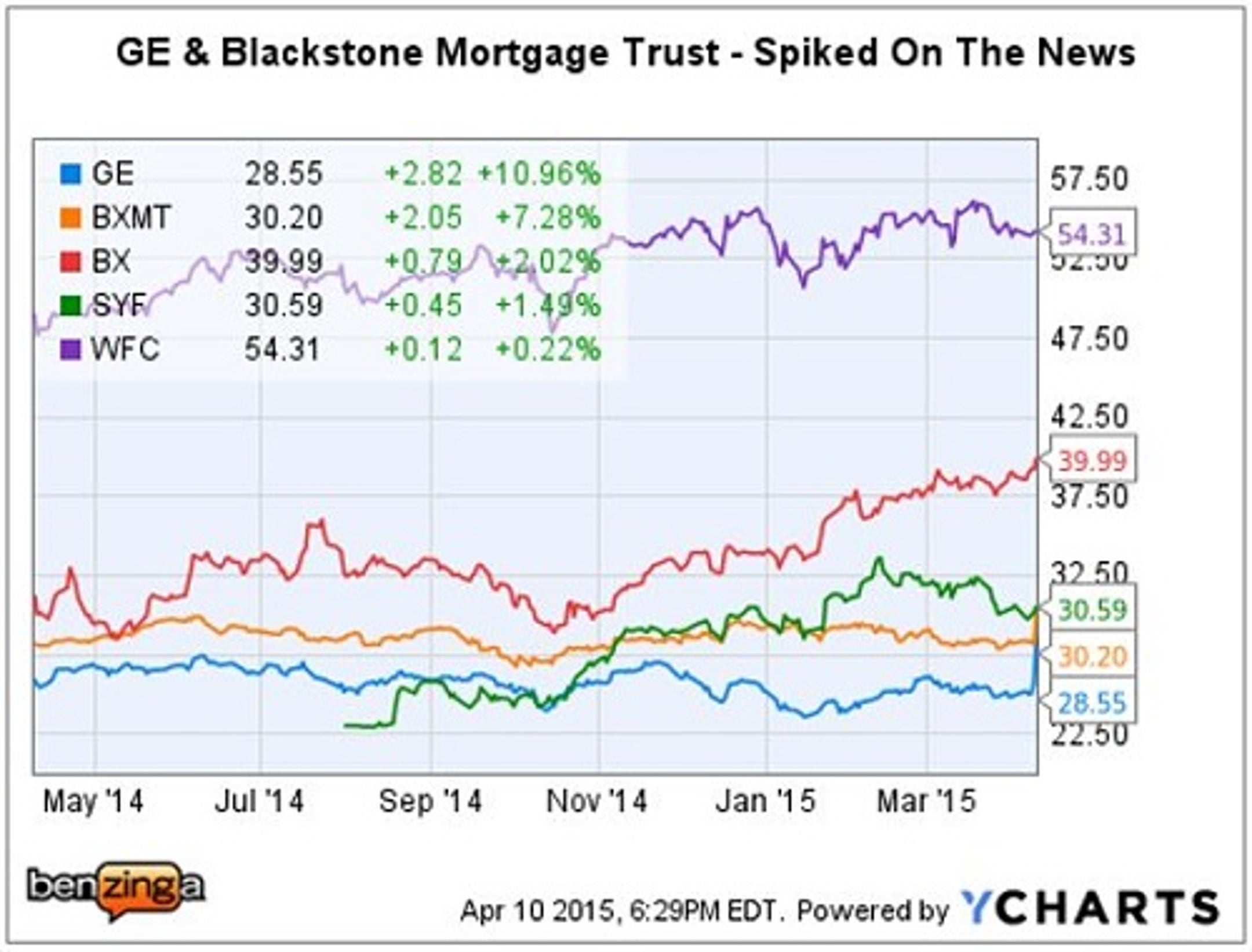

On April 10, Dow 30 stalwart General Electric

GE, hogged most of the headlines generated from selling the majority of its ~$23.5 billion GE Capital real estate asset portfolio to: The Blackstone Group

BX, Wells Fargo

WFC; and notably, a $4.6 billion mortgage portfolio to Blackstone Mortgage Trust

BMXT.

