There’s a phrase on Wall Street that investors often “buy the rumor and sell the fact.”

We may be seeing some of that this morning after President-elect Joe Biden late Thursday unveiled a $1.9 trillion stimulus plan that includes direct payments, increased additional federal unemployment help, state and local government aid, and raising the federal minimum wage to $15 an hour.

The market has been in an uptrend in part on expectations of fresh stimulus from the Biden administration. With that priced in, investors may be taking the actual announcement as a time to book some profits. There could also be some concern about how raising the minimum wage could affect businesses at a vulnerable time while the pandemic continues.

Biden’s announcement came ahead of major bank earnings this morning, which investors seem to be paying close attention to as a potential gauge for how the rest of the fourth-quarter reporting season might go.

Big Banks Ring The Opening Bell On Earnings Season

The buy-the-rumor-sell-the-fact dynamic may apply to JPMorgan Chase & Co. JPM as well. JPM had a tremendous quarter, with revenue topping expectations and earnings coming in at $3.79 per share when analysts had expected just $2.62. The strong quarter came as the bank was able to unwind some of its loan loss provisions and trading was strong amid the support the market has been seeing from the Federal Reserve.

But JPM shares were trading 1% lower in the premarket, perhaps a result of JPM having been on quite a tear, rising nearly 48% since the start of November.

JPM CEO Jamie Dimon may have contributed to this morning’s general weakness, saying there is still “significant near-term economic uncertainty.”

Still, although the bank is keeping credit reserves of more than $30 billion, the fact that it was able to release some of the money it had set aside for loan losses seems good news for the broader economy as it continues to recover, and as it looks forward to more stimulus and wider-spread vaccines.

Turning to the other big bank earnings news from this morning, Wells Fargo & Co’s WFC results were mixed, with the bank-beating expectations on its bottom line number but missing on revenue. Legacy issues continued to haunt it, and its CEO said its “results continued to be impacted by the unprecedented operating environment.” Its shares were off 1.3% in pre-market trading.

Meanwhile, Citigroup Inc’s C shares were also lower despite an earnings beat. The bank reported slightly lower-than-expected revenue.

Last quarter, the banks boosted market sentiment regarding how investors and traders felt about the upcoming earnings season. This time around, it looks like the reaction isn’t as optimistic. Still, we haven’t yet seen all the results from the big banks.

An upsurge in capital markets trading activity and a very strong initial public offering (IPO) market could bode well for Q3 outperformers Goldman Sachs Group Inc GS and Morgan Stanley MS. However, the more consumer-oriented Bank of America Corp BAC might face continued challenges, according to analysts’ sagging estimates for the company.

Jobless Claims Uptick, But Reassurance From The Fed

The main three U.S. indices were relatively muted yesterday as details about President-elect Joe Biden’s stimulus plan came in, new data showed the jobs market has taken a turn for the worse, and Federal Reserve Chairman Jerome Powell reiterated what investors expected to hear about interest rates and bond purchases.

Powell delivered on what most in the market probably expected to hear—that the central bank isn’t planning to raise interest rates or taper its bond purchases any time soon. Despite those tools being in use because of the adverse effects from the coronavirus on the economy, Powell also said the economy might be able to get back to pre-pandemic levels sooner than feared.

Nevertheless, things don’t look particularly great right now on the economic front. Data yesterday showed that weekly jobless claims rose to their highest level since August, spiking to 965,000 when a Briefing.com consensus had been expecting 780,00.

Still, the market opened in positive territory, perhaps as some investors and traders figured the labor market situation might give lawmakers extra incentive to pass further stimulus. As the pandemic has dragged on, it’s also possible that Wall Street has become a bit numb to the jobless numbers. It might be easy to forget that, even if the figure had come in at 780,000, as expected, that’s still an astronomical number compared to where we were before the pandemic.

Shots In The Arm: Stimulus And Vaccines

Stimulus expectations seemed to buoy the market, before it ran out of steam toward the end of the session, on hopes that the stimulus measures will help tide the economy over until vaccines can be widely administered and help the economy get back on its feet.

Speaking of vaccines, Johnson & Johnson JNJ shares finished the day up 1.75% after early safety study data showed its coronavirus vaccine produces a promising immune response. While the vaccine still has a ways to go before it could be authorized for use in the broad population, the findings offer another arrow of good news in the quiver of humanity’s attempts to beat back COVID-19.

It seems that the market has plenty to be optimistic about despite the ongoing pandemic. That might be why big tech-related companies had a down day. All the FAANG stocks ended the day lower, helping pull down the broader market. These stocks have been in heavy demand during the pandemic as their size, cash and technology-focused businesses made them a safe haven investment of sorts while many other companies had a rougher time.

Now, as the vaccine rollouts, stimulus efforts, and Fed backstopping help investors and traders become more optimistic, the big tech-related names have been giving way to stocks that stand to benefit when the economy gets back to normal. That dynamic was borne out yesterday as the Russell 2000 (RUT)— which is made up of small cap domestic stocks that are expected to do better as the economic recovery continues—managed to increase its gains during the day, rising more than 2%, even as the three main U.S. indices pared their gains and ended up in negative territory.

