The banking system is wobbly this morning. Regional banks were down yesterday and are down AGAIN pre-market this morning. Meanwhile, the FED is going to raise rates today.

What could go wrong?

Market

Prices as of 4 pm EST, 5/2/23

Macro

House Democrats are working to force a vote on a debt ceiling increase ahead of a potential default on June 1.

-

For the discharge petition to be successful, they would need signatures from the majority of the House.

-

That means Democrats would have to win over some Republicans to bring the bill to the floor.

-

President Biden is set to meet with congressional leaders on May 9.

It’s Fed Day and a 25bps hike looks imminent.

-

Traders are placing a nearly 90% chance on this being the final hike in the most aggressive tightening campaign since the Volcker era.

-

After that, markets expect the Fed to pause and hold

-

With no new dot plot being issued, Powell’s words following the decision will be under the microscope for clues about future policy.

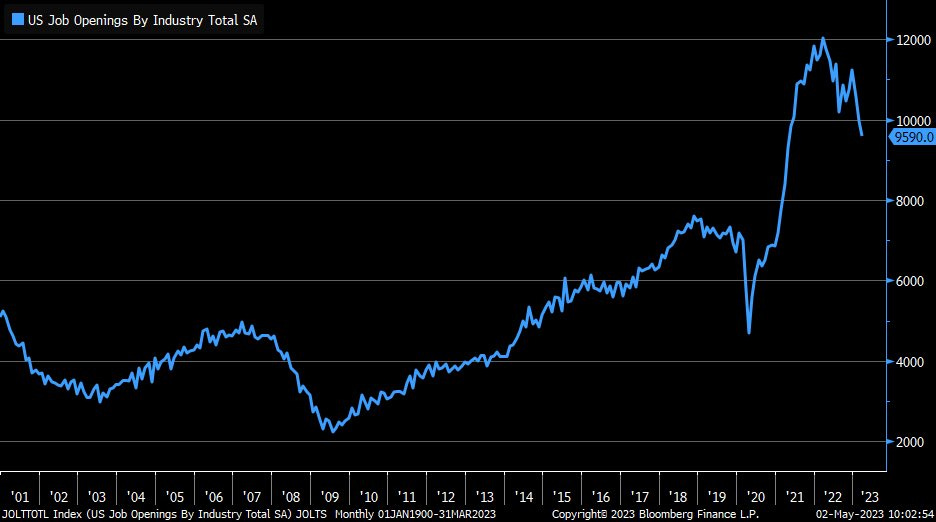

JOLTs data revealed the number of US job openings fell to its lowest in March since April 2021.

-

Vacancies fell below market expectations suggesting the labor market may finally be beginning to normalize.

-

A drop in the number of quits also points to cooling.

-

Openings still remain historically high, however, which means there’s more work to be done on this front.

Stocks

Short seller Hindenburg Research has a new target: Carl Icahn.

-

The firm published a report yesterday alleging Icahn Enterprises was overvalued, held assets at inflated prices, and was vulnerable to Icahn borrowing against shares.

-

The stock suffered its worse day ever, falling 20%.

-

Icahn denied the claims and said the firm’s performance would “speak for itself”.

-

His net worth fell by $10 billion on the day.

After acquiring First Republic, JPMorgan CEO Jamie Dimon said “this part of the crisis is over”.

-

He obviously wasn’t referring to literally every other bank that makes up the KBW Regional Banking Index.

-

The index extended its 2023 lows yesterday as PacWest and Western Alliance led the way with drops of more than 27% and 15%, respectively.

Energy

The biggest production changes to OPEC output in April were unintentional.

-

Production dropped by 310,000 barrels per day thanks to a pipeline suspension in Iraq and a labor strike in Nigeria.

-

Even so, the decline in output isn’t doing much to buoy oil prices: Brent crude fell below $75 a barrel for the first time since March (which was before OPEC+’s surprise cut).

Earnings

Here are some of yesterday’s highlights:

Advanced Micro Devices AMD: $0.60 EPS (vs. $0.56 expected), $5.35 billion in sales (vs. $5.3B expected).

-

Revenue fell 9% due to a decline in PC chip sales.

-

Forecasted revenue of $5-5.6 billion for Q2 fell short of analysts’ expectations of $5.5 billion.

Ford Motor F: $0.63 EPS (vs. $0.41 expected), $39.09 billion in sales (vs. $36.08B expected).

-

Better-than-expected results from fleet and legacy operations outweighed losses from its EV division (which are expected to continue).

-

Reiterated guidance of adjusted earnings between $9-11 billion for 2023.

What we’re watching today:

-

Qualcomm QCOM

-

CVS Health CVS

-

Estee Lauder EL

-

Equinix EQIX

-

Mercadolibre MELI

-

Public Storage PSA

-

Emerson Electric EMR

-

Kraft Heinz KHC

-

Metlife MET

-

Philips 66 PSX

-

Corteva CTVA

-

Trane Technologies TT

-

Exelon EXC

-

Realty Income O

-

Yum Brands YUM

-

Williams Companies WMB

-

Barrick Gold GOLD

Top Headlines

-

T-Bill yields: Concerns over debt ceiling limitations are being reflected in the short end of the yield curve.

-

SEC vs. fees: Gary Gensler is calling out high fees charged by private equity and hedge funds.

-

Another chatbot: The co-founders of Google DeepMind and LinkedIn have launched their own AI chatbot, called Pi.

-

Banker warning: A top banking CEO is predicting more US regional banks will need rescuing.

-

EM shorts: The China-heavy Vanguard FTSE Emerging Markets ETF is at its most shorted in over a year.

-

DeSantis vs. DIS: Florida has sued Disney over control of expansion at its Orlando theme park.

-

Housing inventory: According to Black Knight, ~30% fewer new listings hit the market in March compared to pre-pandemic norms.

-

Green copper: Goldman Sachs estimates “green” copper will account for 47% of total demand growth between 2023 and 2040.

Crypto

Prices as of 4 pm EST, 5/2/23

-

Fund outflows: Digital asset investment products saw their second straight week of outflows totaling $72 million last week.

-

Ordinals: The number of NFTs tied to the Bitcoin blockchain surged above 3 million, but most are just text.

-

Unusual depegging: Stablecoin TrueUSD (TUSD) depegged from the dollar…to the upside.

-

Bitcoin transactions: For two days, transactions of tokens on the Bitcoin network have outnumbered that of regular Bitcoin.

-

COIN: Coinbase will launch an international derivatives exchange for institutional investors outside the US.

Deals

-

Fintech: A Peter Thiel-backed SPAC is close to merging with Hong Kong-based fintech firm Hyphen.

-

IPO markets: Chinese IPOs have raised more than 5x as much as their US counterparts in 2023.

-

Untapped gas fields: Saudi Aramco is in separate talks with Sinopec and TotalEnergies to raise ~$10 billion for midstream/downstream projects.

-

AI funding: Generative AI startup Cohere is in talks with Nvidia and Salesforce to raise $250 million at a ~$2 billion valuation.

-

Infrastructure: Space rivals are joining forces to bid on the EU’s $6.6 billion satellite project, IRIS.

Meme Of The Day

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.