This deal both reinforces GE's core business focus and continues to reduce company exposure to riskier financial and real estate assets -- an initiative spearheaded by GE Capital's Synchrony Financial

consumer finance spinoff this past August.

Mr. Market - Votes Approval

GE - Problem Solved

GE Capital required a liquidity transfusion from the Federal TLGP during the 2008 financial meltdown. This also led to GE's designation as a "systemically important financial institution" (SIFI), and adherence to strict SIFI compliance requirements.

This ongoing transformation will likely result in the SIFI label being removed from GE moving forward.

Notably, GE Capital intends to keep its Aviation Services, Energy Financial Services and Healthcare Equipment Finance arms to support sales of its core industrial manufacturing business groups.

GE intends to utilize proceeds from these sales to fund part of a large stock buy-back.

BX & WFC - Business As Usual

The Wells Fargo reported purchase of a $9 billon international portfolio of GE Capital performing commercial mortgages barely registers a blip, given the size of its balance sheet.

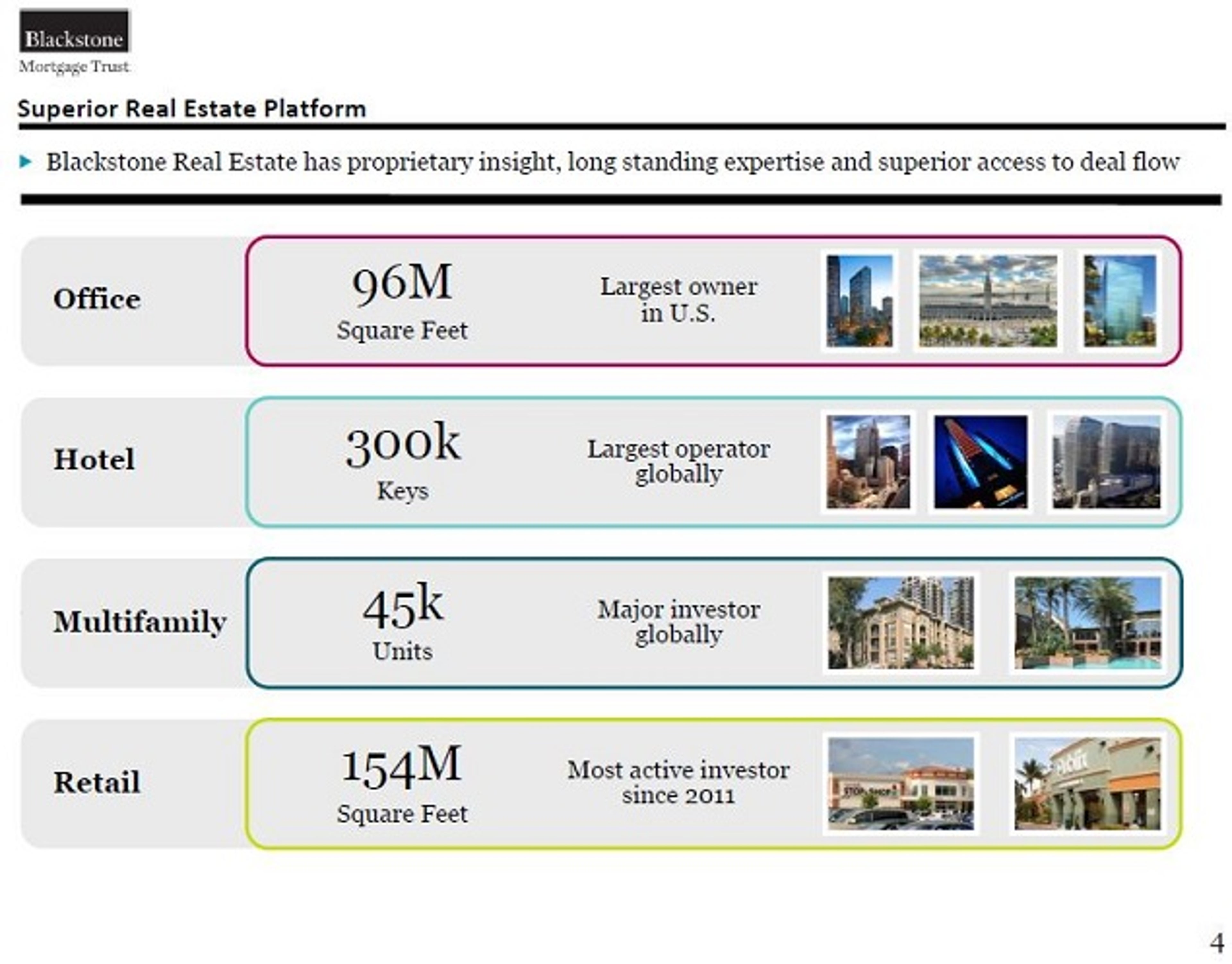

The Blackstone Group will reportedly add $3.3 billion of SoCal, Chicago and Seattle office buildings as well as $2 billion of international properties and commercial mortgages to its industry leading ~$85 million of real estate AUM (assets under management).

http://www.benzinga.com/trading-ideas/long-ideas/15/03/5331305/blackstones-willis-tower-purchase-set-a-record-but-is-it-a-ba

