Wall Street got some clarification from the Fed yesterday after a long wait, which helps explain why major indices are painted green this morning. The Fed basically said the economy is doing better, and that’s good to hear.

Volatility is down, with the Cboe Volatility Index (VIX) falling back under 20 after soaring above 25 during Monday’s selloff. A dip in VIX could signal a clearer road to stock market gains, as many investors still appear to be bullish about the U.S. stock market vs. other possible places to park their cash.

In a less helpful bit of news, 351,000 Americans filed for jobless claims last week, vs. 320,000 that analysts had expected and an increase from 332,000 the previous week. That could indicate continued labor shortages for some companies and the service sectors.

Today's Best Finance Deals

Don’t Dismiss Evergrande Too Quickly

Earlier, in Asia, beleaguered Chinese property developer Evergrande said it would start making payments on some of its debt. However, Beijing is sending out signals that it might let the real estate giant fail on some of its obligations, namely those held by investors overseas.

It’s interesting how the Evergrande worries have faded into the background a bit here after slamming Wall Street earlier this week. It just goes to show how important the Fed is. However, don’t dismiss the Evergrande story. For now, it seems to be in the background, but these stories have a habit of coming back.

In other news, there might be interest in a scheduled meeting today with the White House on producers and users of semiconductors, of which there has been a shortage affecting everything from computers to cars. Workers have been curtailed by the pandemic while demand has increased.

Demand also is on the increase for homes, judging by the very nice quarter just reported by KB Home KBH. The homebuilding company had supply chain issues, but revenue still rose 47%. In other earnings news, Blackberry BB shares were also rising this morning after an earnings beat.

There’s also a bunch of key earnings reports ahead later, including Costco COST and Nike NKE, which could give insight into the health of both U.S. and Chinese consumers.

Next Jobs Report Could Help Determine Fed’s Taper Timing

A decent September jobs report probably means the Fed could announce a slight loosening of the economy’s training wheels in November.

That’s basically what Fed Chairman Jerome Powell told us at his press conference yesterday after the Fed’s meeting, and so far, the market seems OK with that. While the major indices pulled back a bit from their peaks after Powell spoke, Wednesday was still a very strong day.

Leading sectors included Financials—which would conceivably benefit from higher rates—and Energy. Both are so-called “cyclical” sectors that tend to do better when the economy is growing, and a taper announcement might be seen as confirmation from the Fed that things are going well.

Getting back to Powell, what he said in his press conference is that he thinks “the test is all but met” for a taper of the Fed’s $120 billion a month bond-buying program, but he needs to see a “decent” jobs report. The report—due Friday, Oct. 8—now arguably becomes even more important than it already was following relatively soft August jobs data that reflected the Delta variant’s impact on travel and leisure hiring.

As Powell also said, many Fed officials think the test has already been met to taper. To some analysts, the chairman’s words signaled that a taper announcement is all but baked in at the November meeting, barring some major new bearish development between now and then.

It’s unlikely most investors really believe Powell about a taper not being connected to future hikes. After all, more Fed officials now expect a 2022 rate hike than back in June, according to the Fed’s “dot plot” issued yesterday. (The dot plot is a table released four times annually that shows Fed members’ projections for rates in coming years).

Debate Over 2022 Vs. 2023 Rate Hike Underway At Fed

It’s going to be very interesting to watch this debate shape up next year about whether to hike in 2022 or 2023 because Fed officials look very divided now. Of course, as Powell reminded us, so much can change in just a year, so it’s worth taking the dot plot with a major grain of salt.

Just for historic perspective, it was roughly two years between the start of tapering in 2013 and the first-rate hike in late 2015. It’s hard to believe it would take that long this time because the pandemic that caused this economic mess had nothing to do with any problems in the U.S. financial markets. Covid was an unrelated blow from out of the blue, and if it starts to ease meaningfully, we can hopefully expect the economy to be at least as strong as it was in early 2020 before it began.

As a reminder, the Fed funds rate right before Covid was 1.75% and the benchmark 10-year yield was just below 2%. Unemployment—now 5.2%—was below 4% back then. The Fed anticipates unemployment moving back under 4% by the end of next year.

Returning to the present day, the 10-year yield actually gave up a little ground to 1.3% after the Fed meeting. That level has been kind of the fulcrum lately, but we might see yields start rising if the employment data look good. In fact, by this morning the yield popped to 1.35%.

