(Wednesday market open) As Congress gathers to vote on a debt ceiling bill, the market’s focus turned overseas this morning to cooler-than-expected data from China and Europe. Stocks came under pressure but the dollar rose and crude oil plunged.

Inflation data from France and parts of Germany was lower than anticipated and a manufacturing reading from China showed activity contracting there for the second month in a row. Weaker inflation in Europe could take pressure off the European Central Bank to keep raising rates, perhaps a reason why the euro fell versus the dollar today.

With Friday morning’s May Nonfarm Payrolls report and a debt ceiling vote looming, trading on Wall Street could be subdued the next couple of days, as it was to some extent Tuesday. Major indexes were broadly lower in premarket trading.

As people returned from the holiday yesterday, a familiar pattern resumed. A few mega-cap info tech stocks shined Tuesday while most of the market languished. Declining shares led advancing ones even as the tech-packed Nasdaq 100 (NDX) climbed and the S&P 500® Index (SPX) held its ground. The rally hasn’t been a healthy, broad-based one that lifts all boats.

However, the tech stocks that drove last week’s rally show signs of running out of steam. Nvidia NVDA reached nearly $420 a share at one point yesterday, but now it’s below $400.

Morning rush

- The 10-year Treasury note yield (TNX) slipped another four basis points to 3.65%

- The U.S. Dollar Index ($DXY) reached a new two-month high of 104.46 as the euro declined.

- The Cboe Volatility Index® (VIX) futures rose to 17.97.

- WTI Crude Oil (/CL) plunged to $67.54 per barrel, a nearly four-week low.

Treasury yields swung lower early this week as some risk premium exited stage left following the debt ceiling deal. With less chance of default, investors embraced Treasuries again—and when Treasuries rise, yields ease. A weak reading on the Dallas Fed manufacturing index Tuesday might also have weighed on yields.

WTI Crude Oil (/CL) slipped to three-week lows Tuesday amid debt ceiling worries and sparring among OPEC members ahead of the cartel’s meeting this weekend. Energy shares slumped as crude contracted.

Stocks in the Spotlight

Earnings roundup: It’s been a rough morning for shares of Hewlett-Packard Enterprise HPE, which fell 8% in premarket trading after the info tech company reported lower-than-expected revenue and reduced its guidance for the year. HP HPQ shares also faltered this morning as investors digested its earnings.

Salesforce CRM is expected to report after the close today. When the cloud software maker reported fiscal Q4 earnings back in March, shares soared 16%. The company’s strong forecast and announcement of a major stock buyback helped then, but that means investors approach today’s earnings with high expectations. Salesforce projected fiscal Q1 revenue of between $8.16 billion and $8.18 billion, with profits of $1.60 to $1.61 per share.

Last time out, a company executive told Barron’s that tough macroeconomic conditions continued to have an impact on Salesforce’s customers, but no worse than in the previous quarter. Today’s report could provide investors an updated view of cloud market demand.

This short week is long on earnings. Quarterly reporting moves along tomorrow with expected results from Broadcom AVGO, Dollar General DG and lululemon LULU.

Eye on the Fed

Chances of a 25-basis-point rate hike at the June meeting stand at 66% as of this morning, according to the CME FedWatch tool. That’s up from 36% a week ago.

The two elephants in the room are this Friday’s jobs report and next week’s May Consumer Price Index (CPI). Either or both could influence the outcome of the June 13–14 Federal Open Market Committee (FOMC) meeting.

Analysts expect jobs growth of 190,000 in May, according to Trading Economics. The wage component might have even more impact on the Fed after strong 0.5% hourly pay growth in April. Analysts expect a slight easing to 0.3% in May.

Meanwhile, the premium of the 2-year Treasury note yield to the 10-year Treasury note yield (the yield curve inversion), has steepened to around 80 basis points after falling to 60 basis points earlier this month. A steepening curve is often associated with higher chances of an economic slowdown, and the 2-year note yield is more sensitive to rate hikes.