BXMT - Game Changer

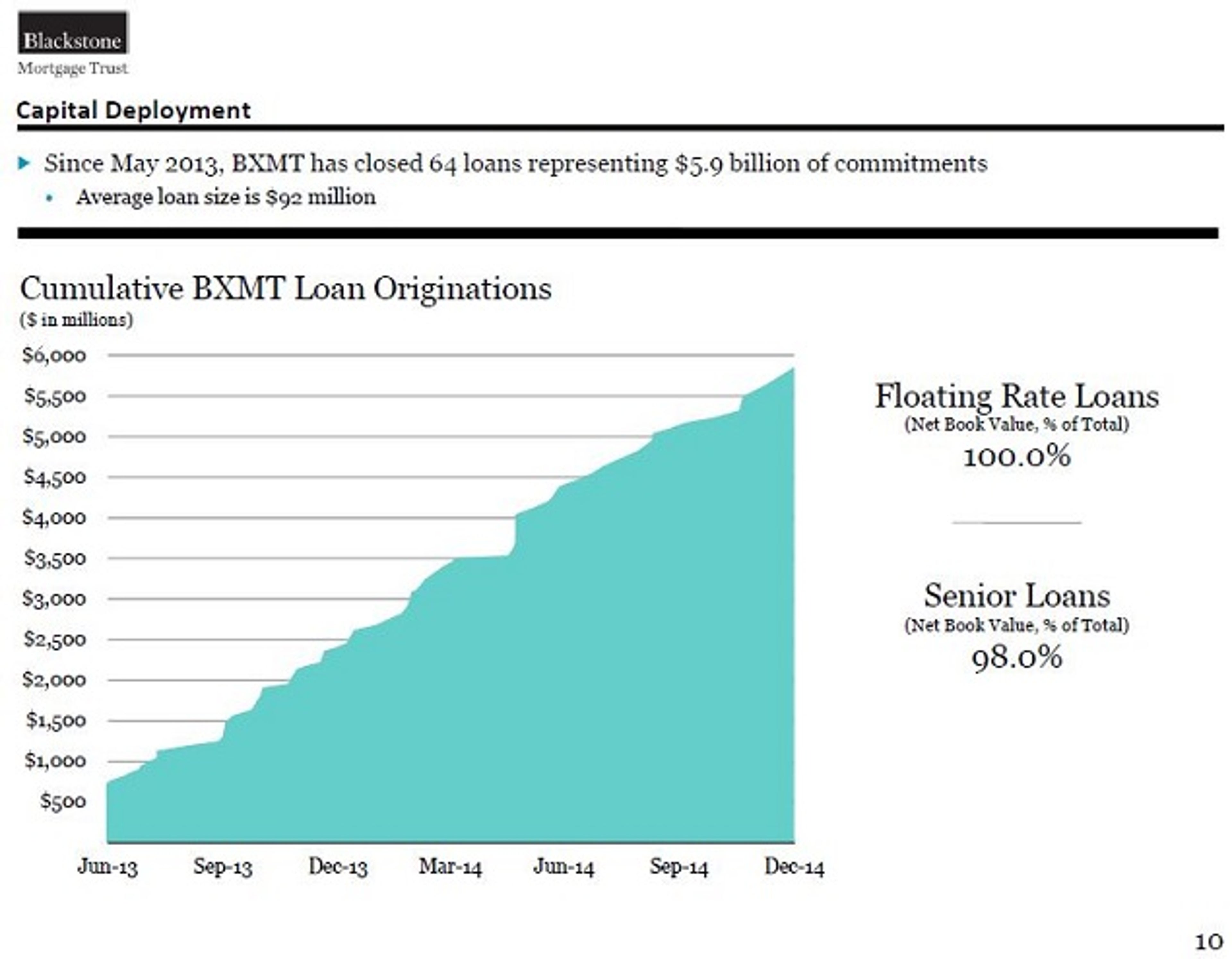

However, the $4.6 billion portion of GE Capital's commercial mortgage portfolio being acquired by $1.65 billion cap Blackstone Mortgage Trust, effectively doubles the size of the existing BXMT portfolio of assets.

Wells Fargo is providing BXMT with a $4 billion acquisition financing package of which $3.8 billion will be funded at closing, the balance will be funded with a combination of BXMT cash on hand and/or an additional capital raise.

Blackstone "expects the acquisition to result in a stabilized $0.24 - $0.28 accretion to annual Core EPS, benefiting from an attractive average portfolio credit spread of 4.21% combined with an efficient financing structure."

Blackstone Mortgage leverage will increase 50 percent, from a fairly modest 2x debt to equity ratio, to 3x debt to equity, as a result of this one large transaction.

