OMAHA, Neb. — After a volatile week, stocks closed lower with the S&P 500 shedding 0.8%. The index is now up 7.7% year to date, up 15.6% from its October 12 closing low of 3,577.03, and down 13.8% from its January 3, 2022 record closing high of 4,796.56.

As we’ve been discussing on TKer, one of the biggest concerns in the stock market has been the expectation by many that earnings growth could go negative in 2023.

On this near-term matter, Berkshire Hathaway CEO Warren Buffett doesn’t have good news for you.

"In the general economy, the feedback we get is that perhaps the majority of our businesses will actually report lower earnings this year than last year," Buffett said at Berkshire’s annual shareholders meeting on Saturday.

He reflected on the widespread supply chain disruptions everyone has faced since the onset of the coronavirus pandemic.

“It was an extraordinary period,” he said. “And that period has ended.“

For more on how supply chains have normalized, read: We can stop calling it a supply chain crisis

During that period, however, many companies, including those under Berkshire’s umbrella, over-ordered and now sit on excess inventory that will have to be cleared out at unattractive prices.

“It is a different climate than it was six months ago, and a number of our managers were surprised,” Buffett added. “Some of them had too much inventory on order, and all of a sudden it got delivered, and people weren’t in the same frame of mind as earlier.”

While the prospect for lower prices might be welcome news for customers struggling with inflation, it’s bad news for corporate profitability.

“We'll start having sales at places where we didn't need to have sales before,“ he said

Warren Buffett speaks at Berkshire Hathaway’s 2023 annual shareholder meeting. (Source: CNBC / YouTube)

With a market value of $719 billion, Berkshire is one of the largest companies in the world. The diversified conglomerate’s massive portfolio of companies includes dozens of businesses across almost every imaginable industry, employing over 382,000 as of the end of 2022. Its well-known brands include GEICO, BNSF Railway, Fruit of the Loom, Precision Castparts, Benjamin Moore, Duracell, and Dairy Queen.

As such, Berkshire is considered a bellwether of the economy. So it’s worth heeding Buffett’s warning when thinking about the near-term outlook for the business environment.

‘Nothing is ever sure’

That said, don’t mistake Buffett’s warning on earnings as a sign to sell. In fact, Buffett would be the first person to advise against trading on short-term expectations

“Nothing’s sure tomorrow,” he said. “Nothing’s sure next year. Nothing is ever sure in markets or in business forecasts or anything else.”

In response to a question about opportunities in value investing, Buffett criticized those chasing short-term gains.

“The world is overwhelmingly short-term focused,” he said. “If you go to an investor relations call, they're all trying to figure out how to fill out a sheet to show the earnings for the year.”

Obviously, Buffett and his colleagues do buy stocks with the expectation that prices will go up. However, if you ask him about time frames, he’ll tell you its in the order of 20 years.

For more on Buffett’s thoughts on short-term earnings, read: Warren Buffett blasts ‘one of the shames of capitalism’

What Investors Should Make Of All This

Not that anyone should pay attention to quarterly tweaks in Berkshire Hathaway’s portfolio, but as of the end of Q1 the company held $328 billion in stocks, up from $309 billion three months earlier. So Buffett isn’t exactly dumping stocks.

Even assuming the S&P 500 were to report negative earnings growth in 2023, history says this does not guarantee prices will fall for the year. Quite the opposite: stock prices usually rise in years when earnings fall. (Also, worries about weak earnings growth is an old story and has arguably already been priced into the market.)

Investing isn’t about only looking at the positives while ignoring the negatives. It’s about thinking holistically and making informed decisions while balancing the good with the bad.

This is why Buffett’s frank language about the short-term challenges his businesses face is refreshing amid his ongoing long-term optimism with regards to stocks and the U.S. economy.

Reviewing The Macro Crosscurrents

There were a few notable data points and macroeconomic developments from last week to consider:

Fed signals the end of rate hikes. On Wednesday, the Federal Reserve tightened monetary policy further by announcing a 25-basis-point rate hike, bringing the central bank’s target range for its policy rate to 5.0% to 5.25%. This was the 10th straight rate hike announcement, and it brought the range to its highest level since September 2007.

With the announcement, the Fed changed the language of its monetary policy statement in a way that suggested this could be the last rate hike for now.

Specifically, it dropped this phrase from its prior statement (emphasis added):

“The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time.”

And replaced it with (emphasis added):

“In determining the extent to which additional policy firming may be appropriate to return inflation to 2% over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.“

But make no mistake: This is not the beginning of easy monetary policy. From Fed Chair Jerome Powell’s press conference on Wednesday:

“Inflation has moderated somewhat since the middle of last year. Nonetheless, inflation pressures continue to run high. And the process of getting inflation back down to 2%, has a long way to go.”

So, inflation has eased in a way that the Fed seems comfortable not having to tighten monetary policy further, but inflation remains high enough that monetary policy will remain tight for at least a little while.

