Image sourced from Pixabay

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Wednesday Market Open) A better-than-expected earnings report from Salesforce.com CRM is leading stocks higher, gaining more than 9% in premarket trading. Equity index futures are pointing to a higher open as investors try to bounce back from yesterday’s retreat.

Potential Market Movers

Despite the positive news from Salesforce, the stock may struggle to find a footing. The 10-year Treasury yields (TNX) is up another 2.5 basis points adding to yesterday’s 10 basis points as the June 1 start for the Fed’s balance sheet cleanup begins. Rising yields could put pressure on growth stocks, which means the consumer discretionary and tech sectors could a tough day.

Treasury yields could have additional pressures from oil futures, which were up 1.6% before the stock market opened. The next OPEC+ meeting could be an interesting one for Russia because other nations could choose to raise their production to cut in on the Russian oil markets. However, OPEC members could risk losing a valuable partner with Russia as the Russia-Ukraine war prompts nations to pick sides.

The Cboe Market Volatility Index (VIX) is lower this morning but the last two times it has hit this level in the last month and a half, it has rallied higher. Just as stocks appear to be absorbing bad news and building a bottom, this could be a pivotal level for traders.

After the open, investors will see key reports from ISM Manufacturing and the JOLTS Job Openings. U.S. manufacturing has been weaker, according to the ISM report. Nearly each month the report has reflected slowing starting back in January of 2022. Manufacturing is expected to be lower once again. However, the job market remains strong. JOLTS are expected to be lower than previous months, but still near historical highs.

Reviewing the Market Minutes

Stocks failed to extend the rally that snapped a nearly two-month losing streak on its last trading day in May, one of the most tumultuous market months in recent memory. The S&P 500 (SPX) and the Dow Jones Industrial Average ($DJI) finished nearly flat with their April close as investors turned their attention to key employment data arriving later in the week.

A Memorial Day filled with news about the toughest European energy sanctions yet against Russia, rising global inflation, and the Fed’s latest movements set an uncertain stage for the continuation of last week’s market rally.

All but two of the S&P 500’s sectors finished down on Tuesday with consumer discretionary stocks the top gainer, up 0.76% %, followed by communications services, up 0.41.%. The S&P 500 lost 0.6% Tuesday after ending its seven-week downturn before the long weekend, while the Dow Jones Industrial Average ($DJI) lost 0.7%—leaving both major indexes nearly unchanged for the month by the close. The Nasdaq Composite ($COMP) dropped 0.41% on the day.

The Conference Board’s monthly report showed consumer confidence dropped slightly in May from previous months, and Brent crude went on a roller-coaster ride before finishing up 1% after European Union leaders announced an oil embargo against Russia, their toughest energy sanctions yet. And in a key report for the direction of the housing market, the S&P Case-Shiller Home Price Index showed home prices gained more than 20% during May even as interest rates rose.

Though cloud software leader Salesforce beat on top and bottom estimates, its CEO said it expects to be more “measured” in future hiring. Investors will likely be watching today’s Job Openings and Labor Turnover (JOLTS) report, tomorrow’s unemployment claims numbers, and Friday’s May jobs report for signals indicating whether the nation’s continuing hot job market might finally be cooling. Estimates show nonfarm payrolls likely declined to 320,000 in May from April’s 428,000.

