Friday’s momentum melted away like snow in the March sun. Then it appeared to come back, at least for parts of Wall Street. The Nasdaq (COMP) isn’t one of them.

Things didn’t start out all over the place like they are now. Major indices initially rose in sync during the overnight session after the Senate passed the $1.9 trillion stimulus bill. The full-service rally didn’t last. Weakness in Asian markets and the 10-year Treasury yield climbing back above 1.6% might have done the trick. The Nasdaq (COMP), home of many Tech stocks, seems to be taking it worst in the early going. Tesla Inc TSLA and Apple Inc AAPL are down in pre-market trading.

One reason we rallied so much Friday was a leveling out in the yield. Now that it’s climbing again (for the moment), Tech stocks may face a headwind from fears that higher yields point to potential higher inflation. The bond market is telling us there’s a lot of money in the system as more people get back to work. And with all this money coming back in, people are concerned, especially with U.S. debt now more than 100% of gross domestic product (GDP).

Finding Some Separation

There may be some bifurcation developing on Wall Street today. Tech stocks are getting whacked, but these higher interest rates may not be the worst thing in the world for banks. That means the Dow Jones Industrial Average ($DJI) and the S&P 500 Index (SPX) could be separating themselves a bit from the COMP. The Russell 2000 (RUT) and the $DJI turned slightly higher as the opening bell approached. Remember, the RUT is where many mid-sized banks trade.

We’re in that time between earnings seasons where corporate news sometimes gets thin, meaning the market can get led around by developments outside the financial world. Stimulus is one of those, with the House expected to vote this week. However, most of that appears to be built into stock prices already, so new catalysts might be needed for a sense of direction. Each time we go up, sellers appear, and any downward moves get met by “buy the dippers.” For now, anyway, major indices could be range-bound unless there’s some big outside news.

Some of that outside news could come from across the pond, so to speak, as the European Central Bank (ECB) meets later this week and faces the question of what to do about rising bond yields over there. This happens with the U.S. dollar recently touching three-month highs. The dollar might be getting some help from last Friday’s strong U.S. jobs report.

Don’t forget another feature: Volatility. It could hold the key to this week’s markets. The Cboe Volatility Index (VIX) pulled back Friday from its flirtation with 30, but began the week pointing slightly higher. It’s still below 28, but keep an eye on it. Meanwhile, it would be nice to see some buyers in the Nasdaq. That’s probably got to happen for the market to get back on its feet. They’re the ones that led us here, but now the question for them is, what’s next?

Market Diagnosis: A Case Of Whiplash

If you saw anyone wearing a neck brace on Friday, you probably understood why if you were watching the markets. Wall Street had whiplash all over the place to end the week, with the COMP ending 1.6% higher after being down 2% in the early part of the session.

If you’re trading these markets, it’s probably safe to say more volatility lies ahead, so buckle up (see below). Keep in mind that if you do jump into and out of markets at times like these (not that you have to feel compelled to), you’re going to have times when you’re dead right and other times when you’re dead wrong. That means have a plan if you’re going to be part of it. It’s not against the rules to sell some on the way up, or to hold on when things go against you—even if it can be tough.

What seemed to happen Friday was another “buy the dip” rally after a surprisingly strong February jobs report. The initial read was bearish because yields zoomed higher in the first minutes after the data. It looked like the 10-year yield might be off to the races, but it stabilized and eventually fell from above 1.6% to the mid 1.5% range. That’s still about 15 basis points above where it was a week ago.

Once it became clear that yields were kind of checked, stocks reversed the early losses. The “buy the dip” mentality has worked for years, which helps explain why many people continue to do it. Friday may have been the ultimate example. There was shocking strength by Friday afternoon, and to see that kind of comeback after a huge selloff is encouraging for this coming week.

The big question is how much higher yields might go from here and if Wall Street can get used to it. A lot of selling hit the high-flying growth stocks last week, with Tech taking a nearly 3% haircut overall despite Friday’s solid comeback. There’s a reassessment going on, with many investors taking profit after the long rally in this neighborhood of the market. More on the Tech and Treasury yield relationship below.

Conversation Starters: Inflation And Volatility

A few months ago almost no one was worried about inflation. The main fear was the chance of the economy cratering again as virus cases surged. Then about three weeks ago it was like someone pushed a button and everyone got worried about inflation. It’s almost funny how fast it started to dominate the market conversation.

Another dominant topic that’s probably not going away anytime soon is volatility. Going into Friday, we’d suggested that a close below 25 in the VIX could probably say good things about where stocks went. That’s exactly how it played out, with VIX falling to 24.8 by the end of the day as stocks made their incredible turnaround. But there’s no reason to believe volatility will slow down, and we could continue to see days like Friday right into next week’s Fed meeting.

