Yesterday the market got behind the Fed’s idea that inflation is transitory after a calm consumer price index (CPI) reading.

Will that change today after a sizzling producer price index (PPI) reading? Remember that any gains in PPI can often get reflected in CPI down the road as companies react to higher wholesale prices by passing them along to the consumer. And then there’s the other side of the coin—where companies absorb these prices, which can impact margins. Either way, inflation tends to pack a wallop.

Major indices didn’t immediately react much to a July PPI reading of 1%, which was way above the Wall Street analyst consensus of 0.5%. That followed yesterday’s CPI coming in about as expected and well below the June level. The July PPI was equal to June’s, so that kind of takes a bit of the transitory argument away. Also, core PPI, which strips out volatile energy and food prices, was the same as the headline figure, so there’s no hiding behind that.

The PPI report is just the start of today’s action. Later on, Disney DIS steps onto center stage with its earnings report. Focus is likely to be on streaming and whether the Delta variant might slow attendance gains at theme parks and movie theaters. It’s likely DIS executives will be asked how the big jump in Florida cases is affecting the Magic Kingdom in Orlando.

Weekly jobless claims of 375,000 were more in line with estimates and pretty much down the middle compared with recent numbers. There doesn’t seem to be much improvement going on here, but it’s not getting worse, either. The number probably won’t have much influence today.

Instead, investors are likely to spend their time trying to make sense of these contrasting inflation indicators, which might explain why major indices initially went nowhere in pre-market trading on the PPI reading. Does this strong PPI give the Fed more reason to begin its tapering earlier than expected, or will the Fed wait for another month of data to try and get more clarity? If history means anything, we can probably bet on option two.

Inflationary Showdown Shows Slight Slowdown

Wednesday’s Consumer Price Index (CPI) report told investors mostly what they already knew: overall inflation is running hot. But that’s not what the market was keen to focus on. Instead, investors appeared to be looking at the core CPI, which jumped 4.3% year over year as expected but only 0.3% on a monthly basis—a tad less than the 0.4% analysts estimated.

On top of this, the Fed’s “transitory” narrative suddenly seemed a bit more believable as a slowdown in used car prices likely allayed fears of a monetary sudden-brake shock. Used car prices rose only 0.2% in July, a small bump compared to the prior month’s steep 10% surge.

But again, this morning’s PPI seems to be at least a partial counterargument to the transitory view. A single month’s data isn’t a trend, but this is certainly one to keep an eye on.

Following the CPI report, the Dow Jones Industrial Average ($DJI) jumped as much as 200 points, with Caterpillar CAT and Home Depot HD leading the index, while 10-year Treasury yields stood mostly flat, and “FAANG” stocks slid into negative territory, with the exception of Apple AAPL. Could it be that fears of a “too-laid-back” Fed policy are starting to morph into a “just right” Goldilocks scenario?

Big cyclical sectors like Energy and Financials were already on the upswing this week even before yesterday’s bullish CPI data. Strength in these sectors helped give the blue-chip Dow Jones Industrial Average ($DJI) a lift so far over the other major indices.

Small-Caps Still Scuffling

So where does that leave small-caps, which are often known for their solid performance during economic recoveries? The small-cap Russell 2000 Index (RUT) is still scuffling a bit, pretty much flat so far this month and well below its 2021 highs. It did rise a bit on Wednesday, but again got outpaced by the $DJI. It’s basically still stuck in a volatile 5-month “rut” despite the strong and steady doses of easy-money policy.

It might be worth watching to see if RUT can break out of the slow pattern it entered after emerging from its early summer selloff. Which way RUT goes from here might help provide clues about the market as a whole, because RUT can be an early leader up or down.

Another consideration is where the FAANG stocks go if Treasury yields resume their climb. Remember that earlier this year, rising yields appeared to take a big bite out of the “mega-cap” Tech stocks, with AAPL and Tesla TSLA among that hit hardest. It’s fine to say that Financials and Energy can pick up the slack, but that ignores the fact that the FAANGs—like it or not—comprise about 20% of the value of the SPX. That means any significant setbacks for these huge companies could drag the overall index.