A couple of Fed speakers are on the docket today as the futures market continues to price in a higher probability of another 25-basis-point rate increase in June. Fed Governor Michelle Bowman speaks this morning and Fed Governor Philip Jefferson is on tap this afternoon.

What to Watch

Investors should watch for a couple of important reports soon after the open today. Then tonight long after the close, at 1 a.m. ET, comes China’s May Manufacturing Purchasing Managers Index (PMI).

On the job: The April Job Openings and Labor Turnover Survey (JOLTS) report, due just after the market opens, is expected to show a slight decline from March at 9.37 million openings, according to Trading Economics. The March figure remained historically high at 9.59 million, but below last year’s even more swollen numbers. The number bows at 10 a.m. ET.

Midwest markets: Chicago PMI, which tracks the health of the manufacturing sector around the Chicago area, is the other key report following the bell today. The headline figure was 48.6 in April, which represents contractionary territory. Analysts believe things got worse in May, with consensus at 46.1, according to Briefing.com. Chicago PMI hasn’t been in expansion mode above 50 since last August, and this report doesn’t look likely to break the negative swing.

Soggy May: The May ISM Manufacturing Index due out Thursday morning has been in contraction territory below 50 going back to last October. Analysts expect that to remain the case, projecting a headline of 47, down from 47.1 in April, Trading Economics says. Higher borrowing costs and tight credit are among the factors inhibiting manufacturing activity.

Beijing watch: Things aren’t a lot better in China, apparently. The May Caixin China General Manufacturing PMI fell to 49.5 in April from 50 in March, and analysts look for another 49.5 reading in May. We’ll have that report in our hands by the time Wall Street wakes up Thursday morning. More weakness in China might start having an impact on some of the U.S. sectors with exposure to that economy, including info tech, automobiles, and commodities-related companies (think energy).

U.S. agency bonds are a type of highly rated bond investment that may help investors earn slightly higher yields than U.S. Treasuries without taking on too much additional risk. Learn more about this somewhat under-the-radar investment in Schwab’s latest bonds update.

