It’s never too early to start saving for retirement.

If you’ve already started, and set aside even a little bit, congratulations. You’re ahead of a sizable portion of Americans, according to a 2017 Retirement Confidence Survey conducted by the Employee Benefit Research Institute (EBRI). Only 61 percent of survey respondents say they've saved anything toward retirement, and 24 percent say they have less than $1,000 in savings and investments.

For those of you that haven’t yet, but are ready to get started, a good first step toward retirement planning can be understanding the alternatives—the types of accounts available and the different types of financial professionals who can help you on your journey.

Retirement Savings Products

While there are a number of ways to save and invest for retirement, some retirement accounts come with possible tax advantages. Two common retirement plan types are the 401(k) plan, typically offered through an employer, and the Individual Retirement Arrangement (IRA), which can be set up through a bank, broker, or other financial institution. Here’s a look at some of the most popular options.

- 401(k) and other employer-sponsored retirement plans: If your employer offers a 401(k) plan, you can have money automatically deducted from each paycheck, which you can then invest into the plan’s investment choices. Consider making as big a contribution as possible—taking contribution limits (which are $18,500 for 2018; $24,500 if you’re age 50 or older) and your financial situation into account—to help maximize your savings. Some employers may also match a percentage of employees’ contributions, which helps to add to your nest egg. Obviously the more you can contribute the better, but if money is tight, work to at least contribute to get your company’s match. You don’t want to leave free money on the table.

- Traditional IRA: There are several types of IRAs, each with different potential advantages, rules, and limitations. With a Traditional IRA, investors can make tax-deductible contributions up to $5,500 for the 2018 tax year ($6,500 if you’re age 50 or older). Like a 401(k) plan, you don’t pay Federal taxes on the contributions and investment earnings until you take out money. IRAs can allow some flexibility in investment choices, unlike a 401(k) plan, which may limit you to a specific group of funds. Consider an IRA if you don’t have access to a 401(k) with matching funds. Or, if you’ve contributed to your 401(k) up to your company’s matched limit, consider contributing to an IRA. Yes; you can potentially contribute to both within the same tax year.

- Roth IRA: Although there are no tax deductions up front for Roth IRA contributions, your withdrawals and earnings may be tax free at the Federal level if certain conditions are met. You may want to compare Roth and Traditional IRAs to see which may be right for you.

- SEP and SIMPLE IRAs: If you happen to be among the 28 million small business owners, or one of the 15 million self-employed workers in the U.S., there are a couple plans designed just for you. SEP IRA plans and SIMPLE IRA plans offer many of the same potential tax advantages as Traditional IRAs, but the contribution limits are typically higher. Each has its own set of rules and requirements, potential benefits, and drawbacks.

You may also want to visit the IRA Selection Tool which can help you determine your IRA eligibility and how much you may be able to contribute to either a Roth or Traditional IRA.

Getting Started

Once you’ve educated yourself on available retirement savings accounts, and chosen which might work for you, you may consider calculating how much money you may need once you get to retirement. Using a Retirement Calculator can help.

Other things to keep in mind when setting your retirement goals include: (1) When do you expect to retire?; (2) How much do you need before you can retire?; (3) How much will you contribute each month to help reach your goal?; (4) Which types of investments and asset allocation could align with your risk tolerance and retirement savings goal?