Since May, mega-cap Techs have been helping pull up the SPX while some of the other sectors struggle. Analysts are talking about how the rally has less “depth,” meaning it’s more dependent on a few big gorillas to keep it going. While yields aren’t in the kind of territory we saw last spring, it’s worth watching that relationship between yields and FAANGs for clues about where the market goes next.

If inflation growth is actually slowing—and one CPI report isn’t a trend—that could drive optimism that the Fed won’t clamp down right away, perhaps keeping yields from overheating and mega-caps from melting down. Now the PPI report may have people rethinking that. The tug of war continues.

The Sweet And The Sour Impact Of Washington

Stocks got a nice assist from Congress earlier this week when the Senate passed the infrastructure bill. On the opposite side of the equation, markets seem to be ignoring a debate in Congress over the debt ceiling. Treasury Secretary Janet Yellen encouraged the parties to find a solution, and for now, the thinking on Wall Street seems to be that there will be one. However, that doesn’t mean a smooth process.

There was eventually a solution in 2011, too, and the U.S. didn’t default on its debt payments. But it did see its credit rating lowered, and stocks took a pounding that summer. We’ll see if Congress can avoid getting to that point this time around. As a reminder, the debt ceiling has been raised numerous times since the 1980s, with both parties voting to do so. The last time was in 2019, under President Trump.

If the debt ceiling fight starts to ramp up, volatility could eventually return. It’s not really a big factor right now, but don’t be surprised if we see some intraday volatility continue in the coming weeks.

You saw the beginnings of that the last couple of weeks, where we’d be up significantly in the morning and sell back off. Or be down significantly in the morning and rally back. We’re probably going to see that pattern continue because besides awaiting the next steps on the infrastructure bill, the market still awaits clarity from the Fed. And even though this bill is exciting, that clarity from the Fed is arguably the big cloud that everything else operates underneath right now as far as the market is concerned.

For instance, yesterday Kansas City Fed President Esther George said it was time for the central bank to begin pulling back its bond-buying program. There’s been similar language from other Fed officials recently. No single person at the Fed sets policy, but at least a few seem to be chomping at the bit, so to speak, to start tapering.

