The Last Week, In A Nutshell

What Happened: Stocks closed the week lower on an escalation of U.S. and China tensions, mixed reactions to earnings results, and delays in stimulus talks.

Remember This: “Congress’ decision on a new wave of support could make or break the next leg of the economic recovery,” said Lindsey Bell, chief investment strategist for Ally Financial Inc's ALLY Ally Invest.

“With over 16 million people collecting unemployment and businesses unable to open at (or near) capacity, pulling or reducing fiscal support could lead to a deterioration in the economic improvement recently recorded.”

Pictured: Profile chart of the S&P 500 E-mini Futures

Technical: Broad-market equity indices struggled to hold onto recent gains, evidenced by the failed continuation higher.

Recapping last week’s action: On Monday, after a good amount of volatility contraction, the S&P 500 opened inside prior balance and tested lower, before rotating higher, into the gap zone left from the late February sell-off. Pre-open on Tuesday, the market rallied, further discovering prices up into the gap zone. After the U.S. cash open, Tuesday’s activity was reminiscent of rebalancing to recent overextension.

On news that China would react to the closure of its consulate in Houston, Texas, Wednesday’s session saw prices push lower overnight, before turning and balancing out higher, into the close. On more news regarding geopolitics and initial jobless claims turning higher, Thursday’s session experienced a news-driven, emotional liquidation, with the Nasdaq leading lower.

Friday’s session opened near a high-volume area, balancing out and trading responsively, before closing and accepting prices lower.

Looking beyond broad market indices, the innovation-driven, technology-based sectors are showing signs of relative weakness, while other sectors, such as industrials, energy, and financials are finding more support.

Overall, the S&P is in balance. Absent positive news regarding geopolitical tensions, monetary policy, a vaccine, earnings, and stimulus, the market may find itself correcting through time, testing the prior balance area, below $3,180, as more impactful earnings are released.

Scroll to the bottom of this story to view non-profile charts.

Key Events: Earnings; Durable Good Orders; Consumer Confidence; Initial Claims; GDP; Personal Income; Personal Spending; Employment Cost Index; Consumer Sentiment.

Fundamental: Big tech antitrust probe report from Congress expected early fall.

- Nasdaq Composite, tech weakness comes alongside a weaker dollar.

- Five charts illustrating U.S. economic trends amid the coronavirus pandemic.

- General Motors Company GM, Volkswagen AG VWAGY, Nissan Motor Co Ltd NSANY charge ahead with electric-vehicle plans.

- Consulate closures mark escalation between U.S. and China.

- Boeing Co BA to delay 777X as demand drops for big jets.

- Intel Corporation INTC shares dive on manufacturing retreat.

- American Express Company AXP warns of slow spending recovery.

- Inflation-adjusted bonds are currently priced for very low inflation.

- Proposal to suspend certain payroll taxes is a high priority.

- U.S. home prices, existing home sales rise toward records.

- Tesla Inc TSLA chose Texas for the new Cybertruck factory.

- FDA orders unauthorized e-cigarettes removed from the market.

- China’s regulators take over insurers, financial institutions to cut risks.

- Supplemental unemployment benefits expire alongside new stimulus efforts.

- Housing strengthens while mortgage forbearance continues to decline.

- Biden may enact higher taxes, climate reform, and increased health care spending.

- Earnings beat expectations, but fundamentals remain weak.

- Commercial real estate market slips despite Federal Reserve action.

- The face value of defaulted non-financial corporate bonds jumped to a record.

- American Airlines Group Inc AAL, United Airlines Holdings Inc UAL to lay off workers.

- Dell Technologies Inc’s DELL VMware spin-off increases uncertainty.

- U.S. global investment banks preserved capital strength in Q2 amid credit provisions.

- UnitedHealth Group Inc’s UNH earnings, lower leverage is credit positive.

- Sentiment: 26.1% Bullish, 27.1% Neutral, 46.8% Bearish as of 7/22/2020.