Right now there’s a lot of technical resistance in the 1.37% to 1.38% range. The dollar index did rise after the Fed meeting, as you might expect it to anytime the Fed hints at a more hawkish policy. At 93.45, the dollar index is near a one-year high.

Other Economic News Ahead

The Fed’s announcement yesterday clearly had the biggest impact this week. But some earnings ahead could be worth watching, too.

After the closing bell today, Costco COST might garner some attention when it opens its books. The warehouse retailer could be seen as a bellwether due to the double-whammy of rising costs for hourly wage workers that may cut into margins and supply shortages that have had a ripple effect on retailers. Its stock has gained more than 37% over the past 12 months, including a gain of more than 20% so far in 2021.

Athletic gear maker Nike Inc. NKE has created high expectations for its fiscal 2022 first-quarter results as well. Its stock has been running fast, gaining nearly 40% over the past 12 months, including an increase of 11.7% for the year to date. The Dow Jones Industrial Average ($DJI) component—which is expected to release earnings after today’s close—has said it expects to generate $50 billion in sales this year, a jump of 12% from its 2020 total. NKE is often a good barometer of the Chinese economy since it does so much business there.

A bit lost in the market euphoria yesterday was a disappointing earnings report from FedEx FDX.

The shipping giant posted weaker-than-expected quarterly earnings due to supply chain disruptions and labor scarcities that weighed on results. FDX is traditionally seen as a good barometer of consumer demand, but these supply chain issues might be making it harder to get a really clear picture, at least for now.

General Mills GIS posted solid earnings Wednesday, giving hope to the beleaguered package-food company stocks.

On Friday, August new home sales data are scheduled and Fed Chairman Jerome Powell is scheduled to speak about the pandemic. Traders will again likely be parsing each syllable he utters in hopes of any elaboration on his tapering “soon” comments from Wednesday.

