Snap-On Inc. (NYSE:SNA) reported better-than-expected second-quarter 2025 results, surpassing both revenue and earnings consensus estimates on Thursday.

Quarterly net sales reached $1.179 billion flat year-over-year increase and above the consensus estimate of $1.16 billion. EPS for the quarter was $4.72, down from $5.07 YoY, above the consensus of $4.67.

For 2025, Snap-on expects continued growth in 2025, expanding its professional customer base in automotive repair and adjacent markets, with projected capital expenditures of $100 million. The company anticipates a full-year 2025 effective income tax rate between 22% and 23%.

Snap-On shares gained 7.9% to close at $337.80 on Thursday.

These analysts made changes to their price targets on Snap-On following earnings announcement.

- Baird analyst Luke Junk maintained Snap-on with a Neutral and raised the price target from $329 to $347.

- B of A Securities analyst Elizabeth Suzuki maintained the stock with an Underperform rating and raised the price target from $265 to $285.

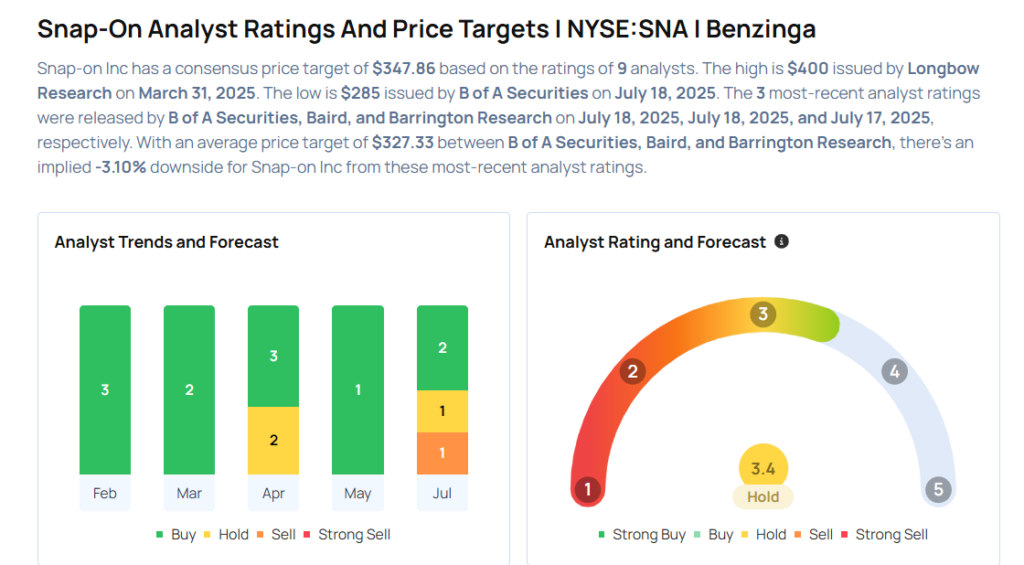

Considering buying SNA stock? Here’s what analysts think:

Photo via Shutterstock

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.