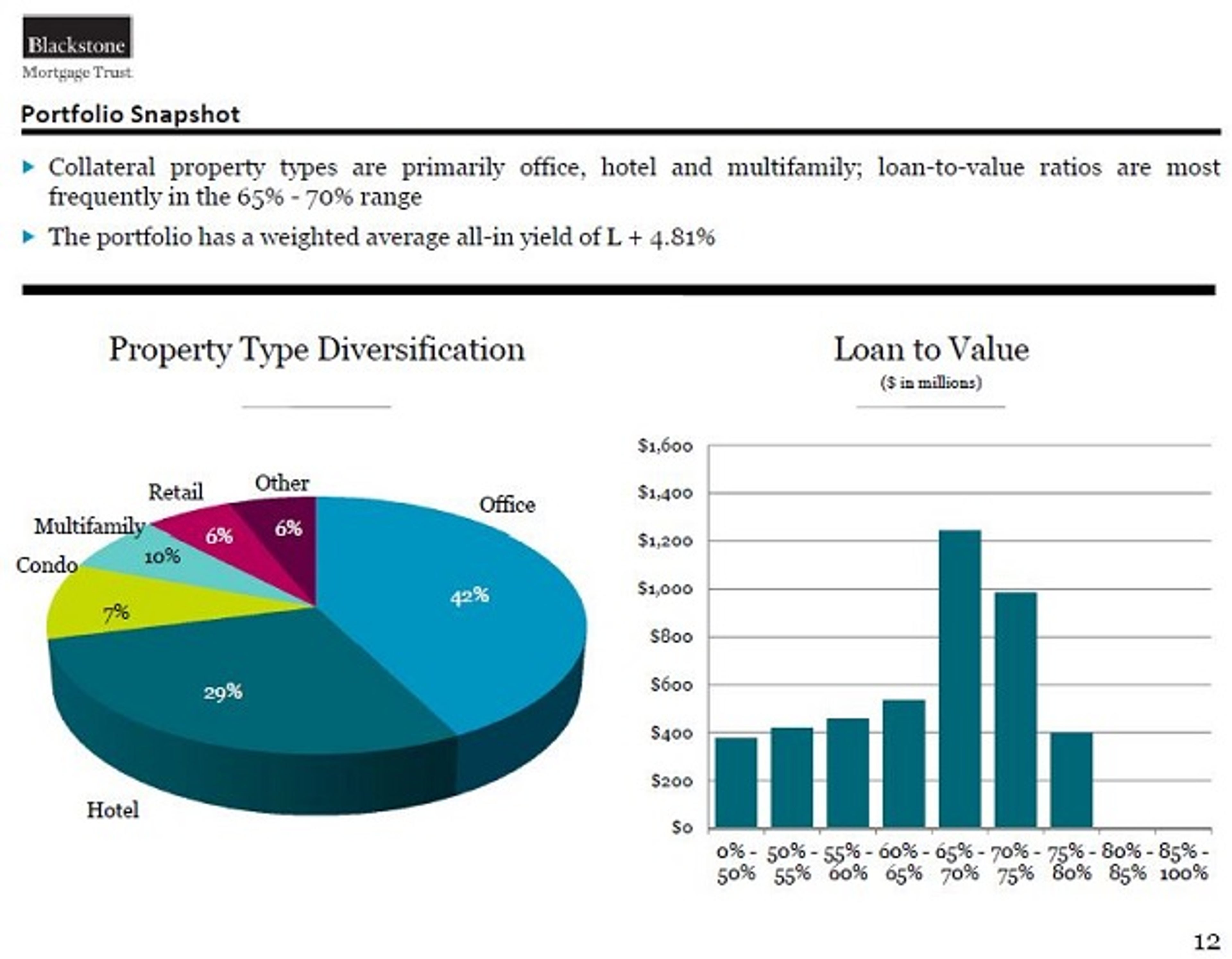

Existing Blackstone Mortgage Portfolio - Feb. 2015

The portfolio to be acquired by BXMT "consists of 82 first mortgage loans secured by a diverse set of commercial property types across its core and target markets, including the United States (68%), Canada (15%), the United Kingdom (10%), and Germany (7%) with an estimated weighted average loan-to-value ratio in line with BXMT's existing portfolio."

Not All Mortgage REITs Are Alike

When most investors think of mortgage REITs (mREITs) the images that often comes to mind are: risky high-yielding mREITs, typically leveraged (5x or more), largely residential mortgage portfolios, containing long-term fixed rate mortgages or mortgaged backed securities.

This strategy can result in a high degree of volatility when interest rates change, resulting in sudden losses of book value and/or dividend cuts, if rates move the opposite of how the portfolio is constructed and hedged.

The Blackstone Mortgage Trust model is basically 180 degrees different from that, and therefore is potentially much more attractive to the average investor.

