(Wednesday Market Open) Equity index futures were trading higher before the market open and ahead of today’s Fed rate decision. Up until last Friday’s Consumer Price Index (CPI) report, the Fed was expected to raise the overnight rate 50 basis points, but now much of the market is expecting 75 basis points.

Potential Market Movers

The Fed isn’t the only central bank making headlines. The European Central Bank (ECB) called an emergency meeting today to discuss the widening gap between yields in various countries. Yields are fragmenting as some countries have seen rates rise at a faster pace particularly in Italy‚ but Italian yields fell on the announcement of the meeting. The ECB said it plans to use existing tools and create new ones to address the situation with specifics to come.

On top of the ECB news, there’s a couple of new economic reports for the Fed to dig through this morning before they announce their June rate this afternoon. First, the Mortgage Bankers Association (MBA) reported a break in the slide of mortgage applications with a 6.6% increase last week. However, though the average 30-year mortgage moved up to 5.65% last week, this week the 30-year is on track to finish above 6%. To date, mortgage applications are less than half what they were a year ago.

Second, the May retail sales report came in lower than expected, down 0.3% instead of 0.2%. This is a bad report because it isn’t adjusted for inflation, so the actual sales number is lower than the headline. For example, gasoline was the biggest expense for the month, and when removed from the report, sales growth was negative. Core retail sales also come in lower at 0.5% instead of 0.8%.

Import prices into the United States increased 0.6% in May, below the forecasted increase of 1.1%. Higher fuel prices offset lower nonfuel costs. While imports were less than expected, they continue to grow and provide a drag on the U.S. gross domestic product (GDP). The strong U.S. dollar has made foreign goods more attractive because they tend to be less expensive.

The Chinese economy is also experiencing weakness in retail sales. May’s number fell 6.7% above the -7.1% forecast and better than the April’s drop of 11.1%. Despite ongoing COVID-19 lockdowns, China reported a 0.7% increase in industrial production year over year. Finally, China’s unemployment rate decreased from 6.1% to 5.9%.

The 10-year Treasury yield (TNX) came off yesterday’s highs in premarket action, falling from 3.48% to 3.37%. The Cboe Market Volatility Index (VIX) also pulled back ahead of the opening bell to 32. AVIX above 30 is still a sign of elevated caution for investors.

Reviewing the Market Minutes

Hours away from the Federal Reserve’s pivotal June rate decision, investors got an even better idea of what a bear market feels like.

After an early-morning rally in the futures markets briefly reversed Monday’s heavy losses, all major U.S. indexes but the Nasdaq Composite ($COMP) finished in the red. Among all sectors, information technology and energy were the only gainers while utilities, consumer staples, and health care, all key defensive groups, finished in the red.

As the last major government report announced before the start of Tuesday’s Federal Open Market Committee (FOMC) meeting, the May Producer Price Index (PPI) met expectations but didn’t excite investors. Wholesale prices rose to a near-record 10.8% pace year over year and are up 0.8% for the month, doubling April’s numbers. Without food, energy, and trade, core PPI rose 0.5% for the month, slightly below estimates but still up 0.4% from April.

Later in Tuesday’s session, a sharp sell-off in the mortgage securities market sent 30-year mortgage rates higher than 6%. The bellwether rate has jumped 60 basis points in the last two days alone.

Recession worries accelerated after the yield curve inverted briefly during Monday’s and Tuesday’s sessions. The yield on the benchmark 10-year Treasury yield (TNX) climbed to 3.482% Tuesday, up from 3.371% on Monday.

Investors spent most of the day debating whether a now-consensus 75-basis-point Fed rate hike would actually slow the flow of bad news. Near the close, the CME FedWatch tool reported a 95.8% probability of at least a 75-basis-point rate hike announcement this afternoon, a significant change from Fed Chairman Jerome Powell’s pronouncements weeks ago that the central bank would aim for serial monthly 50-basis-point hikes to curb inflation.

The Cboe Market Volatility Index (VIX) finished a little higher than 32.

