The following post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga.

Since its establishment in 2014 by founding company Fortress Biotech, Inc. (NASDAQ:FBIO), biopharmaceutical company Checkpoint Therapeutics (NASDAQ:CKPT) has focused its research on the development of clinical-stage immunotherapies and targeted therapies for a variety of solid tumor indications, including skin and lung cancer.

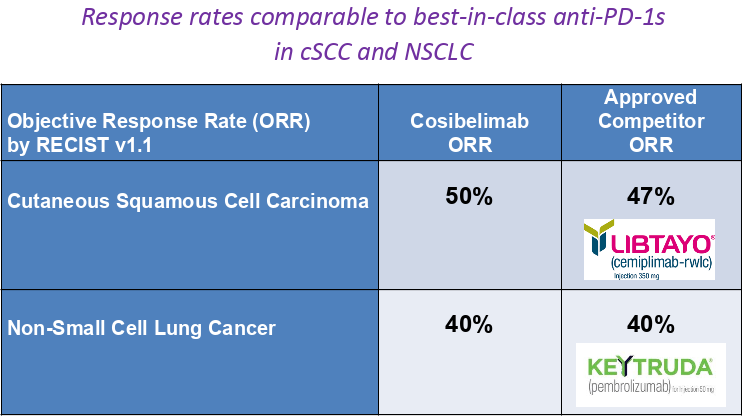

In September of last year, Checkpoint announced that its research efforts have yielded promising results for its lead PD-L1 checkpoint inhibitor, cosibelimab, which is actively enrolling a pivotal clinical trial for the treatment of cutaneous squamous cell carcinoma (cSCC), the second most common form of skin cancer. Preliminary clinical results for cosibelimab have shown similar efficacy rates to Libtayo, the only FDA-approved treatment for metastatic or locally advanced cSCC. This could open up a path to what analysts expect to be a $1 to $2 billion annual cSCC treatment market as well as an initial entry point to penetrating the rapidly growing $25 billion annual market for this class of checkpoint inhibitors across all cancer types.

President and CEO of Checkpoint Therapeutics James Oliviero sees this strategy of innovative treatment alternatives as the company’s core strength.

“Checkpoint is a simple story of developing novel, differentiated products with validated targets in enormous multi-billion dollar markets,” said Oliviero in a recent interview. “Introducing a differentiated product at a lower, market disrupting price point can generate hundreds of millions in annual sales while providing patients worldwide with better access to a potential life-saving class of therapy.”

A Targeted Aim

According to Oliviero, Checkpoint’s near-term outlook on cosibelimab is directed squarely on disrupting the market exclusivity enjoyed by Libtayo, developed by Regeneron Pharmaceuticals (NASDAQ:REGN) in the U.S. and Sanofi (NASDAQ:SNY) internationally.

In addition to entering the cSCC treatment market as a potentially lower-priced alternative to Libtayo, Oliviero points to early clinical evidence for cosibelimab as a potentially more tolerable treatment option for cSCC patients, which he attributes to the way in which the drug specifically targets malignant cells as opposed to targeting the patient's own immuno-receptors.

“Libtayo is an anti-PD-1 antibody, which means it targets PD-1 on the T-cells of the body’s immune system,” he said. “As per recent publications in oncology-focused medical journals, targeting the T-cells with an anti-PD-1 leads to higher rates of moderate to severe immune-related side effects as compared to an anti-PD-L1 antibody (such as cosibelimab) that targets PD-L1 on tumor cells. Checkpoint has observed lower rates of moderate and severe side effects to date in its ongoing study as compared to Libtayo.”

Libtayo, approved by the FDA for use in September 2018, generated $75M in quarterly revenue in the fourth quarter of 2019 (equating to $300M in annualized revenue) for Regeneron and Sanofi. Given this performance, analysts expect the market in cSCC alone could exceed $1 billion.

According to Oliviero, interim trial data presented last year at the European Society for Medical Oncology Congress showed that the first 14 patients with cSCC treated with cosibelimab obtained a 50% objective response rate (indicating tumor shrinkage of 30% or more). These preliminary results compare well to the 47% objective response rate that led to Libtayo’s marketing approval in cSCC. Oliviero also indicated encouraging response rate data were also presented in 25 patients with non-small cell lung cancer.

Cosibelimab Clinical Program Investor Presentation

Checkpoint Therapeutics, April 2020

Should these results remain consistent at the conclusion of the ongoing pivotal cSCC trial, Oliviero voiced optimism that the drug could soon be submitted under a Biologics License Application (BLA) to the U.S. Food and Drug Administration — and similar international regulatory agencies —for marketing as the world’s second cSCC treatment.

Checkpoint’s next interim cSCC data update is planned for the second half of 2020, with full top-line results expected in 2021.

Expansion Opportunities

According to Oliviero, current sales of the entire class of approved anti-PD-1 and anti-PD-L1 checkpoint inhibitors are roughly $25 billion annually. Lung cancer makes up the largest proportion of the sales of this class.

Although Checkpoint has focused on cSCC as its first indication for cosibelimab, Oliviero expressed a long-term intention to submit the treatment for potential use in other oncological manifestations, particularly lung cancer.

“Beyond CSCC, Checkpoint plans to initiate registration (pivotal) studies in non-small cell lung cancer to expand into this $10-plus billion market,” said Oliviero.

Existing approved PD-1 inhibitor treatments for lung cancer currently include Keytruda, from Merck & Co., Inc. (NYSE:MRK), and Opdivo, produced by Bristol-Myers Squibb Company (NYSE:BMY).

However, just this April, Regeneron and Sanofi released promising clinical data in lowering mortality rates among lung cancer patients with tumors exhibiting high expression of a PD-L1 biomarker. Pending success in further trials in lung cancer, the results are encouraging for Checkpoint’s current ambitions for cosibelimab.

“Additionally, combination therapies including an anti-PD-1 or PD-L1 agent are a rapidly emerging approach to improve cancer patients’ outcomes, with hundreds of these studies underway,” Oliviero explained. “Approved combination regimens can conceivably increase the checkpoint inhibitor class to well over $60 billion annually in just a few years, and we believe cosibelimab is a great candidate for these studies given the efficacy and safety profile seen to date.”

Reaching For A New Checkpoint

While Checkpoint is pursuing continued trial data on cosibelimab, the company is also in an active Phase 1 study of a third-generation epidermal growth factor receptor (EGFR) inhibitor, CK-101, which aims to diminish cancer cell growth. Oliviero explained that Checkpoint’s EGFR inhibitor is intended to compete with Tagrisso, a $4 billion annual sales drug produced by AstraZeneca PLC (NYSE:AZN) that interestingly showed an intolerance among 13% of its trial patients, according to Oliviero.

However, in the near-term, Checkpoint’s focus will be on continued efficacy and approval trials for cosibelimab, a strategy that Oliviero maintains should provide a more affordable checkpoint inhibitor treatment alternative throughout the healthcare sector and among patients.

“With near-term data catalysts from the pivotal study in cSCC planned for the second half of 2020 and 2021, we expect increased visibility of our lead program’s near-term market potential,” he said. “While we are confident we can effectively launch and market cosibelimab ourselves, we are also aware that, upon a successful outcome in the ongoing study, cosibelimab would be viewed by large biotechnology and pharmaceutical companies as a near-term revenue opportunity, with the potential to supplement their portfolios of patent-expiring products.”

The preceding post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga. Although the piece is not and should not be construed as editorial content, the sponsored content team works to ensure that any and all information contained within is true and accurate to the best of their knowledge and research. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.