It’s actually unclear what the Fed could say to calm things down at this point. Fed Chairman Jerome Powell barely said anything in his remarks last week, but the market sold off when he said the dreaded “I” word, or inflation. The Fed meeting is scheduled for March 16–17, but it’s hard to say what the yield situation will be by then.

One thing we will know more about is inflation, however. This week brings the February consumer price index on Wednesday and producer prices on Friday. These should be two of the more closely watched economic reports of the month, and we’ll discuss expectations tomorrow. Year-over-year CPI rose 1.4% in January, with core CPI rising 1.6%. Both are below the Fed’s 2% target, but the Fed typically looks more closely at personal consumption expenditure (PCE) prices for its inflation read.

There’s not much on the earnings calendar this week, which figures considering the time of year. However, Campbell Soup Company CPB and Oracle Corporation ORCL both report on Wednesday, representing very different segments of the economy. Of course, earnings aren’t the only type of company events. The big three U.S. telecom companies all host investor days this week. Verizon Communications Inc. VZ starts things off on Wednesday, followed by T-Mobile US Inc TMUS on Thursday and AT&T Inc. T on Friday.

On the economy, it was very encouraging to see a rise in retail jobs in the February payrolls report. That’s seasonally unusual and could speak to a strong reopening trend.

Energy Takes Weekly Prize Again As Supplies Seen Tighter

In the sector watch Friday, Energy powered well ahead of the field; the rest were playing for second place. Energy has gone from C-student last year to the top of the class. What’s happening? Crude oil supplies—already expected to tighten in what’s expected to be a vibrant post-pandemic economy—may be getting even tighter as, in a surprise move this week, OPEC+ members agreed to keep output steady. That means continuing its January pledge to dial back the spigot.

And remember another thing that may be working in Energy’s favor: Last year’s pandemic had some producers (especially in the U.S.) turning off the taps. You can’t turn those things back on like a light switch. It takes time, money, and effort, so that could put a lid on how fast supplies come back from Texas.

What a turn of events for Energy. It wasn’t too long ago that tanks and tankers across the globe were full to the brim, with nowhere to offload it. Prices went from cratered to—dare we say it—eyeing the $70 per barrel mark. Crude hit $66 today before pulling back slightly. If you’re looking for a sign of what the market’s expecting, the Energy sector (IXE) might be it.

