If you’d told someone two months ago that by April 1 crude would be barely hanging on to $20 a barrel and economists would be forecasting possible 15% unemployment, you’d probably have thought it was a bad April Fool’s joke in advance.

Unfortunately, it’s no joke, and April Fool’s Day and the new quarter dawns with plenty of misery despite the major indices rising four of the last six days.

Yesterday’s late washout spilled into overnight futures trading as investors contemplated what President Trump has said will be a “very, very painful two weeks.” If the crisis hadn’t sunk in yet for investors, it probably is now after the market posted its worst Q1 ever.

Q2 is starting us off with a lot of the same punches we saw in Q1. People are trying to figure out what it all means, and when they don’t know, the first reaction is often to sell.

The good news is that things didn’t go limit-down overnight the way they did a couple weeks ago. It wasn’t a good night, but the big moves aren’t as violent and the market is coming back a little toward some possible ranges. It hasn’t set a range yet, but it’s down 3.5%, not 5%. That’s the solace. It’s a tough time, but there’s solace that we’re possibly starting to get back toward setting some ranges.

Sorting Through the Numbers

There’s a hefty dose of data on the way today, including car and truck sales, ISM manufacturing, and construction spending. Of these, you probably want to give ISM the closest look. It was trending kind of weak even before the crisis hit.

In other manufacturing data, good news came out of China earlier today as the Caixin manufacturing PMI climbed 9.8 points to 50.1 in March. That was better than many analysts had expected, but remember this isn’t hard data. It’s a sentiment measure that gauges how manufacturers see conditions vs. February. Still, it’s good to see sentiment improve in China and could be another sign of the country recovering from the virus.

Still, Asian and European stocks fell sharply earlier today. Japan’s Nikkei was down almost 5%. Over in Europe, some banks said they won’t pay dividends because they want to keep cash on hand as the economy hits the brakes. There’s tough stuff everywhere today.

There’s definitely some buying interest in bonds this morning, which could be a sign of more investor caution. The 10-year yield lost its grip on the 0.7% handle this morning and plunged all the way back to just above 0.6%. Cboe Volatility Index futures (/VX) are flirting with 60. Gold is up, but pared some of its overnight gains. Crude managed to hold the $20 a barrel line.

One possible reason for the heavy losses early Wednesday could be the quarter ending and “window dressing” being finished. That’s a term for position-squaring many fund managers do at the end of a quarter, and it might have contributed to some of the rebound we saw over the last week. Now the window dressing is being removed, so to speak.

Counting Your Blessings

From a market perspective, at least, things could be far worse. The roughly 24% loss in the S&P 500 Index (SPX) from February’s peaks isn’t nearly as bad as the one experienced during the 2008 financial crisis. Although there’s no guarantee the major indices won’t re-test earlier lows or even get worse, it does look like for now, at least, the markets are trading in less wide of a range. Volatility started to step back yesterday, too.

Another positive element lately is some retail investors were apparently stepping back into the market. Though people aren’t typically going “all in”— seldom a good idea even in the best of times—it does seem like many investors are getting comfortable with some of the levels the major indices are at now.

There’s been a really nice bounce from recent lows, and some consolidation appears to be happening after a couple of really wild weeks. Some people apparently saw the downturn as a buying opportunity, but they didn’t spend everything in one place. It looks like many have cash on the sidelines looking for more opportunity if it comes, which could indicate a “buy the dip” mentality possibly shaping up. We’ll have to wait and see if that happens today as the market looks set to swing sharply lower. It will be interesting to see as we go through the day if people start buying a bit.

The dollar continues to fade from nearly three-year highs reached earlier in March when investors appeared to be rushing to cash. If the dollar continues to fall, that could be another good sign that more people are putting their money in places besides under the mattress. On the other hand, Treasury yields remain historically low and don’t seem to be getting much of a bounce.

Another good thing specifically about entering a new quarter is that companies start to report, which could provide a much cleaner lens into the potential impact of the crisis. We’ve all been fumbling through the dark trying to find the light switch. Companies won’t necessarily be ready to shine an arc lamp on the situation yet, but anything they can share has to be better than this confusion.

No one knows how long this national shutdown might last or how bad unemployment might get, though Goldman Sachs Group Inc. GS sees unemployment hitting 15% by mid-year.

Obviously, the length of this crisis is a huge unknown. One thing investors might want to follow is a site maintained by The Institute for Health Metrics and Evaluation (IHME), which at this point predicts U.S. deaths from the virus to peak around April 14 and slowly decline from there. The IHME says its projections “assume the continuation of strong social distancing measures and other protective measures.”

It’s positive to see some signs of “curve bending” in a few places around the U.S., according to media reports. However, it wasn’t enough to rescue stocks late Tuesday or early today.

Same Difference

The old quarter ended in familiar territory, with steep losses. After a week of mostly stronger trading, major indices saw their early rally flag and then fade pretty badly into the close. End-of-quarter rebalancing might have contributed to the huge 4% plunge in Utilities stocks and a surprising jump in the Energy sector despite crude staying below $21 a barrel, Briefing.com observed.

Selling yesterday was heaviest in the Russell 2000 Index (RUT) of small-caps, continuing the trend of small-caps trailing larger companies. This could indicate investors honing in on large growth companies seen as having the biggest balance sheets and strongest free-cash flow to help them through this crisis. Apple, Inc. AAPL and Alphabet Inc. GOOG GOOGL were among the behemoths that outperformed the broader SPX on Tuesday.

