Hold onto your coffee cups, 'cause we're kicking off the day with GREAT news! GDP soars to 2.4% in Q2 2023. This is up from 2% in Q1. The “for sure recession" is nowhere in sight - it vanished like a magician's trick!

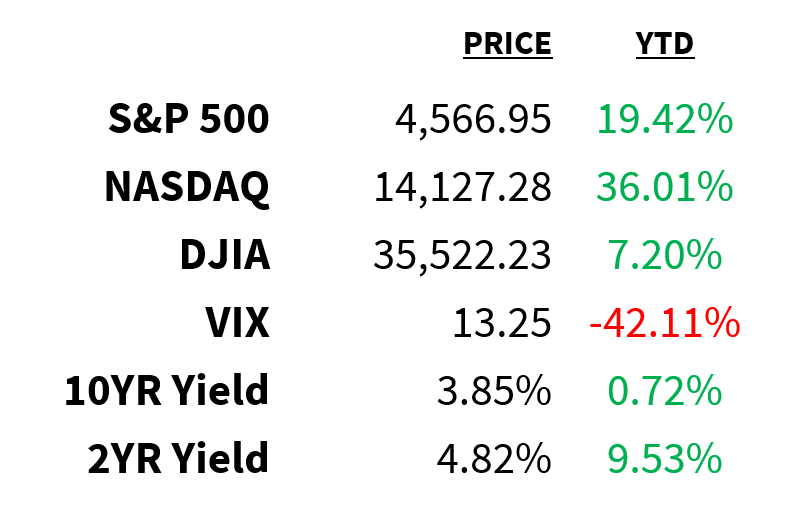

Market

Prices as of 4 pm EST, 7/26/23

Macro

Sales of new single-family US homes fell 2.5% in June to 697k.

-

The previous month’s sales were also revised down significantly from 763k to 715k.

-

The median sales price fell 4% YoY to $415,400.

-

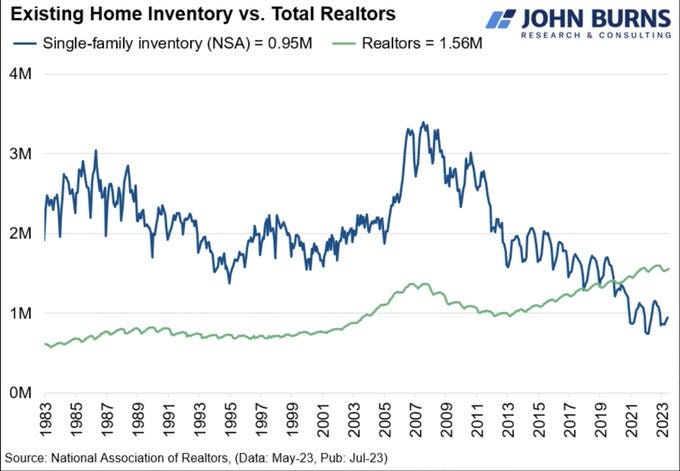

Keeping the market tight is a shortage of inventory.

-

In fact, according to John Burns, there are 600k more realtors in the US than there are homes for sale:

John Burns

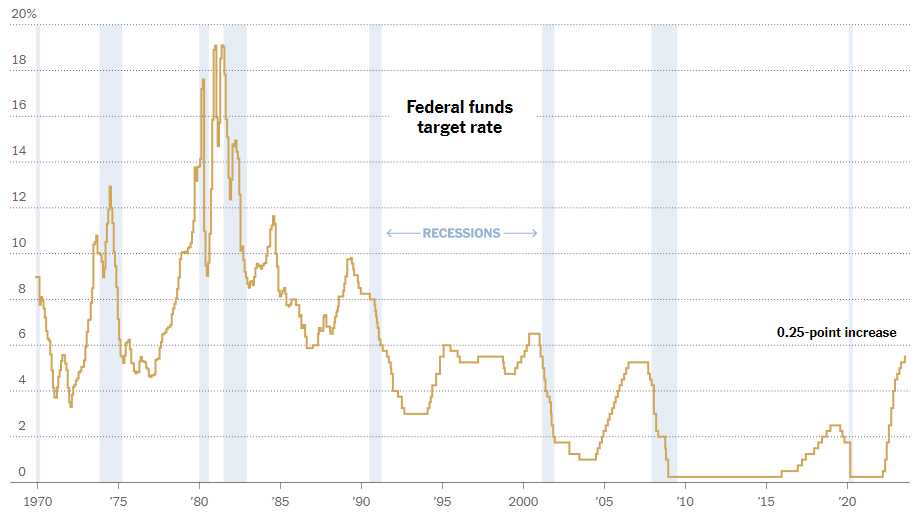

The Fed raised interest rates to the highest in 21 years yesterday.

-

FOMC officials voted unanimously to hike by 25bps to 5.25-5.50.

-

The move surprised exactly no one.