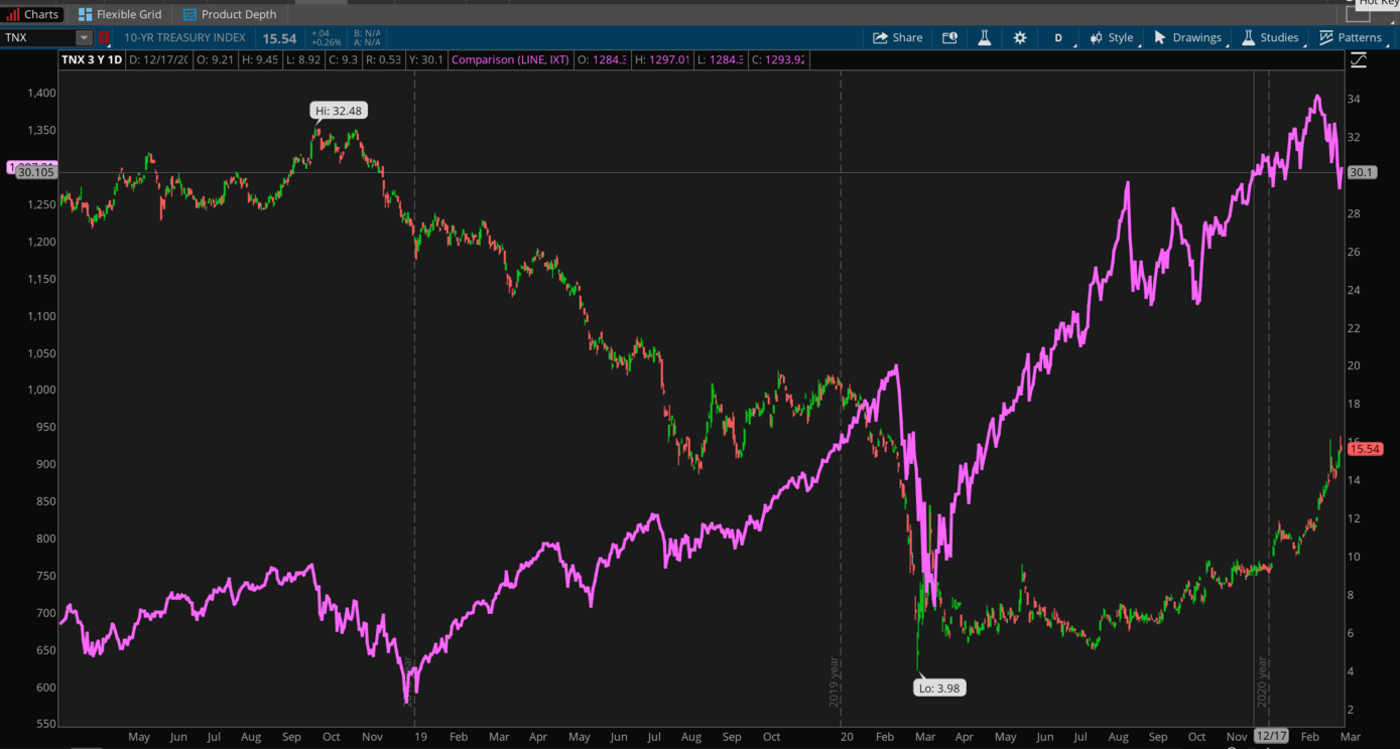

CHART OF THE DAY: DANCE OF THE TREASURIES AND TECH. This three-year chart shows how the Tech sector (IXT—purple line) has twice been hit by higher 10-year yields (TNX—candlestick). First in late 2018 (see left side of chart), and more recently in the last few weeks. However, recent history shows Tech has generally run hot as long as the 10-year stays below around 2.5%. Data Sources: Cboe, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

From the “Good News is Bad” Department: Some analysts expect jobs numbers to keep improving this year thanks to reopening. That would typically be good news for stocks, but right now it’s playing into the hands of the bears. Certainly when you see this kind of employment situation, with 379,000 new jobs in February, and January getting revised higher, it’s a little bit of an arrow in the quiver for those who have inflation fears.

On top of a lot of the other good news we are getting, and on top of the fact it does look like we are closer to a stimulus plan, there’s also a lot of money continuing to slosh around in the economy that could give some credence to these inflation fears. Obviously, inflation doesn’t usually hurt some sectors as much as others. In fact, it can actually help the cyclical sectors that tend to do well in an environment of economic recovery. That could explain why two of the only sectors on the rise last week were Energy and Financials.

Strange Days: Though it’s tempting to try to come away from a big monthly jobs report with a couple of key takeaways, it’s dangerous to make any major conclusions in this strange environment where some states are emerging faster than others from the pandemic. Friday’s February report was a perfect example. For instance, education jobs were lost pretty significantly across the country in February, but the month before almost the same amount of education jobs were gained across the country. It’s really tough to figure out as the states open differently what is actually going on. That all said, the trend is positive. Ultimately, reopening and getting back to normal is a good thing, even if we get some hiccups along the way like we are now from rising Treasury yields.

While the more normalized yield situation is taking a bite out of growth stocks, it’s worth remembering that many of these companies now getting dinged did just fine in the 2016–2018 period where yields were much higher than they are now and the Fed was actually raising rates. We’re having some growing pains now, which could last a while longer. Ultimately, if inflation gets back toward the Fed’s 2% goal, it wouldn’t surprise some analysts to see the 10-year yield roughly match inflation.

Comfort Spot for Tech: Does it seem hard to believe Tech can thrive in a rising rate environment? Well, between mid-2016 and mid-2018, shares of Apple Inc AAPL basically doubled. In that same period, the 10-year yield rose from 2.36% to 2.84%. Meaning the biggest Tech company and yields rose in conjunction. The Tech sector as a whole didn’t do quite as well as AAPL, but still climbed a very solid 60% over that time frame—which happened to also correspond with regular Fed rate hikes. Now, you could poke holes in this argument by noting that these are cherry-picked dates (AAPL and Tech both got hammered in late 2018 after yields rose above 3%), and that shares of both AAPL and Tech weren’t as highly valued then as now. Points taken.

Over the last 10 years, Tech has typically performed best in years when the 10-year yield stayed below 2.5%. Rising yields corresponded with weakness in Tech back in 2014 and 2015, as well as in the late-2018 decline. However, at this point we’re nowhere near a level for the 10-year where yields have historically hurt the sector. Also, the Fed still has short-term borrowing costs at basically zero, with no rate hikes in the picture. What we’re probably seeing in Tech is a reassessment by a lot of investors wondering if the sky-high valuations are justified in a rising yield environment. Don’t count Tech out, especially if overall weakness in the market continues. That might send people scurrying back into some of the “mega-cap” stocks they’re familiar with. We saw the same thing a year ago when the pandemic hit.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Jorge Alcala on Unsplash

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.