In 2019, former financial professional Keith Gill, who goes by “Roaring Kitty” on Reddit, began a movement that pushed GameStop Corporation’s GME stock price as high as $513.12 in premarket trade Jan. 28, after which numerous brokers made the controversial decision to limit trades, creating a synthetic imbalance that caused the stock to plummet to a low of $112.25 in regular trade.

As part of the development, Benzinga chatted with Kris Sidial, a former institutional trader and the co-chief investment officer of The Ambrus Group, a volatility arbitrage fund that looks to exploit changing market structure dynamics.

Dynamics At Play: Alongside speculative commentary on online forums like WallStreetBets, shares of GameStop were further primed for upside after Ryan Cohen, the co-founder at Chewy Inc CHWY joined the company as a board member.

On the other side of the trade was Citron Research and Melvin Capital, part of a sector in the hedge fund industry that looks to capitalize on the downside of distressed companies and debt.

As news of Cohen’s involvement circulated, shares of the highly shorted retailer began rising as funds looked to reduce their exposure and were buying to close positions.

“From a pure delta one persepctive, this was a short squeeze,” Sidial told Benzinga.

“You have distressed debt hedge funds that focus on shorting these types of companies. Melvin Capital is the one that is singled out due to the media, but they aren’t the only ones.”

Market participants added to the crash-up dynamics. Retail investors aggressively bought stock and short-term call options, while institutional investors further took advantage of the momentum and dislocations.

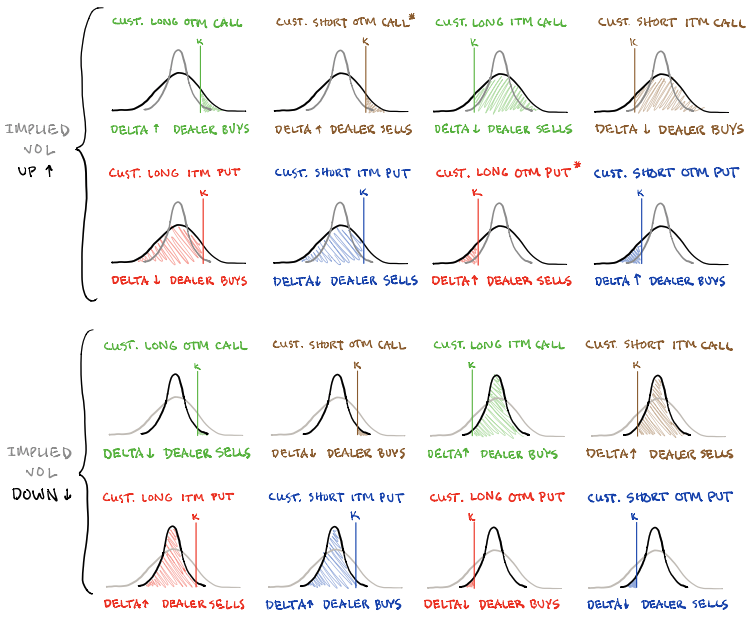

“You have this dynamic in the derivatives market where there is a gamma squeeze when people are buying way far out-of-the-money calls, and dealers reflexively have to hedge off their risk,” Sidial said.

“It causes a cascading reaction, moving the stock price up because dealers are short calls and they have to buy stock when the delta moves a specific way.”

The participation in the stock on the institutional side has not received much attention, he said.

“We’ve noticed that some of the flow is more institutional,” he said in reference to activity on the level two and three order books, which are electronic lists of buy and sell orders for a particular security.

“You have certain prop guys and other hedge funds that understand what’s going on, and they’re trying to take advantage of it, as well.”

This institutional activity disrupted traditional correlations and caused shares of distressed debt assets like GameStop, BlackBerry Ltd BB, and AMC Entertainment Holdings Inc AMC to trade in-line with each other.

“This was not some WallStreetBet user, … if you look at how some of these things were moving premarket, you would see GME drop like 2%, BB’s best bid would drop and AMC’s best bid would drop. That’s an algo.”

The takeaway: although the WallStreetBets crowd is getting most of the blame, institutions are also at fault for the volatility.

Dealers, Hedge Funds Go ‘Ouch’: Liquidity providers and hedge funds were both hurt as a result of GameStop volatility, Sidial said.

“You have to look at what took place, the time frame, and how it took place. There were GME $57 calls that were the furthest strikes at one point. If you sold those calls, you got blown out the water. The stock is now trading at $350.”

The dynamics that transpired in GameStop can be traced back to factors like Federal Reserve stabilization efforts and low rates, which incentivize risk taking.

“The growth of structured products, passive investing, the regulatory standpoint that’s been implemented with Dodd-Frank and dealers needing to hedge off their risk more frequently than not” are all part of a regime change that’s affected the stability of markets, Sidial said.

“These dislocations happen quite frequently in small windows, and it offers the potential for large outlier events,” like the equity bust and boom of 2020, he said.

“Strength and fragility are two completely different components. The market could be strong, but fragile.”

Pictured: Newfound Research unpacks market drivers, implications of liquidity.

The aforementioned dynamics of dealers’ risk exposure to direction and volatility causes violent crash dynamics to transpire.

In February 2020, one-sidedness in the market by yield-seeking participants like target date funds — such as mutual funds — selling far out-of-the money puts on the S&P 500 exacerbated volatility. So did customers looking to buy puts in an increasing fashion for downside exposure.

Pictured: SqueezeMetrics highlights implications of volatility, direction and moneyness.

“We’re in there buying puts, dealers are short puts and short stock,” Sidial said in a discussion on rising delta and volatility forcing dealers to sell into weakness to hedge.

“As people reach for those downside puts on SPX, it now reflexively has another implication on increasing volatility. Well, all those people that are carrying short volatility exposure in their book are losing money.”

In all, a new regime with knock-on effects is forming solely due to positioning in the market.

‘Something Needs To Be Done’: Last week, brokers like Robinhood, popularized due to its no-cost, gamified investing platform, came under scrutiny for halting the opening of positions in GameStop, AMC and Koss Corporation KOSS.

That’s because one, it takes nearly two days to settle as stock certificates are transferred between brokers, and two, the cost to settle rose as the Depository Trust & Clearing Corporation’s collateral requirements inflated due to volatility, among other variables.

“A broker is paid to facilitate trade. Some brokers and dealers are crossing the bid and ask spread between flow, between market participants, making money on that, and some still charge a commission,” Sidial said in a discussion on clearing and broker solvency.

“This is not the market participants' problem, they paid to play. It’s the broker’s problem, from an operational standpoint, to make sure that these things are in check.”

Sidial added that preventing trades is a slippery slope, as it opens the door for similar decisions during other periods of volatility.

It induces one-sided synthetic imbalances. For example, after brokers limited trade on GameStop to only closing orders, shares of the retailer fell nearly 70%, which led to speculation that this was collusion with liquidity providers like Citadel, a customer of Robinhood overflow. The company was in the news for investing in Melvin Capital after the firm’s short bets went awry.

“What if we go risk-off and the market’s down 25%,” the trader added in a conversation involving the SEC or FINRA. “Does this open pandora’s box for brokers to say, ‘well, you know, you guys can’t sell Apple stock?'"

An alternative solution is for exchanges to halt the stock completely, preventing the formation of imbalances.

“If you can’t sell, at what point are we not in a free market? Now, it’s a completely synthetic, manipulated market.”

For more on changing market structure dynamics, Sidial and the Ambrus Group, click here.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.