The BXMT Secret Sauce

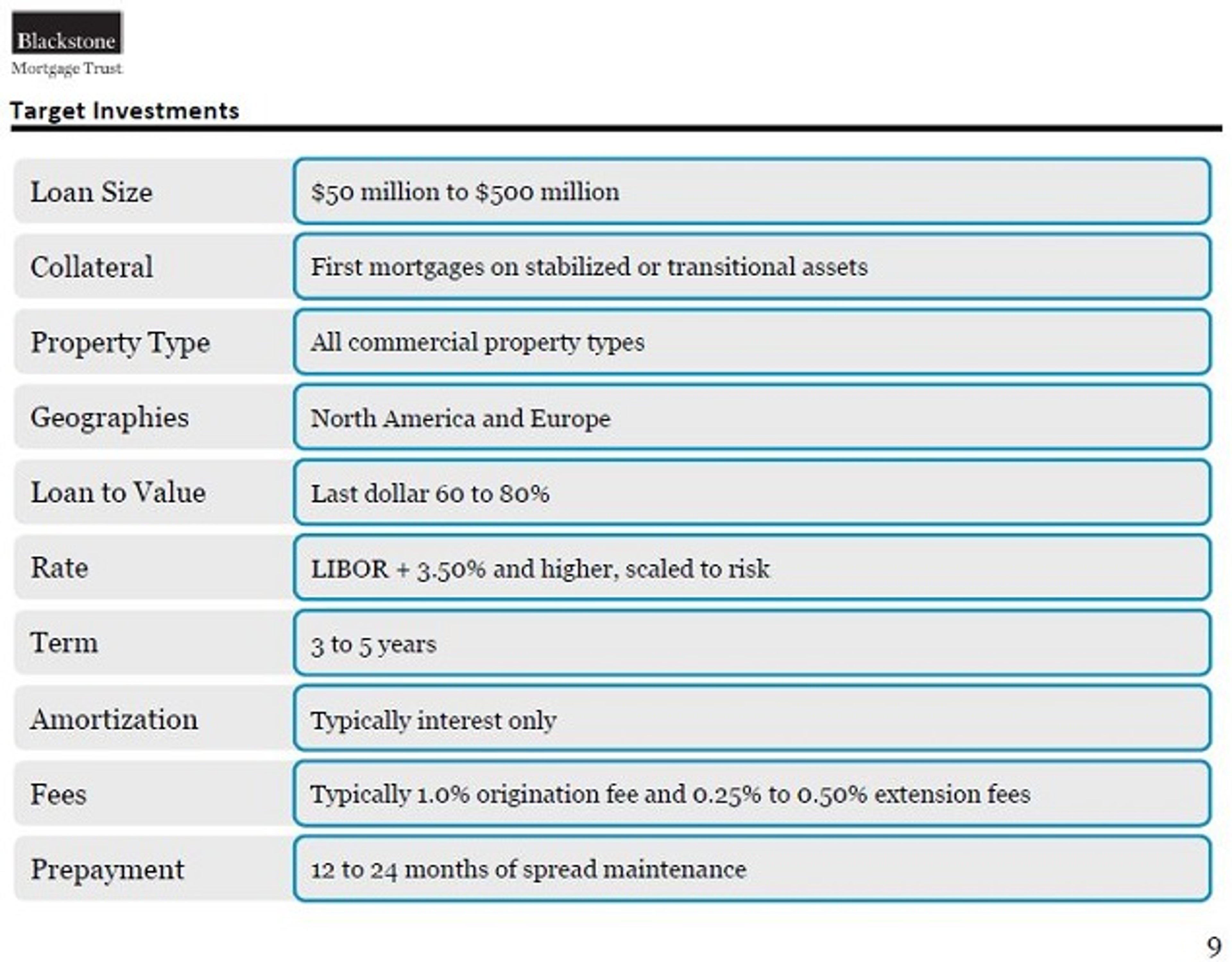

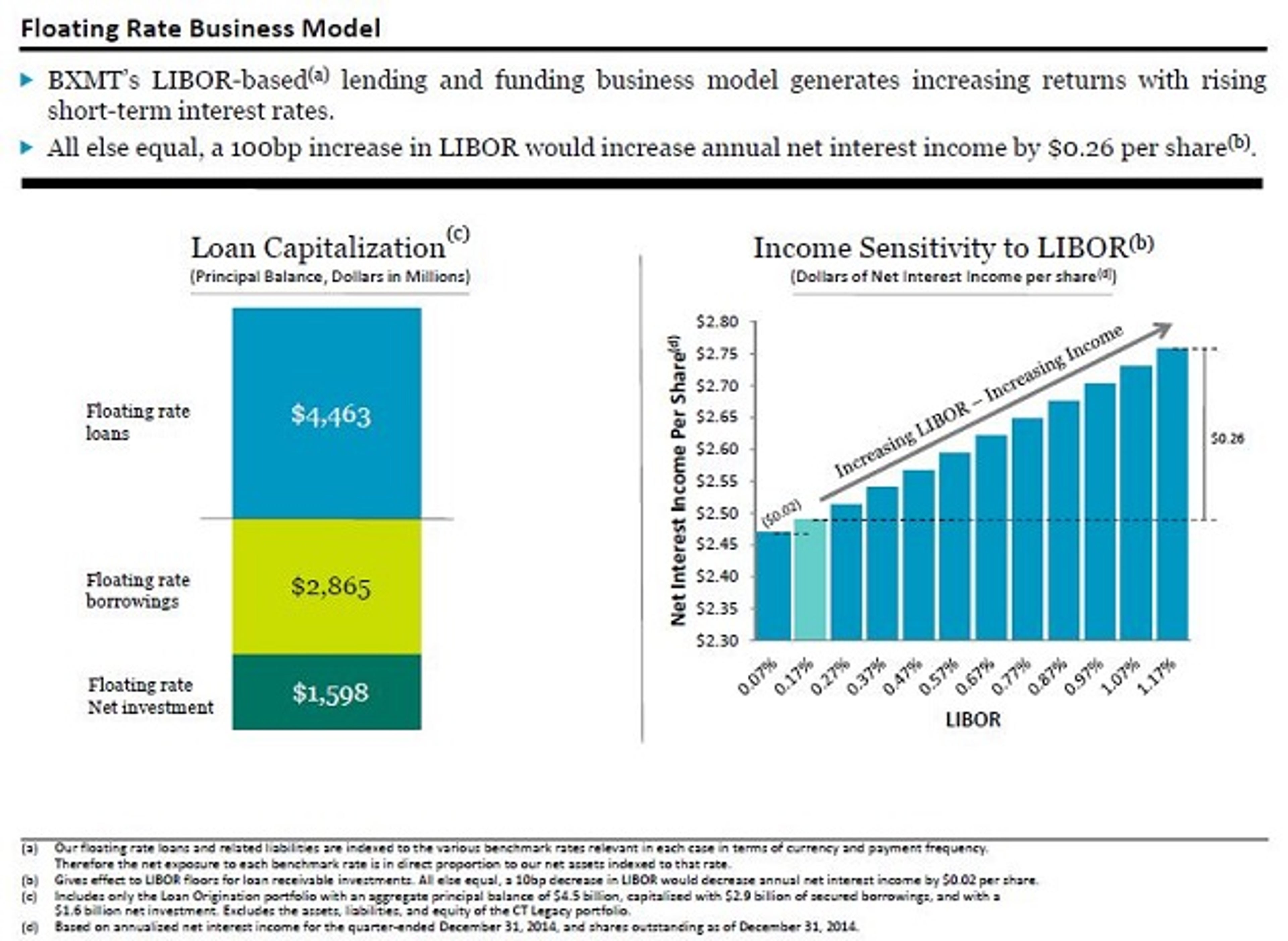

The BXMT "secret sauce" is making shorter duration, floating rate loans on commercial real estate which are typically tied to a spread above LIBOR of 3.5 percent or more. This locks in a minimum return, which potentially could increase in a rising rate environment; not lose value like long-term fixed rate mortgages.

This strategy is currently paying BXMT shareholders a yield of ~7.4 percent.

