As a comedian once said, “And away we go!”

Earnings season kicked off today with a bang as both JP Morgan Chase JPM and Goldman Sachs GS easily surpassed analyst’s average estimates on the top and bottom lines. Despite the beats, neither stock moved much in pre-market trading.

JPM absolutely crushed it, setting an all-time high with its best quarter ever in investment banking. The only reason shares moved slightly lower after the earnings announcement might be because people are wondering if they can do it again. GS had worldwide dealmaking that was off the charts.

Before discussing banks in more detail, there was some inflation news this morning that’s a bit unnerving. The June consumer price index (CPI) rose 0.9% from May, with the same gain for core CPI that strips out energy and food. Both were much higher than the 0.5% Wall Street analyst consensus. While the Fed keeps calling inflation “transitory,” the question is how long transitory might be. The year-over-year CPI gain of 5.4% was the highest in 13 years. Core inflation growth of 4.5% was the highest since 1991.

It looks like the inflation gains might be stealing some of the sizzle from these strong bank earnings.

A Strong Day One For Banks

With these pretty amazing results, some of the nervousness around the banks has hopefully been put aside. It’s not certain every bank can put up numbers like these, but we’re off to a pretty darn good start. This is only day one of a long road when it comes to earnings season, naturally. It’s kind of like, “Next man up.” We’ll have to see what the pattern will be. It’s a great first day, but it’s just one day.

Putting things into perspective, some of the bottom line gains came from the banks releasing reserves they’d put aside during Covid for reserve against possible losses on loans. You could argue that this aspect of earnings isn’t really the same as organic growth. JPM, for instance, took a $2.3 billion earnings benefit this quarter as it released reserves, but pointed out that these aren’t core earnings nor are they recurring.

If you want to pick things that weren’t perfect, JPM came up a bit short of analysts’ estimates in its fixed-income trading business, though equities trading was better than the Street had expected. Trading revenue fell year over year at GS. Most analysts said trading revenue at the big banks would likely be down considering the situation last year at this time when trading surged as people tried to take cover during the worst of the lockdowns.

With the big bank earnings, it’s always important to check the tone of the releases and listen closely to what executives say on their calls. One key takeaway from JPM’s release is a quote from CEO Jamie Dimon, who said, “Consumer and wholesale balance sheets remain exceptionally strong as the economic outlook continues to improve.” That’s arguably a nice stamp of approval on the economic situation from a CEO whose words tend to carry a lot of weight on Wall Street.

The press release quote from GS CEO David Solomon was a bit more reserved. “While the economic recovery is underway, our clients and communities still face challenges in overcoming the pandemic,” Solomon said. Investment banking revenue at GS rose from Q2 2020 but slowed a bit from Q1 2021. Trading revenue fell from the amazing levels of a year ago, but looked relatively strong.

Banks weren’t the only earnings story today. PepsiCo PEP raised its outlook after easily beating Wall Street’s earnings estimates. Net sales rose more than 20%, and overall earnings looked really good. It’s pretty interesting to see PEP’s foodservice revenue soar during the quarter because this is the category that includes restaurants and other venues. People appear to be getting back out again.

The markets turned red going into the opening bell, possibly due to the inflation data. Another drag might be Boeing BA, which announced it faces a new production problem with its 787 “Dreamliner.” Shares fell 2% in pre-market trading.

Up Next? More Bank Earnings, What Else?

Today’s bank earnings set the stage for another round of bank industry Q2 reports tomorrow and Thursday. While year-over-year earnings are expected to rise sharply for Bank of America BAC, Citigroup C, and Morgan Stanley MS, any drop in trading could weigh on year-over-year revenue growth.

Remember that a year ago, trading was frantic during the pandemic, and it’s calmed down quite a bit over the last few months. That probably means fewer people making trades in both fixed income and equities, where some of the biggest banks harvest a lot of their cash.

With BAC, trading revenue continues to be under a microscope. The company scored big in that category last time out after missing Wall Street’s estimates in Q4. C’s credit card business will get scrutiny to see how that’s holding up as consumers seem to be in a transitory mode. BAC and C both are straight ahead Wednesday, and MS, the last of the big banks to report this week, is expected to open its books on Thursday.