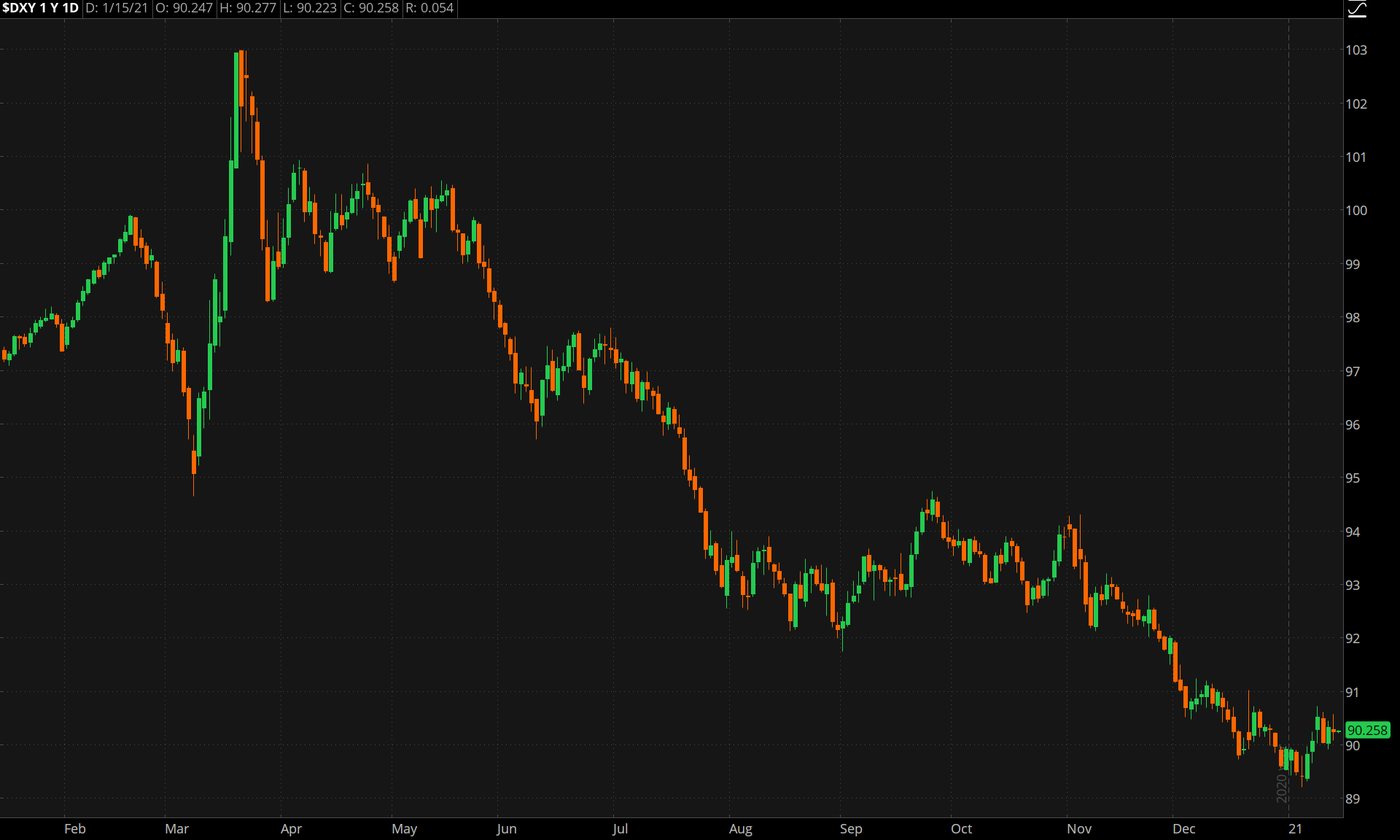

CHART OF THE DAY: The ICE U.S. Dollar Index ($DXY), which measures the buck against a basket of other major currencies, has been on the decline in recent months as Federal Reserve and Congressional efforts to boost the economy have diluted the value of the greenback. A lower buck tends to help U.S. multinationals. See more below. Data source: ICE Data Services. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Mark Your Calendar: Next week’s economic calendar is relatively light, but that doesn’t mean investors get a total break from the flow of important data. The weekly initial jobless claims report may bear even more scrutiny on Thursday, as investors try to discern whether unemployment claims in the 900,000 range might become a trend for a while after this week’s figure. Market participants will also get to look a little deeper into the state of the housing market with reports on housing starts, building permits, and existing home sales. It could be interesting to see how low mortgage rates are affecting those numbers. Notable earnings reports next week include Bank of America Corp BAC, Goldman Sachs Group Inc GS, and Netflix Inc NFLX.

Earnings Outlook Less Bad: Speaking of earnings, fourth quarter S&P 500 Index (SPX) earnings growth estimates have been increasing, with analysts raising their forecast to a 9.8% decline recently from a 14.4% drop in July as the economic recovery has been generally going better than expected, despite some pockets of entrenched weakness and recent data showing a moderation in economic activity because of the third COVID-19 wave, according to Zacks Investment Research. Although the quarterly earnings reports are important, the research firm said the market will focus on expectations for full-year 2021 results. “We strongly feel that current consensus estimates for 2021 GDP and earnings growth understate the full extent of the rebound,” Zacks said. “We see a significant acceleration in the favorable revisions trend in the coming months on the back of a stronger-than-expected rebound in consumer and business spending as the ongoing vaccination effort gains pace.”

More (Or Less) Bang For Your Buck: U.S. stocks have been in a general uptrend as investors have been hopeful that more stimulus from Congress can help jumpstart spending on Main Street. Meanwhile, the Fed’s easy monetary policy has helped boost equities by lowering corporate borrowing costs and lowering bonds’ attractiveness compared to stocks. But Wall Street may also be cheering the money “printing” from the Fed and the unprecedented spending from Congress because those efforts have been weakening the U.S. dollar. A weaker buck can boost the profits of multinational companies by making their products less expensive in markets abroad. If Apple Inc AAPL can sell more iPhones in Europe and other companies can sell more of their goods abroad through Amazon.com, Inc. AMZN, the size of those companies can help lift the market in general when their shares are ascendant.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Katie Moum on Unsplash

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.