-

At the presser, Powell stressed upcoming meetings would be “live” (i..e, no decisions have been made).

-

He suggested that target inflation (2%) wouldn’t be reached until at least 2025.

-

He also noted that staff are no longer predicting a recession as their base case.

NYT

Stocks

As we noted yesterday, the Fed’s rate increase was mostly priced in ahead of the official decision.

-

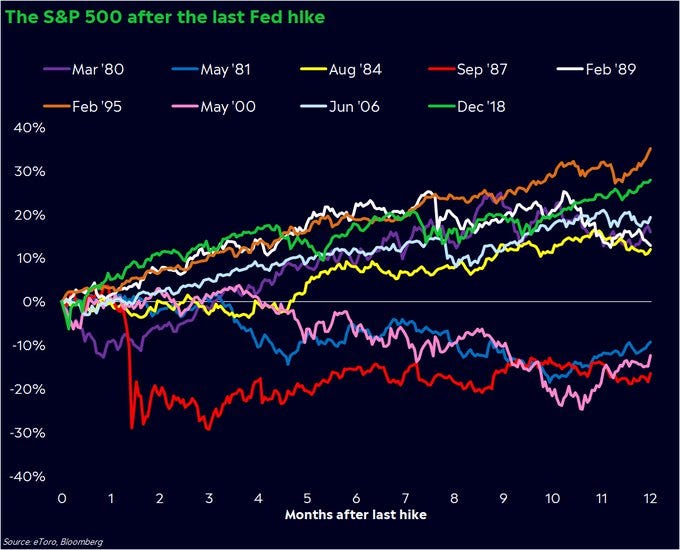

If yesterday’s hike proves to be the last, what can we expect from stocks?

-

The S&P has gained an average of 7.6% in the 12 months following the end of a rate hike cycle (chart).

-

Zooming out further, the S&P has gained an average of 46.2% and 70.6% in the 3- and 5-year periods after the last hike.

@callieabost

Global equities have seen back-to-back months of inflows for the first time since March 2022.

-

Leading the way lately is the Dow, which has posted 13 straight sessions of gains—the longest streak since 1987.

-

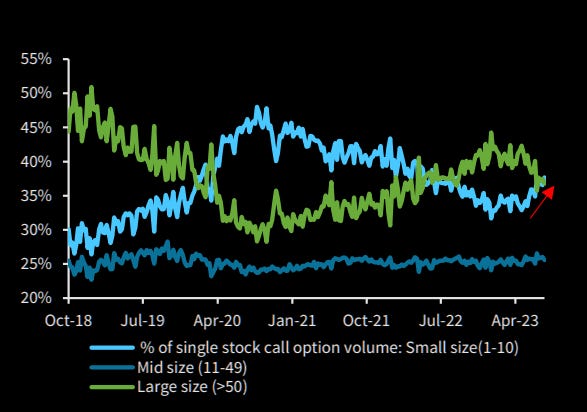

Also leading the way are retail investors whose demand for equities has been rising.

-

In fact, retail investors are now buying more call options than institutions are (chart).

-

Smart money is now playing catchup.

-

Even so, equity allocations from both retail and institutional investors remain far from excessive, according to Barclays.

Barclays

Energy

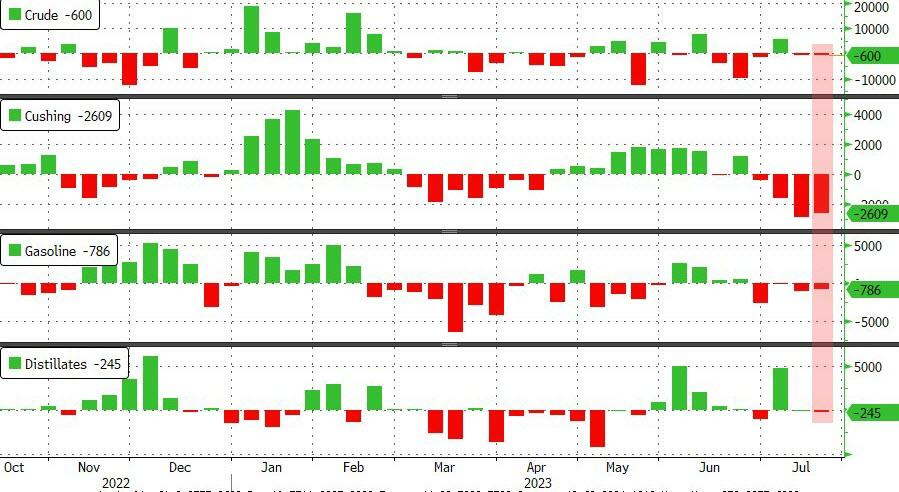

Crude is up this morning following yesterday’s inventory draw.

-

Crude inventories fell by 600k barrels (vs. 2.2 million expected).

-

Cushing, gasoline, and distillates stocks also declined.

-

Both WTI and Brent prices are at their highest since mid-April.