Another earnings report to consider watching this week is Delta DAL, and we’ll talk more about that and the other airlines below. Besides DAL, PepsiCo PEP, and banks, it’s actually not the most crowded earnings week. Kansas City Southern KSU could be another company to watch because Canadian National CNI recently made a bid to buy it. One question for KSU on its call later this week could be how President Biden’s recent anti-competition executive order might affect chances for the deal to be completed.

Record Highs Again To Start Week, But Mind The Gap

Before all that, the week began basically where the old week left off. It was another session of new all-time highs for the S&P 500 Index (SPX) Monday, with broad-based strength across almost every sector with the exception of Energy and Staples. Financials led as investors appeared bullish on banks heading into earnings season.

Surprisingly, the Financial strength didn’t seem to help the Russell 2000 Index (RUT) small-cap index much, even though the RUT is heavily weighted toward banks. Also, Energy slipped as crude prices dialed back a bit to start the week.

Crude remains elevated on tight supply concerns, but worries about the spread of the Delta variant of Covid and its possible impact on demand have helped keep crude from cruising past the three-year highs it posted recently near $76 to $77 a barrel. A while ago we pinpointed that area as a possible tough one for crude to surpass that, and so far it’s held. There’s a bunch of reasons why crude might be bumping its head, but also some worries it could rise to $80 or above.

Another worry this week could be what some analysts believe is a narrowing of the market’s winners. Not too long ago, all the major indices were posting new record highs. Lately, the Dow Jones Industrial Average ($DJI) and the RUT haven’t joined the party. Over the last month, Tech has outrun all the other sectors while cyclical ones like Financials and Energy that generally do well in an expanding economy are in the red.

One theory is that with interest rates falling, investors have gotten worried about economic growth, which could be sending them from cyclical into Tech as they embrace some of the “mega-cap” FAANG stocks and Microsoft MSFT.

Obviously, people who own FAANGs and MSFT won’t be complaining, considering MSFT and some FAANGs recently posted new record highs for the first time in months. Still, if the pattern continues, it might speak to a narrower number of stocks moving higher while the rest of the market stands on the sidelines.

A broader rally tends to be healthier, especially when you consider what happened in late 2018 when the mega-caps ascended on their own and the entire market fell apart when investors started to take profit on big Tech. Remember, the SPX is weighted by market capitalization, which gives a handful of Tech and Communication Services stocks a huge impact on index performance. Keep an eye on the Tech sector. If it continues to throw its weight around, so to speak, and other sectors lag, that could be a warning sign.