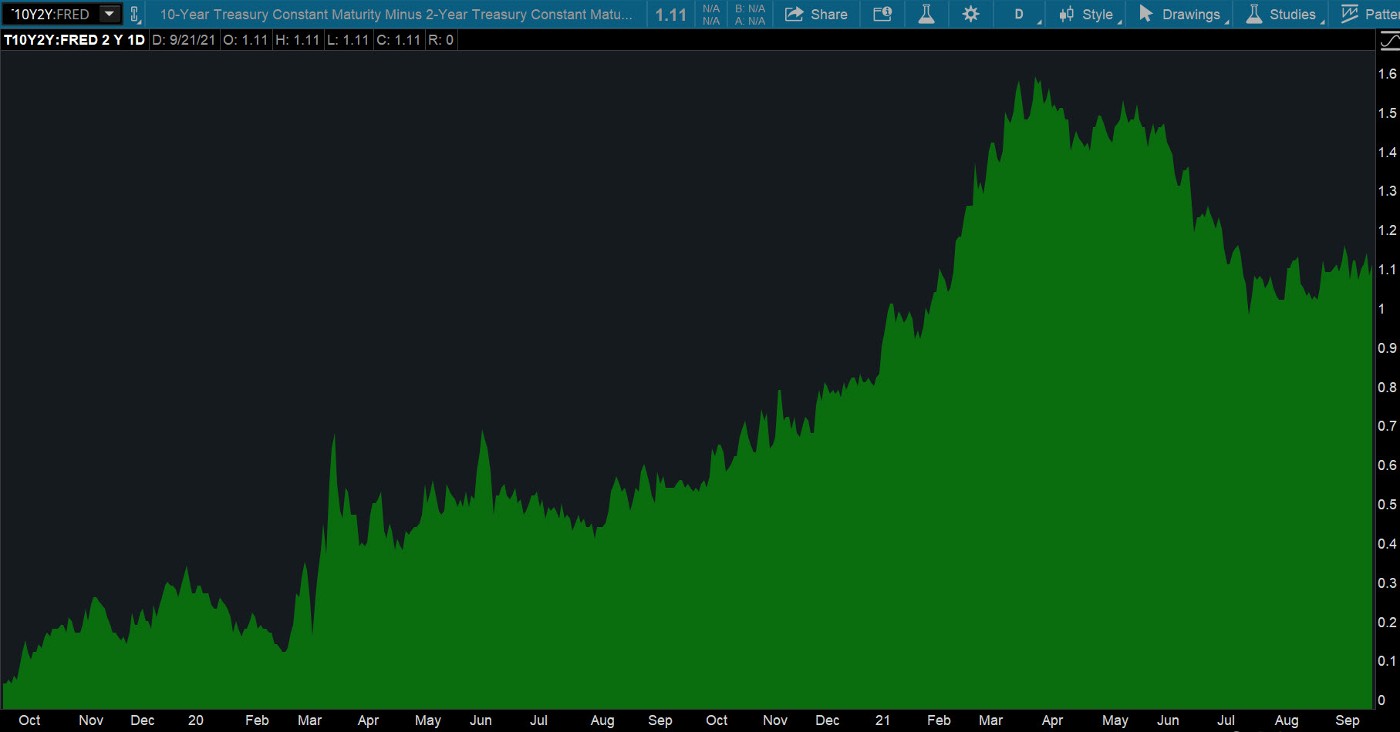

CHART OF THE DAY: THE SHAPE OF THE YIELD CURVE. When the 10-year and two-year yields move further apart, it could be a sign of economic growth. In the last couple of months, the relationship between the two yields doesn’t provide much of an indication of where the economy might be heading. Data source: Federal Reserve FRED database. FRED® is a registered trademark of the Federal Reserve Bank of St. Louis. The Federal Reserve Bank of St. Louis does not sponsor or endorse and is not affiliated with TD Ameritrade. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

To Travel Is To Live. Or at least to make up for lost revenue. The Biden administration has announced it’s lifting travel restrictions starting in November for foreigners who are fully vaccinated against the coronavirus. The move reopens the U.S. following an 18-month travel ban from 33 countries, including members of the European Union, China, Iran, South Africa, Brazil, and India.

November won’t come soon enough for the U.S. tourism industry, which suffered $500 billion in losses due to severe declines in travel expenditures in 2020, according to the U.S. Travel Association, a trade group that promotes travel to and within the U.S.

To put the losses in another perspective, the group calculates that for each week that travel restrictions continue to remain in place, the U.S. economy is losing $1.5 billion in spending just from Canada, the European Union, and the U.K., or enough money to support 10,000 American jobs.

The New York State Comptroller estimates that in New York City alone, the lack of tourists since the pandemic started wiped out 89,000 jobs and resulted in a loss of more than $60 billion in revenue.

Grey And Shine: The greyness of silver kind of symbolizes the fuzzy and undecided character of the metal itself. A strange monetary and industrial metal hybrid, it’s kind of interesting how some investors jump into silver when economic growth is slowing and dump it when times are good, while other investors load up on the metal when times are good only to sell it when times are gloomy. Silver futures’ (/SI) volatile back and forth motion is well into its 13th month. The big picture, though, shows the metal retracing not even 50% of its entire move up from its March 2020 pandemic low. From a trader’s lens, /SI can retrace as much as a 61.8%—between $18 to $20 an ounce—before hardcore gold and silver bugs start feeling the heaviness of their metals. So, the trend, ironically, appears both sideways in the near-term and up in the longer-term, if you read the charts.

Looking to the future, you have to wonder whether analysts who are bullish on the metal are right about silver’s role in the coming “low carbon economy”; whether it might play a critical role in solar and wind power; and whether its high conductivity will sustain its demand in electronics production. Then you have to ask whether enough silver is being mined and produced to satisfy both the industrial and (don’t forget) monetary demand in the coming years.

Housing Market Softening? Maybe a tad bit. The housing market got a lot of attention earlier this year as bidding wars among buyers sent home prices on a tear. But yesterday’s existing-home sales data suggests that the housing market may be showing signs of cooling down. Home sales last month declined by about 2% from the month before and 1.5% from a year ago, according to the National Association of Realtors. Home prices are also growing at a slower rate than we saw earlier this year.

A little cooling may be a good thing given that the higher prices may have made it difficult for some potential buyers to pay those higher prices. But don’t rule out the homebuilding sector. Home sales are still growing—just at a slower pace. And single-family housing starts rose last month. So as prices decline a bit, we could see that give potential home buyers more of a chance to jump in. One month is never a trend, so consider watching these numbers closely over time.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image by Paul Brennan from Pixabay

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.