Let Compounding Work for You

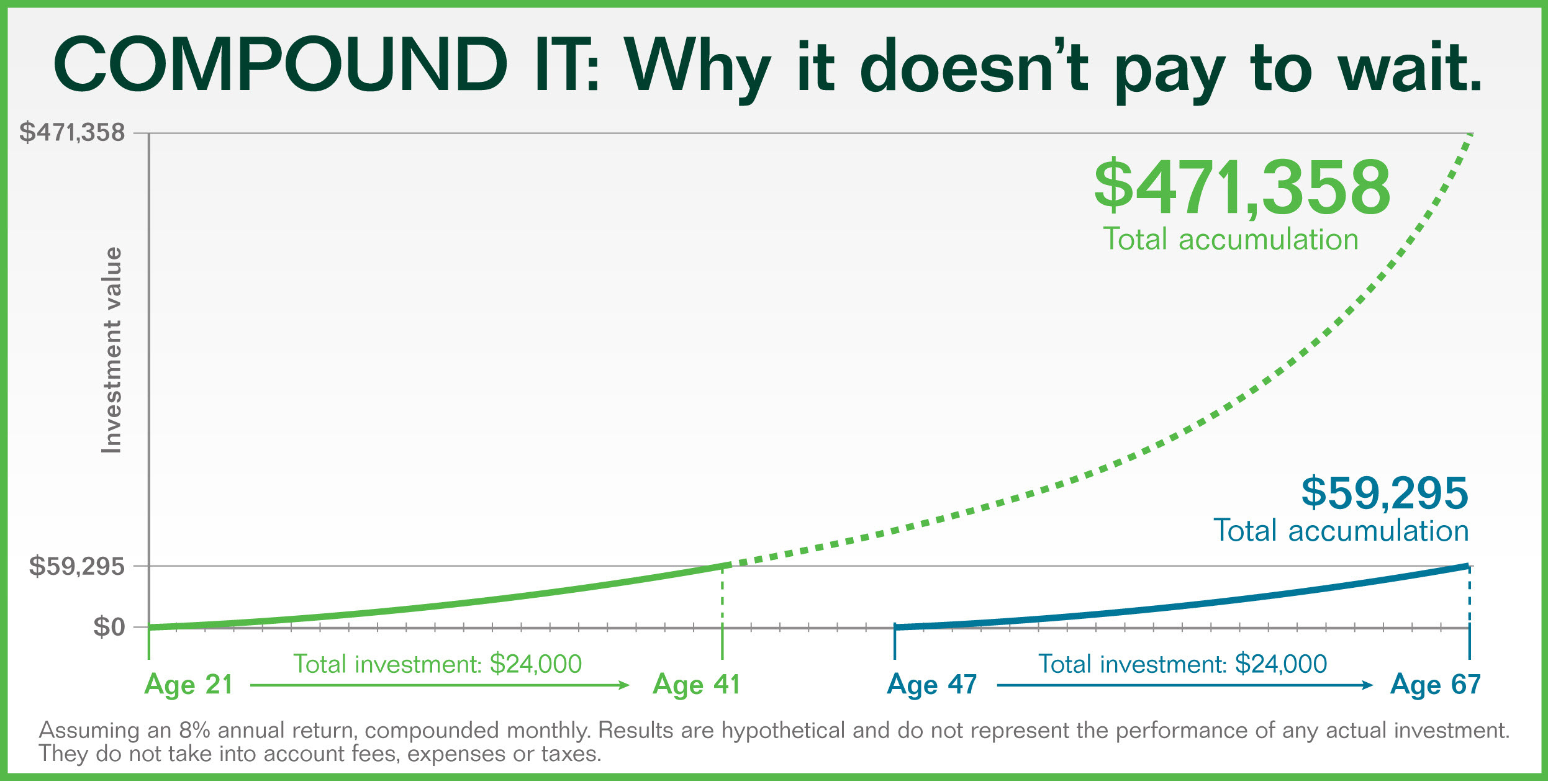

A long-term investor can attempt to use the power of compound interest —which is interest earned on top of interest — to potentially enhance returns. Let’s look at a hypothetical example: If you invest $10,000 at 8 percent a year, you’d have earned $800 after one year, for a total of $10,800. The next year, however, your 10 percent interest would come on top of the $10,800 you now have, not just the original $10,000, meaning your interest earned would be $1,080, rather than $1,000. That might not sound like much, but it can build up quickly.

Because compound interest builds on itself over time, investors who start early tend to have a significant advantage over those who wait, as shown in the graph below.

Working with a financial professional who can provide access to products, tools, research, and guidance may help you get more confident about pursuing your retirement goals. A TD Ameritrade Financial Consultant can help you develop a plan that defines a strategy, timeline, and potential solutions that may help you pursue your investment objectives.

If you have more complex advisory needs you may want to consult with a financial advisor or another type of financial professional. Not all are the same, and it helps to know the difference. Here are three common designations:

- Certified Financial Planner (CFP). Certification requires passing a comprehensive board exam covering financial planning, insurance, taxes, retirement, and estate planning.

- Chartered Financial Consultant (ChFC). Requires a bit more coursework than the CFP, but certification doesn’t require a board exam.

- Registered Investment Advisor (RIA). The RIA designation is more about registration than certification. An RIA is registered with the Securities and Exchange Commission and/or a state securities regulator.

Your financial advisor may have one or more of these licenses and certifications. Each of them comes with a certain level of education and required ongoing learning.

Planning for tomorrow involves setting financial goals today. I hope you found this article helpful and I encourage you to explore the resources you can find throughout the Retirement Planning page.

Check out this Retirement Checklist which can help you streamline your strategy or consider scheduling a complimentary goal-planning session.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.