The Forward Guidance Trap

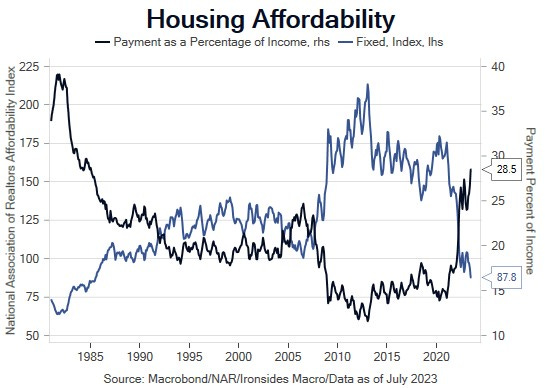

Figure 1: Monetary policy has degraded housing affordability to the worst levels since the mid ‘80s. This is unfortunate given household formations increasing to the best levels in decades due to demographics.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.