• http://www.benzinga.com/news/15/03/5335303/blackstone-ceo-steve-schwarzman-on-the-art-of-the-long-view

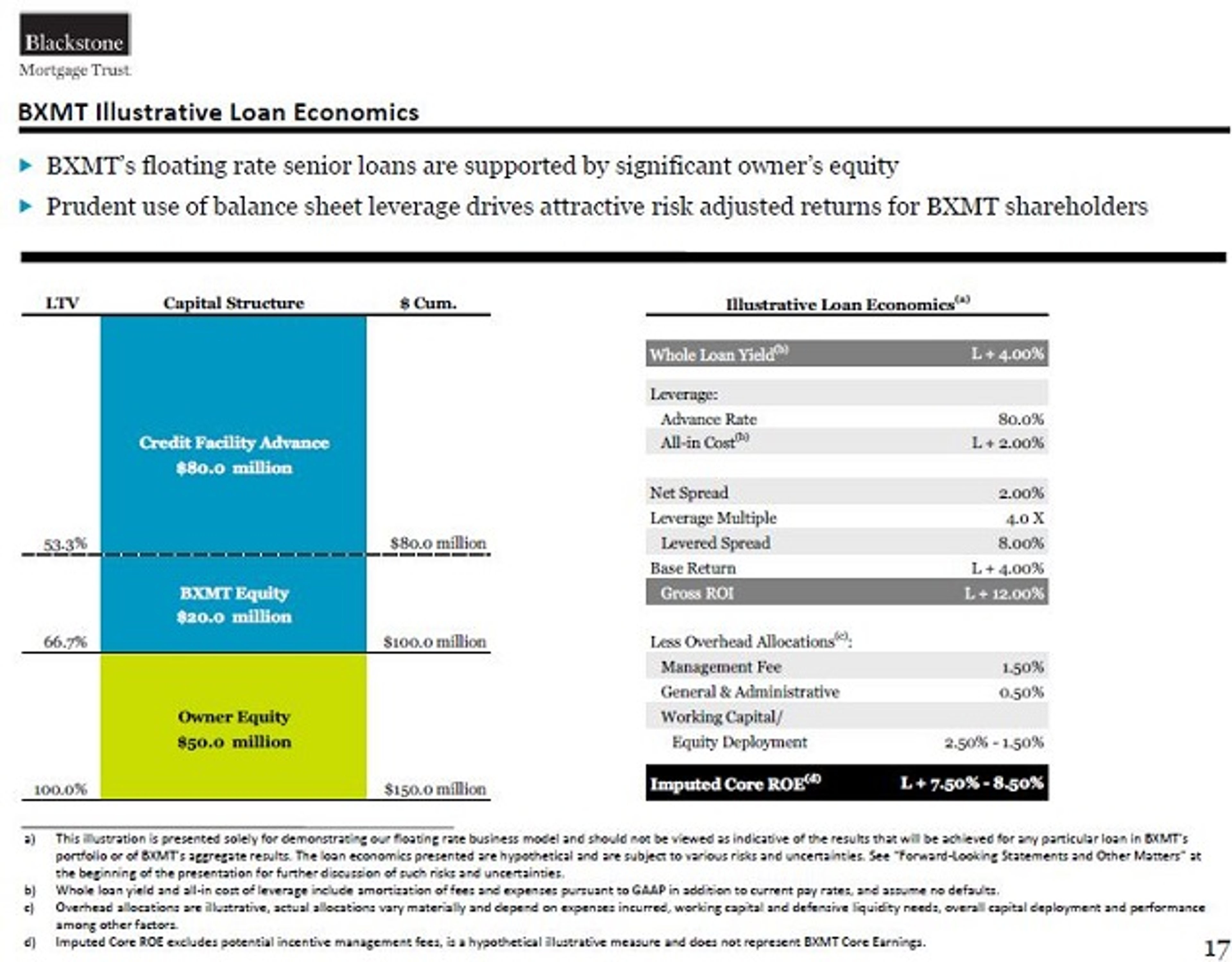

Blackstone Mortgage - Deeper Dive

All slides are from a February 2015 Blackstone Mortgage presentation.

Bottom Line

All things being equal, by doubling its AUM, Blackstone Mortgage should be better positioned to deliver higher margins due to increased scale moving forward.

Loading...

Loading...

BXBlackstone Inc

$135.75-0.86%

Edge Rankings

Momentum

34.80

Growth

61.21

Quality

59.25

Value

Not Available

Price Trend

Short

Medium

Long

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in