For the SPX, if things get rough enough, the old December 2018 low of 2350 could come into play as potential technical support point. Technical support hasn’t been holding up, however, through most of this crisis.

Yesterday, the Conference Board’s Consumer Confidence Index for March dropped to 120.0 from an upwardly revised 132.6 for February. The March reading was the lowest since July 2017. The silver lining? Analysts had thought it would be even lower.

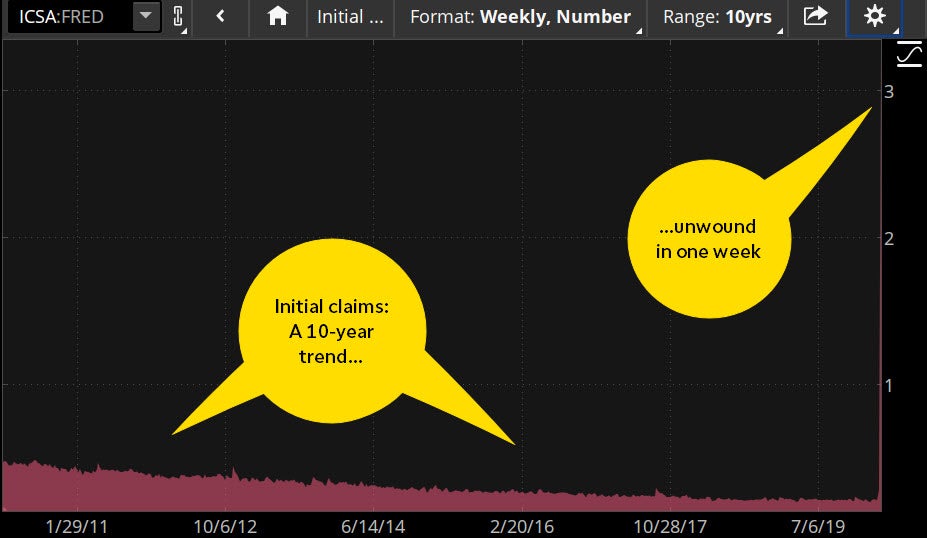

CHART OF THE DAY: WHEN A TREND REVERSES. Last week's jobless claims report showed initial claims of 3.28 million—a new record, and also an immediate unwinding of several years of job growth. Analyst consensus ahead of tomorrow's report is for another 3 million new claims. These two data points are important to keep in mind ahead of Friday's payrolls data release. Data source: Federal Reserve's FRED database. Chart source: The thinkorswim® platform from TD Ameritrade. FRED® is a registered trademark of the Federal Reserve Bank of St. Louis. The Federal Reserve Bank of St. Louis does not sponsor or endorse and is not affiliated with TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

What’s on Tap? Many people are stocking up on painkillers, toilet paper, and hand wipes. Others, though, are taking their own approach to the pandemic. For instance, sales of alcohol have enjoyed a spirited bounce, many Wall Street analysts note. Another sector apparently enjoying a boost is video games, as Activision Blizzard ATVI shares rose again Tuesday, and shares of Nvidia Corporation NVDA—a company whose products serve the video game industry—falling just a touch Tuesday and up 34% from its mid-March low. What else are young people going to do when they’re stranded at home for weeks with their parents? Well, besides video games, there is Netflix Inc. NFLX, which no one needs to be reminded has been one of the best recent performers.

Another winner? Good old-fashioned orange juice. Egg and butter futures might not get traded much these days, but orange juice futures aren’t getting squeezed. They were up 25% from their lows recently as more people try to get their daily dose of Vitamin C, despite some doctors saying there’s little proof it protects against the virus. Then again, try to find a doctor who says beer or scotch helps fight off the microscopic menace, but that hasn’t stopped those items from flying off the shelves.

A Bear of a Different Color: You don’t have to look far to find analysts who say we’re not over the hump yet and another test of the lows could be ahead. Many point to past bear markets where lows got retested over and over. That’s what happened in 2008–2009, for instance. There were a bunch of decent bounces between the first sharp declines in September 2008 and the final 12-year low set in early March 2009. Lots of head fakes, when you look back at the charts from then. Hindsight is 20-20.

One argument against comparing this bear market to past ones is that this one really came out of the blue and involves something unrelated to the financial system itself. You can’t blame this situation on the banks or the “dot-coms,” like the last two. It doesn’t reflect some sort of breakdown in any one sector that’s dragging everything else down. It’s a brutal and sudden body blow to the entire market from the same outside event, more like a Sept. 11 kind of attack (though that came in an economy that was already slowing). Goldman Sachs said yesterday it expects gross domestic product to decline more than 30% in Q2. But it also said it expects things to bounce right back with 19% growth in Q3. Because it’s a singular problem and hopefully has a solution, this time might not be like last time as far as the bear market is concerned.

What Do You See, Dr. Watson? Anyone seeking clues on investor sentiment at this time of crisis might consider monitoring companies investors embraced when the virus first sank its talons into the economy about a month ago. Two of these are The Kroger Co. KR and The Clorox Comapny CLX, shares of which raced ahead in early March as many Americans made emergency purchases based on supply shortage fears. After their initial rallies, both KR and CLX declined pretty sharply from about March 17 through March 25 as the SPX began a rebound and public acceptance of a long downturn appeared to grow. However, the two stocks both gained ground over the last week, so maybe people are getting anxious again. What’s interesting is how the slight bounce in these two Consumer Staples stocks was accompanied by recent strength in the ultra-cyclical sector Information Technology. Buying in that sector is often seen as a sign of investor confidence in the economy. Stay tuned for the next dramatic chapter in this mystery.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.