EIA/Zero Hedge

Earnings

Yesterday’s highlights:

Meta META: $2.98 EPS (vs. $2.91 expected), $32 billion in sales (vs. $31.12B expected).

-

Meta saw growth across daily active users (DAUs), monthly active users (MAUs), and average revenue per user (ARPU).

-

The company guided current quarter revenue above analysts’ estimates and suggests 15% YoY growth.

Boeing BA: -$0.82 (vs. -$0.88 expected), $19.75 billion in sales (vs. $18.45B expected).

-

The jet maker posted better-than-expected cash flow and reiterated its guidance for the full year.

-

It also plans to boost production to help meet booming travel demand.

What we’re watching today:

-

Mastercard MA

-

AbbVie ABBV

-

McDonald’s MCD

-

Shell

-

Linde LIN

-

Comcast CMSA

-

T-Mobile TMUS

-

TotalEnergies TTE

-

Intel INTC

-

Honeywell HON

-

S&P Global SPGI

-

Bristol-Myers Squibb BMY

-

Mondelez MDLZ

Top Headlines

-

UK retail: Retail sales in the UK declined at their fastest pace in over a year.

-

ECB decision: The European Central Bank is expected to raise rates by 25bps today.

-

EV partnership: Several big automakers are teaming up to invest in building ~30k EV chargers throughout the US.

-

Chinese EVs: China’s automakers are eyeing US markets for their cheap EVs.

-

Chinese equities: Hedge funds are rushing into Chinese stocks after the politburo signaled stimulus ahead.

-

Maps battle: Meta, Microsoft, and Amazon are teaming up to take on Apple and Google in maps.

-

Unprofitable reality: Meta’s Reality Labs has lost more than $21 billion since the start of last year.

-

Not cool: A group of hedge funds is seeking to intercept a ~$1 billion payout meant for opioid addiction victims.

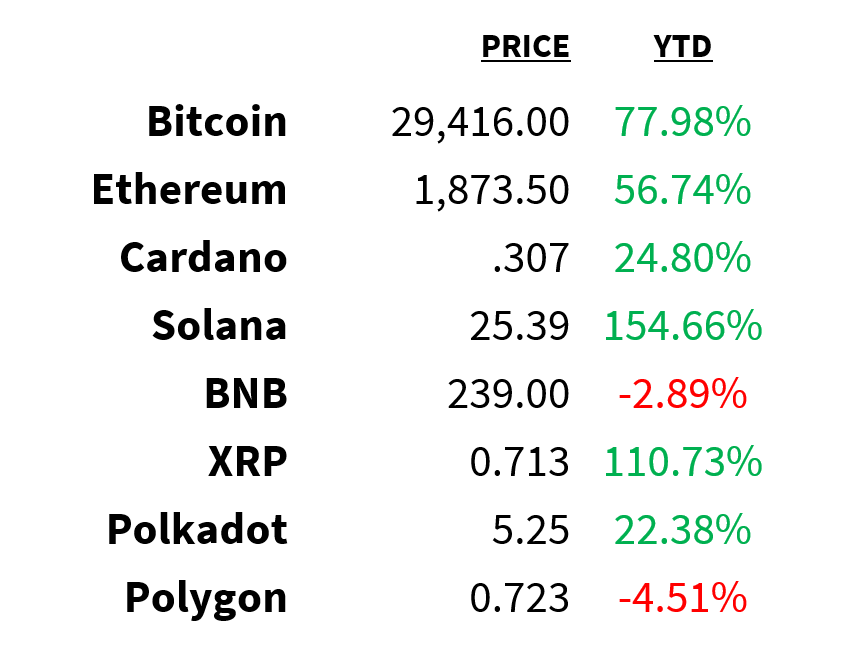

Crypto

Prices as of 4 pm EST, 7/26/23

-

Crypto bills: The US House Financial Services Committee voted in favor of 2 crypto-related bills.

-

SBF charges: Prosecutors have dropped campaign finance charges against Sam Bankman-Fried.

-

Rekt: Immunefi, Polygonn Labs, and Solana have jointly introduced “Rekt Test”, a baseline security standard for web3.

-

Institutional interest: Bitcoin and Ether futures saw record participation from institutional investors in Q2.

-

Compliance: Binance has exited Germany, the Netherlands, and Cyprus as it prepares to comply with new EU MiCA rules.

Deals

-

Teams probe: Microsoft is facing an EU probe over unfair bundling of its Teams app with Office 365 packages.

-

Bank M&A: JPMorgan will purchase $1.8 billion of mortgages to facilitate Banc of California’s PacWest purchase.

-

Lifeline: Carlyle is providing iRobot with a $200 million loan to help keep it afloat during the review process of its acquisition by Amazon.

-

Healthcare sale: The owners of the Plan-B pill are considering selling for over $4 billion.

-

Private funding: Private capital fundraising in Asia Pacific is on track to hit a 10-year low in 2023.

Meme Of The Day

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.