Product Analysis

S&P 500 E-mini Futures (ES) | SPDR S&P 500 ETF Trust SPY

Nasdaq-100 E-mini Futures (NQ) | PowerShares QQQ Trust QQQ

Russell 2000 E-mini Futures (RTY) | iShares Russell 2000 Index IWM

Gold Futures (GC) | SPDR Gold Trust GLD

Crude Oil (CL) | United States Oil Fund LP USO | Invesco DB Oil Fund DBO | United States 12 Month Oil Fund USL

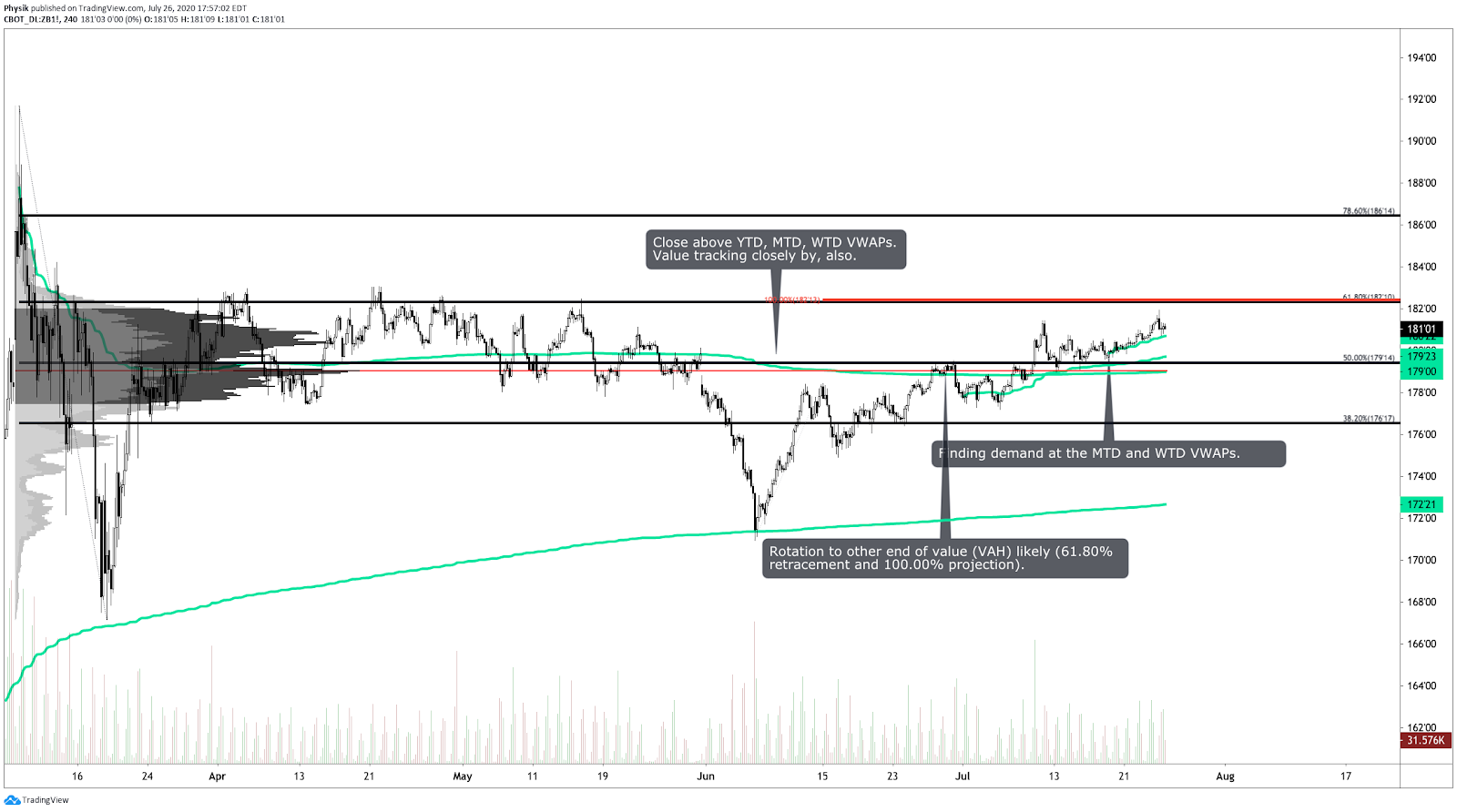

Treasury Bonds (ZB) | iShares 20+ Year Treasury Bond TLT

Photo by Karolina Grabowska from Pexels.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.