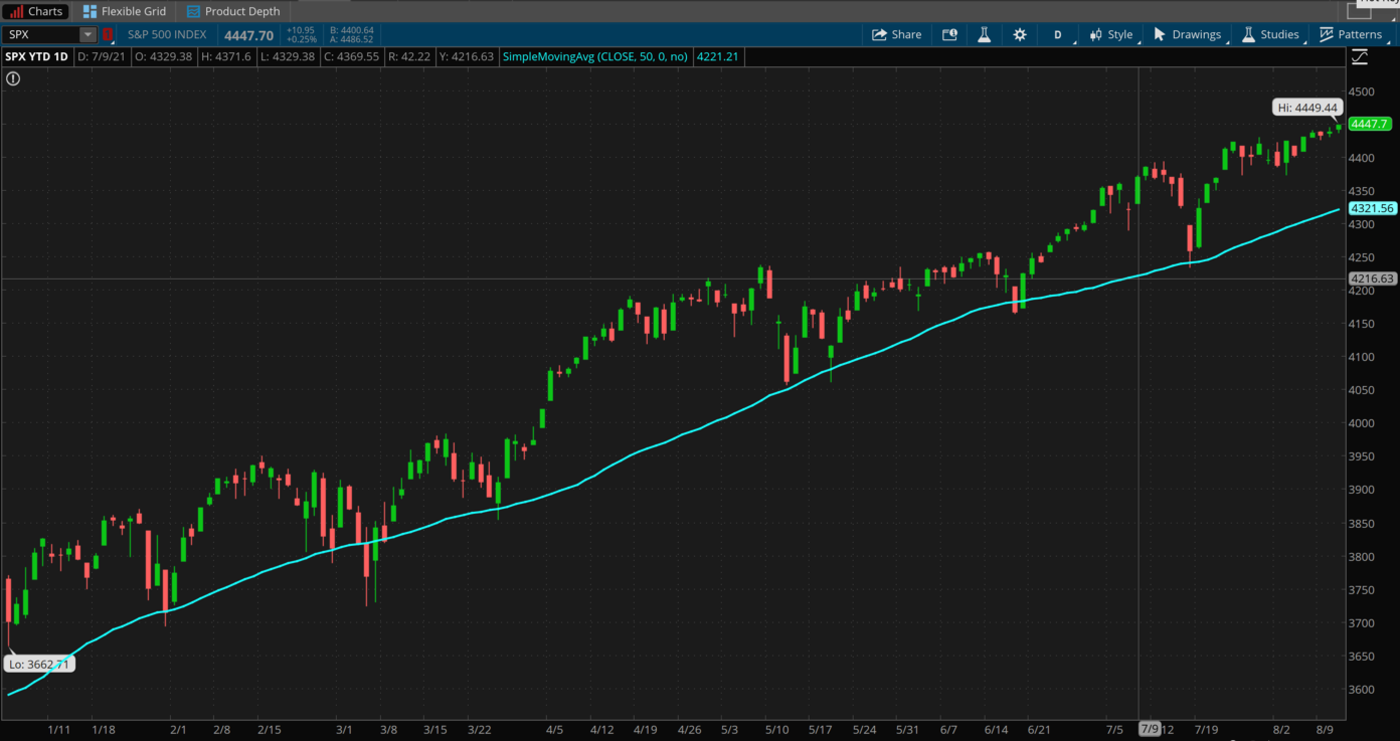

CHART OF THE DAY: WHAT’S YOUR 50? Though it’s been a while since the S&P 500 Index (SPX—candlestick) suffered a setback, it’s worth noting that mid-month has been tough for it the last few months. That doesn’t mean there’s a selloff ahead, only that you might want to prepare for one if the pattern persists. Assuming things run into trouble, the level to watch is the 50-day moving average (blue line), which currently rests about 3% below the index. That’s pretty much how far things fell in mid-July when the last selloff occurred before the SPX bounced off of that 50-day MA. Data Source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

A Tale Of Two Earnings And Reopening: Two earnings reports out this week help illustrate how people are still eager to get out of their homes despite Delta variant fears. First, Ebay EBAY gave some muted Q3 guidance because people don’t want to stay home checking online auctions. Then dating site Bumble BMBL did better than expected, also because people want to get out. This can show us two things. First, there’s still a lot of pent-up demand to get back to normal. Number two, EBAY might give us insight into what to expect from other retailers, especially those who rely a lot on digital, when retail earnings season gets underway in earnest next week.

Patience Could Be A Virtue With Infrastructure Stocks: Companies like U.S. Steel X, General Electric GE, and Cleveland-Cliffs CLF all had a nice bump this week on the Senate’s infrastructure bill passage. But remember, this isn’t something that’s going to hit the economy for a while. If you’re looking longer term as an investor and you want to own these stocks for a few years, that’s probably where the bigger opportunity is. In the shorter term, you could see an initial bump, and then maybe a little bit of a flattening out.

It could take six or nine months before you actually start to see some shovel-ready projects or even some of the architectural and engineering firms starting to lay all of this out. It is a huge undertaking. Long term, it could have a big impact on some of those companies. But again, it takes a while to get going.

Not Enough Gloom For Gold To Shine? The traditional clash between market fundamentalists and chart technicians came to a head over gold at the skirmish zone of $1,670 an ounce range. Why $1,670? For “technical” traders, that price marks the critical 61.8% Fibonacci retracement level. If this makes no sense to you at all, as it is slightly complex for the uninitiated, just assume that it’s nearing the uncle point where either bulls pile in and prevail (which it appears they did), or they flee, dumping their long positions as bears overrun them.

The $1,670 range was tested twice before, in March, with bulls gaining the upper hand each time. But even that wasn’t enough to stem the tide of “risk-on” sentiment, leading to the fundamental vs technical commotion before yesterday’s Consumer Price Index and today’s Producer Price Index reports—both inflationary gauges; and gold, a traditional inflationary hedge. With not enough gloom to glide gold’s flight, will this week’s inflationary readings cause gold to shine or sizzle?

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image by Alessandro D'Andrea from Pixabay

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.