about 12%. Moderna MRNA only fell 0.85% yesterday but has a two-day loss of 9.76%. This seems to reflect an attitude by investors that the pandemic is less of a concern as people are learning to live with the virus.

Tech Heavy

Investors were selling technology stocks with Tesla TSLA and NVIDIA NVDA falling 4.18% and 2.76% respectively. The 10-year Treasury yield (TNX) rose another 2.46% and is testing last year’s highs. The higher yields or interest rates may prompt investors to focus on valuations because higher alternative investment rates with higher safety may become more appealing. The 10-year yield has risen more than 10% in the last three trading days and is up more than 24% from its November low.

The tech-heavy Nasdaq Composite (GIDS) fell 1.33% on Tuesday, while the Technology Select Sector Index ($IXT) was down 1.10%. Chinese tech stocks were hit much harder with Pinduoduo PDD falling 11.19%, JD.com JD decreasing 6.04%, and Baidu BIDU slipping 1.72%.

As investors focus on valuations, they also focus on risk. Last year, China started cracking down on various market sectors, including gaming, real estate, gambling, and more. On Tuesday, Chinese regulators announced plans for a security review of various internet platforms.

CHART OF THE DAY: VA-VA-VALUE. The S&P 500 Pure Value Index ($SP500PV—candlesticks) broke resistance on Tuesday, creating a new 52-week high. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Breaking Bonds: Bond yields may rise for a couple of reasons, like when the Fed increases short-term rates when the Fed stops buying bonds in the open market, and when investors choose to sell bonds in favor of other assets. The Fed hasn’t raised rates yet, but it is tapering its bond-buying programs, which allows yields to rise. However, the recent moves appear to be driven mostly by investors selling bonds.

Investors appear to be selling bonds in favor of value stocks. One reason investors may be favoring value stocks over bonds is that many of these value stocks have higher-than-average dividend yields. This means many value stocks offer potential price appreciation on top of quarterly dividend income.

Vote of Confidence: Many investors buy bonds as part of a well-allocated and diversified portfolio. They’ll often buy bonds when they’re bearish on stocks or if they’re uncertain about the economy. The recent selling of bonds could be seen as a vote of confidence for stocks and the economy. Of course, there’s still the influence of the Fed and pushing rates higher later in the year. Many investors may be looking to sell bonds before rising rates push bond prices lower. But it’s helpful to remember that the Fed is talking about raising rates because of the strength of the economy.

Stock Selection: A problem that might come with value investing is that it takes some analysis. In my January Outlook, I pointed out that if 2022 is the year of value investing, it could also be the year of the active manager. This is because investors may not find the same kind of success with index investing as they’ve seen in the past because some indices have become overweight in a few stocks, and if those stocks lose popularity, they could be a major drag on the index.

According to Yardeni Research, as of December 10, FAANGM stocks, which include Facebook, now Meta FB, Amazon AMZN, Apple AAPL, Netflix NFLX, Google, now Alphabet GOOGL, and Microsoft MSFT, had a combined market cap of $10.4 trillion and accounted for 22.4% of the S&P 500. From 2013 to December 10, 2022, the FAANGM stocks have grown 814.5%, whereas the S&P 500 without the FAANGM stocks only grew 167.1%. What all this data means is that a great portion of the S&P 500’s performance is based on just six stocks. If investors continue to shift from growth to value, the S&P 500 could suffer unless the other 494 stocks can offset the potential losses in the six FAANGM stocks.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

The preceding post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga. Although the piece is not and should not be construed as editorial content, the sponsored content team works to ensure that any and all information contained within is true and accurate to the best of their knowledge and research. The content was purely for informational purposes only and not intended to be investing advice.

Image Sourced from Pixabay

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.