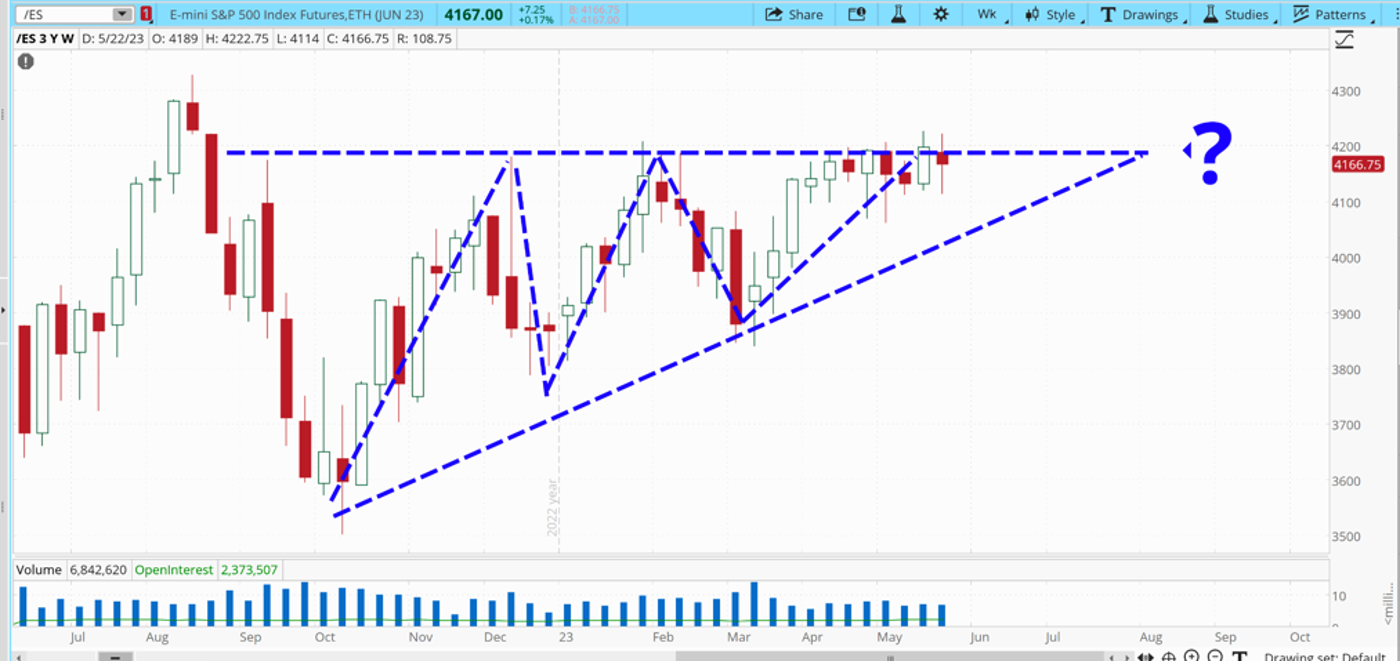

CHART OF THE DAY: BULL PEN. There’s a bullish “ascending triangle” pattern setting itself up in S&P 500 futures on the 1-year weekly chart (/ES—candlesticks). This doesn’t guarantee gains from this point, of course. Resistance still seems quite heavy at around 4,200, and any negative debt ceiling news from Washington might shift things quickly. Data source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Thinking cap

Ideas to mull as you trade or invest

How’s my credit? The credit crunch many economists feared back in March following banking industry turmoil hasn’t arrived. Bank loans and deposits both edged higher last week, and credit spreads—or the ratio between corporate and Treasury yields—continued trading in a relatively narrow range. A large jump in that spread might indicate bank reluctance to issue new credit or company reluctance to take on new debt in an environment where borrowing has become costly, so stay on the lookout. Average investment grade (IG) spreads began the week at +141, which was four basis points tighter than a week before. Average high yield spreads started the week at +453, or nine basis points tighter on the week.

Missing demand: High interest rates, of course, aren’t the only factor that could keep companies out of the credit market. The energy sector, which traditionally borrows heavily, could be less likely to take on loans as crude oil prices remain under pressure. U.S. gasoline demand on Memorial Day fell 3.6% from a year earlier and WTI Crude futures (/CL) dropped below $70 per barrel. This soft demand and pricing picture, if it continues, wouldn’t typically have upstream oil companies eager to reach for the drills. OPEC is scheduled to meet this weekend, and some analysts believe another output cut could be coming. If that, along with relatively light U.S supplies, brings the crude market back, maybe the oil patch could get itchier to uncover new supplies.

When you’re wrong…: Wall Street analysts have missed the boat on nearly every monthly U.S. Nonfarm Payrolls report for a year or more. The pattern is almost always the same: Analysts anticipate slowing jobs growth, and the actual number easily outpaces Wall Street’s average estimate. The worst call was in January, when the average estimate was 185,000 and the actual number was 504,000. The pattern held in February, though in March analysts guessed nearly right. In April the pattern resumed, with actual growth of 253,000 easily topping the average estimate of 180,000. Throughout the postpandemic recovery, analysts have simply underestimated the job market’s strength. For Friday’s May report, the average analyst estimate is 190,000, according to Trading Economics. The average underestimate for the first four months this year is 127,000, which would suggest May jobs growth of well over 300,000 if the pattern holds. Who knows, though. Maybe they have it right this time.

Calendar

June 1: May ISM Manufacturing Index, April Construction Spending, expected earnings from Dollar General (DG), Broadcom (AVGO), Lululemon (LULU), and Hormel Foods (HRL).

June 2: May Nonfarm Payrolls

June 5: April Factory Orders and May ISM Non-Manufacturing Index.

June 6: No major earnings or data.

June 7: April Trade Balance and April Consumer Credit and expected earnings from Campbell Soup (CPB).

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.