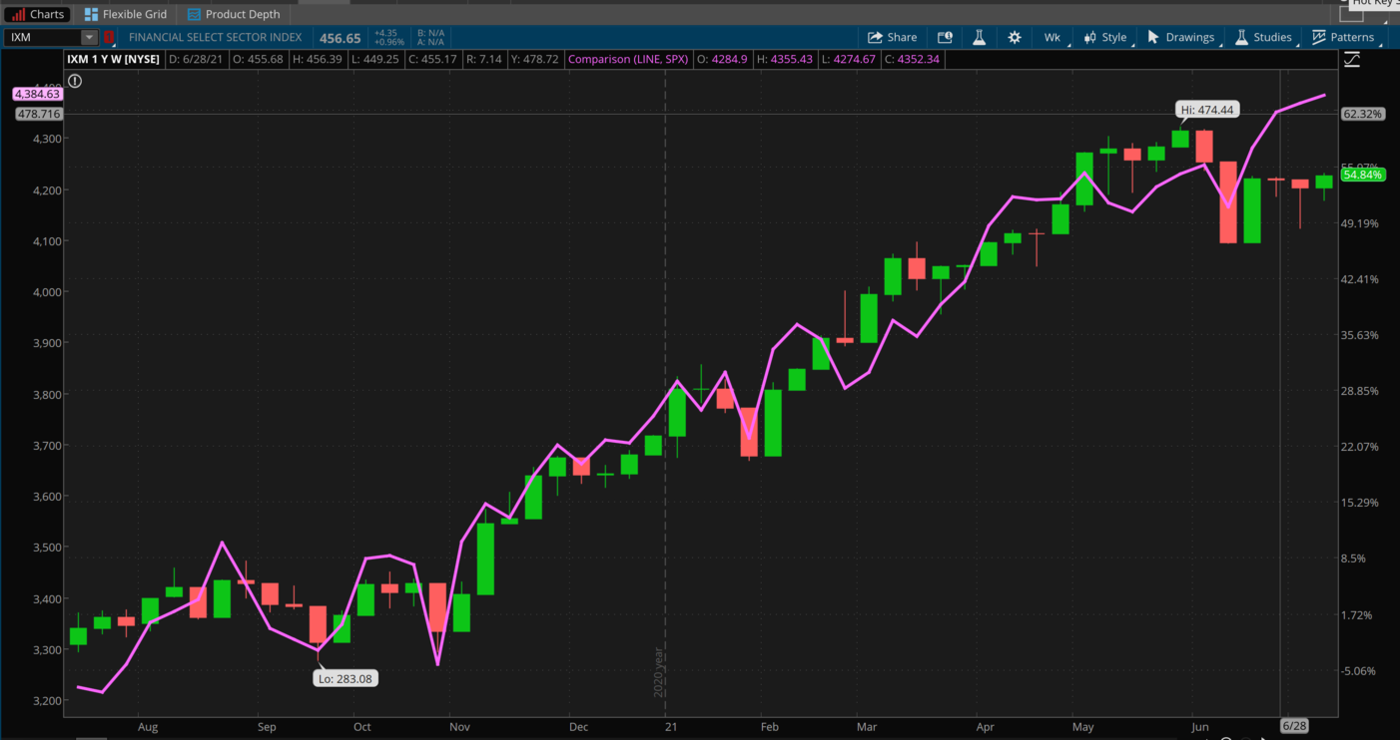

CHART OF THE DAY: FINANCIALS LOSING THEIR EDGE? Though both the Financial sector (IXM—candlestick) and the S&P 500 Index (SPX—purple line) have run up huge gains over the last year, Financials have lost ground to the broader market over the last month or two as bond yields sink. Today is the beginning of Q2 bank earnings season. Data Source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

The Treasury Auctioneer’s Gavel: The recent slide in Treasury yields may have been—at least in part—due to a lack of fresh supply. That began to change a bit Monday with auctions of both three-year and 10-year notes. The 10-year auction looked like it drew more interest, which is worth noting considering how low yields are. Maybe investors were looking for what they might consider a less risky investment amid concerns about the Delta variant (though as a reminder all investments have risk).

One reason yields (and inflation worries) may have softened recently until the slight pop over the last few days could be the realization that price comparisons vs. a year ago start to get a little less dramatic as we move further into the year. Remember that by last summer, much of the economy had reopened, meaning growth was starting to recover from the Covid lows and prices also had begun to go up.

June producer price data tomorrow (see below) could still show sharp increases on a yearly basis, but by later this year (there’s debate about how late) these might start coming down. Remember, markets tend to look ahead, so perhaps it won’t be too big a shock if we don’t see a big reaction in the Treasury market to tomorrow’s report, barring some sort of major surprise.

Inflation Chronicles Continue Tomorrow: Today’s CPI data are the first in a one-two punch of inflation numbers this week. Tomorrow morning we get producer prices for June, and analysts expect a slight easing from May. The consensus is for headline PPI growth of 0.6% and core PPI growth of 0.5% for June, according to research firm Briefing.com. That’s still historically high, but compares with 0.8% and 0.7%, respectively, for headline and core PPI growth in May.

Even if growth is slower month-to-month, numbers like the ones analysts expect would be sharply higher from a year ago when Covid had the economy locked down. In May, PPI growth of 6.6% from a year earlier was the strongest ever recorded and fueled worries that producers might either see their margins narrow or be forced to pass along higher costs to customers. At the time, bond yields made a quick leap, but have since eased a lot.

Look…Up In The Sky: It isn’t just the banks reporting this week. We also get a first glimpse at the airline industry with Delta DAL expected to report early tomorrow. It could be interesting to hear from the airlines about how the global reopening is going. While vaccine rollouts in the United States have helped open travel back up, other parts of the globe aren’t faring as well. And worries about the Delta variant (no relation) of COVID-19 don’t seem to be helping things.

Beyond DAL this week and American AAL and United UAL later this month, the market may be looking for guidance from their executives about the state of global travel as a proxy for economic health. Remember, though, that business travel is where a lot of airlines traditionally made bigger profits, and that aspect of the economy is far from recovered. DAL’s losses are expected to narrow and revenue to rebound, according to analysts who track the company. Growth in leisure travel and premium seats may be tailwinds, Investor’s Business Daily reported.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image by Jo Wiggijo from Pixabay

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.