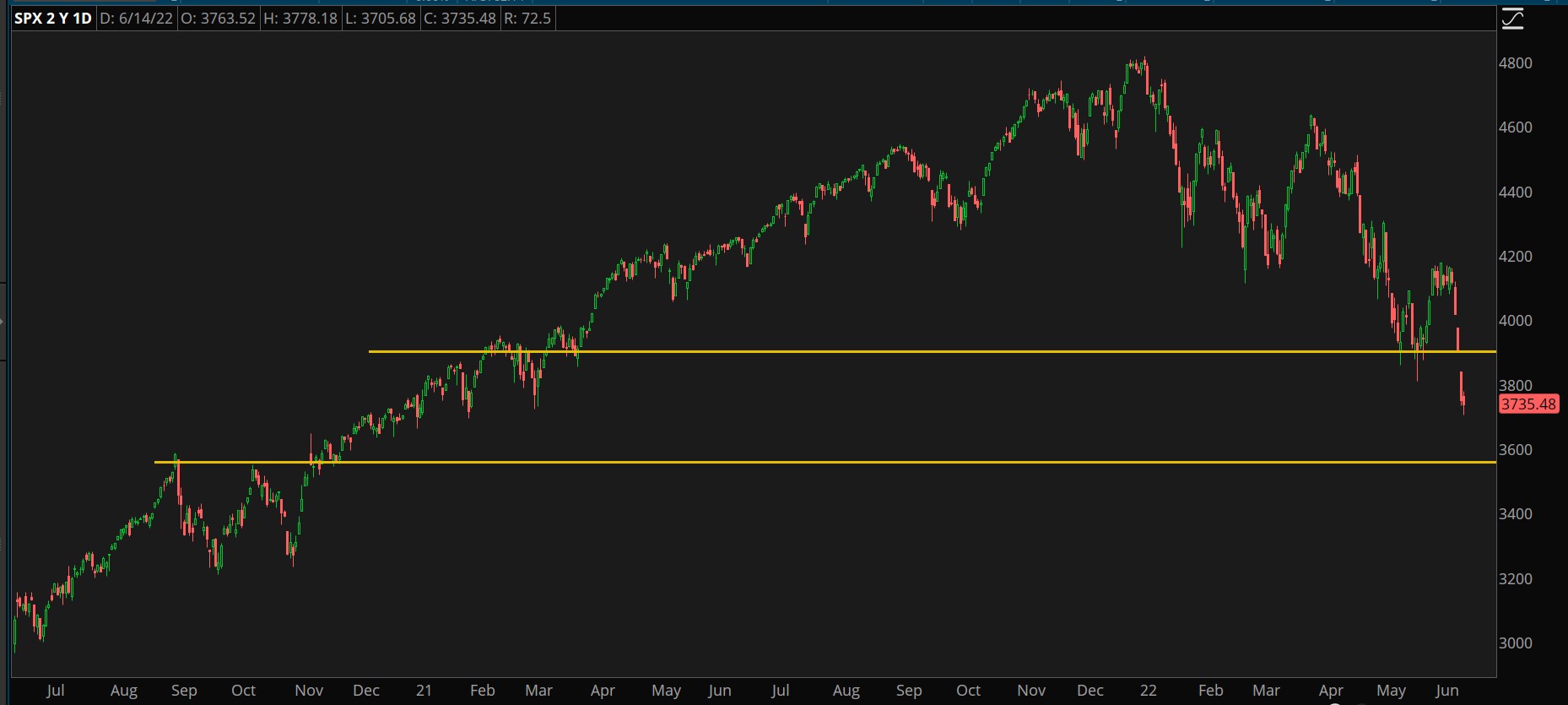

By the close, the S&P 500 (SPX) closed down 0.38% to 3,735.48, the Dow Jones Industrial Average ($DJI) lost 0.50%, and the Russell 2000 finished off 0.39%. The Nasdaq Composite ($COMP), meanwhile, finished up a slight 0.18% by the end of trading.

Among Tuesday’s market highlights:

- FedEx (FDX) announced Tuesday it would double its quarterly dividend, sending the parcel delivery giant’s stock up higher than 28% by the close. The company also added two new directors.

- Moderna MRNA gained 4.43% Tuesday, followed by an announcement after the close by the U.S. Food and Drug Administration (FDA) recommending MRNA’s two-dose COVID-19 vaccine for children ages 6 to 17.

- Oracle ORCL, which reported better earnings after Monday’s close, gained another 10.4% following Monday’s 9% advance in after-market trading.

- Continental Resources CLR gained 9.72% by the close after chairman Harold Hamm offered to buy the remaining shares of the shale company for around $4.3 billion.

CHART OF THE DAY: NOT IMPRESSED. The Federal Reserve’s job turning around the economy has gotten even tougher as the S&P 500 Index (SPX—candlesticks) settled even further into bear market territory after closing below 3,800 on Monday. SPX has fallen nearly 10% in June for its worst performance since 2008. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

You Asked for It: The Wall Street Journal reported Tuesday that Goldman Sachs GS, Barclays BSC, and J.P. Morgan JPM were among firms telling clients that they believe the Federal Reserve would vote for a June rate increase of at least 75 basis points. Investors seemed to join them en masse by the rest of the session. Whether the Fed bows to Wall Street’s wishes or not, it will be interesting to see how Fed Chairman Jerome Powell elaborates on his May 12 remarks that controlling inflation “may include some pain.”

Back-to-School: According to the latest Mastercard MA SpendingPulse report, back-to-school shopping is expected to grow by 7.5% this year. Since this number isn’t adjusted for inflation, it’s likely rising prices may be the single biggest driver behind these gains. It’s also possible that fewer items will be sold because consumers are force to pinching pennies due to rising inflation and revolving credit rates. According to Mastercard, back-to-school shopping is the second largest shopping season after holiday shopping at year-end. Earlier this month, Target TGT announced plans to unload inventory by offering deep discounts on items in order to clear room for the back-to-school and holiday shopping season. It will be interesting to see what consumers think of those sale prices.

SpendingPulse reported double-digit sales growth in May lead by department stores, jewelry, and luxury items. We’ve seen this trend among some select luxury companies including Signet Jewelers SIG, Capri Holdings CPRI, and Nordstrom JWN reporting solid results in recent weeks.

Bitcoin Bobble: As investors continue to eschew risk, bitcoin continues to plunge and is near $20,000, falling more than 10% in the last 24 hours and 30% from last Friday. Bitcoin hasn’t traded below $20,000 since late 2020, which means a break below this level could be a psychological blow to the pioneering cryptocurrency. Crypto traders will also be focused on today’s Fed announcement because it could be a catalyst that breaks $20,000.

Notable Calendar Items

June 16: Building permits, Housing starts, Philadelphia Fed Manufacturing Index and earnings from Adobe ADBE, Kroger KR

June 21: Existing home sales

June 22: Earnings from KB Home KBH and H.B. Fuller FUL

June 23: Initial jobless claims, U.S. manufacturing PMI, and earnings from FedEx FDX, Accenture ACN, and Darden Restaurants DRI

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Featured image sourced from Unsplash

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.