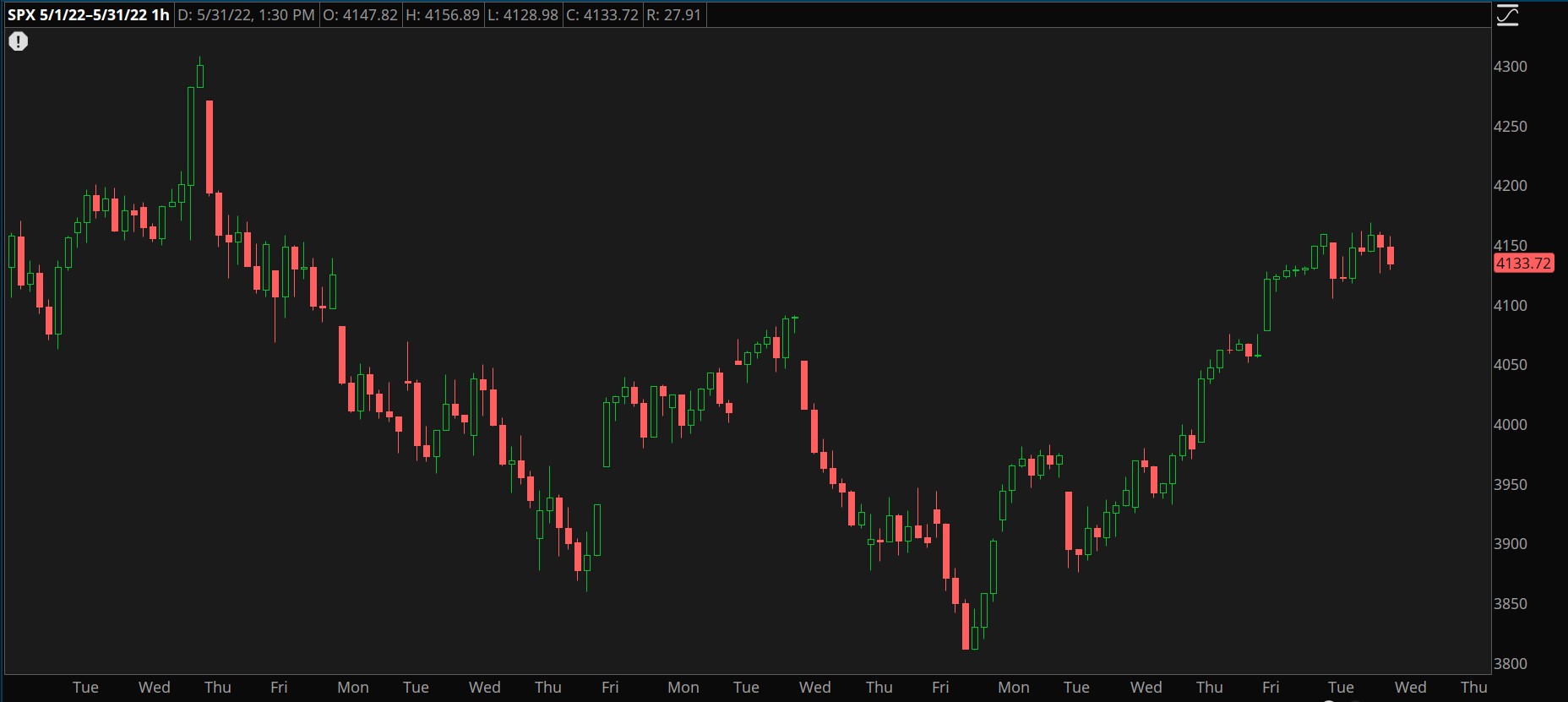

CHART OF THE DAY: BACK TO HIBERNATION? The S&P 500 (SPX—candlesticks) tested historic bear market territory May 20 only to close Tuesday near its starting point at the top of the month. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

Time to Unwind: June 1 marks the first day of the Federal Reserve’s plan to reduce its pandemic-era balance sheet that rose to nearly $9 trillion during the height of the crisis. Much of the Fed’s bonds are expected to simply mature and not be replaced, which won’t directly affect Treasury prices. However, without the Fed buying bonds, the bond markets could see some liquidity issues. Lower liquidity could result in higher volatility in the bond markets.

On Tuesday, the 10-year Treasury yield (TNX) jumped from 2.74% to 2.84%, or 10 basis points. Rates are likely to continue rising as the Treasury market seeks to entice investors into the bond markets to make up for the loss of demand from the Fed. Last time the Fed tried to clear its balance sheet in September of 2019, overnight rates shot up as bank reserves got too low. However, the Fed has tried to account for this risk by setting up a standard repo facility that will work as a permanent backstop. Bank reserves are also more than double than what they were in 2019.

Greasing the Wheels: Treasuries could also see increased pressures from rising oil prices. WTI crude oil futures continue to inch higher and are currently trading above its March and May highs. Last week, BofA Global Research warned that Brent Crude oil could goas high as $150 per barrel without Russian oil exports. The International Energy Agency (IEA) estimated last week that Russia has already reduced its production by nearly one million barrels of oil per day.

NATO and its allies have struggled to put forward a united front against Russia because of the need for Russian oil. Countries like Italy and Hungary continue to rely on Russian imports.

Maybe’s Don’t Fly in June: Data from Schroders shows that June has the worst track record for the number of stock market gains for the S&P 500, FTSE100, MSCI World, and the EURO STOXX 50 from 1987 to 2018. December, April, and October were the best months for market gains while June, August, and September were the worst. Of course, past performance is not a predictor of future results, the old saying of “sell in May and go away” has historically demonstrated some merit.

If yields rise in June from due to the lack of liquidity from the Fed and/or rising oil prices, we could see continued revaluing of stocks as we’ve seen through the first five months of 2022.

Notable Calendar Items

June 2: Earnings from Broadcom AVGO, Lululemon LULU, and Hormel Foods HRL

June 3: Employment Situation Report, ISM Non-Manufacturing PMI, and earnings from Crowdstrike CRWD and DocuSign DOCU

June 7: U.S. Trade Balance and earnings from J.M Smucker SJM, Verint Systems VRNT, and Cracker Barrel CBRL

June 8: Earnings from Campbell Soup CPB

June 10: May Consumer Price Index (CPI) and preliminary University of Michigan Consumer Sentiment Index Results

TD Ameritrade® commentary for educational purposes only. Member SIPC.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.