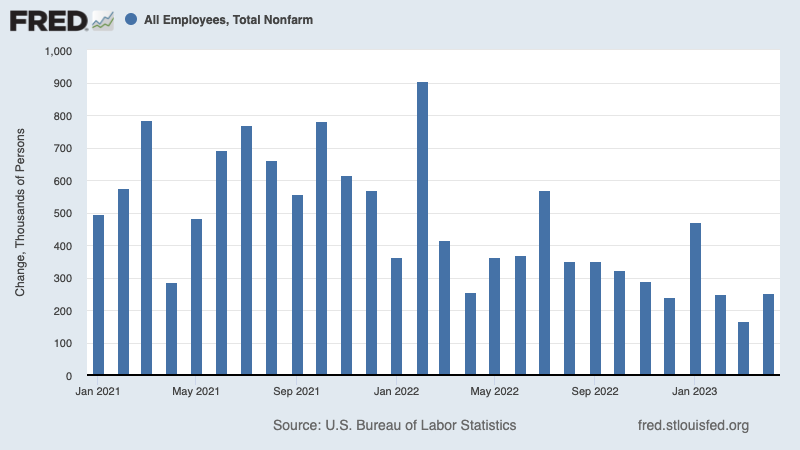

The labor market is hot. According to the Bureau of Labor Statistics, U.S. employers added an impressive 253,000 jobs in April. While the prior two months figures were revised down by 149,000 jobs, they remained positive.

FRED

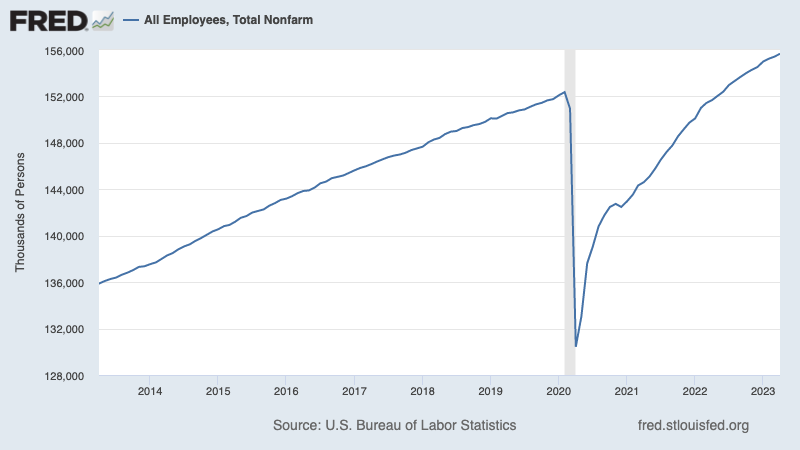

Employers have added 1.14 million jobs since the beginning of the year. Total payroll employment is at a record 155.67 million jobs.

FRED

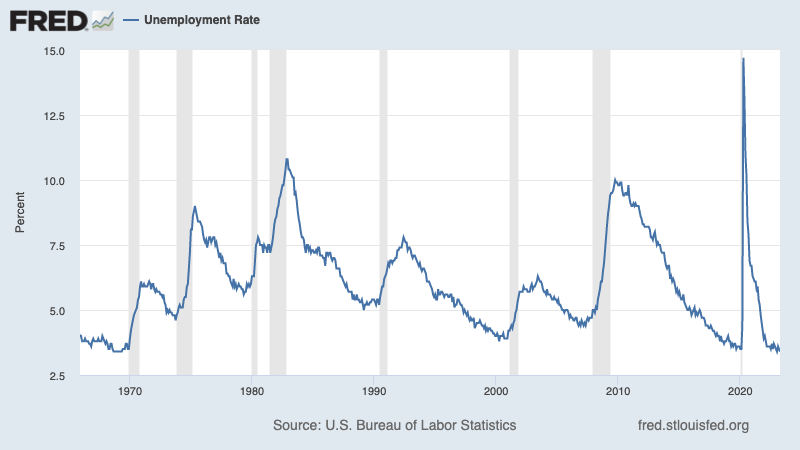

During the period, the unemployment rate fell to 3.4%, the lowest level since 1969.

FRED

Average hourly earnings rose by 0.5% month-over-month in April, up from 0.3% in March. This metric is up 4.4% from a year ago, up slightly from the 4.3% rate in the prior month.

FRED

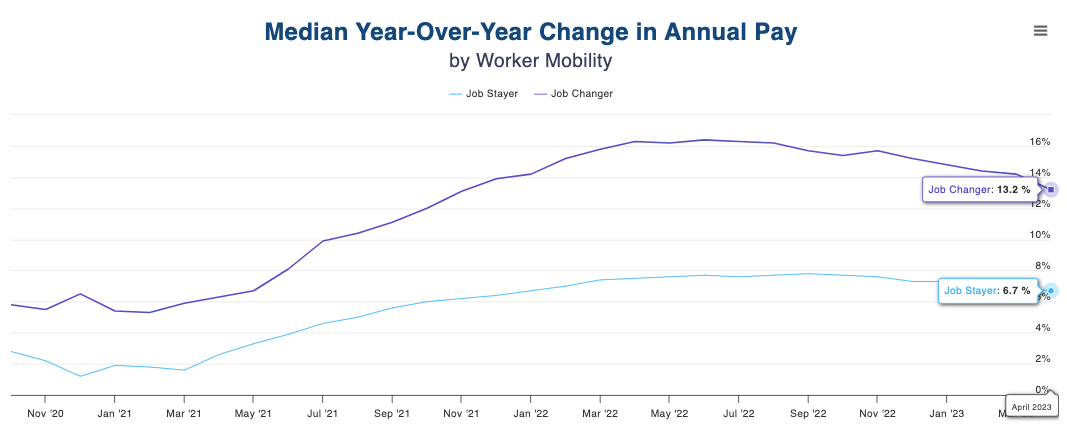

Job switchers get better pay. According to ADP, which tracks private payrolls and employs a different methodology than the BLS, annual pay growth in April for people who changed jobs was up 13.2% from a year ago. For those who stayed at their job, pay growth was 6.7%.

ADP

For more on why the Fed is concerned about high wage growth, read: The complicated mess of the markets and economy, explained

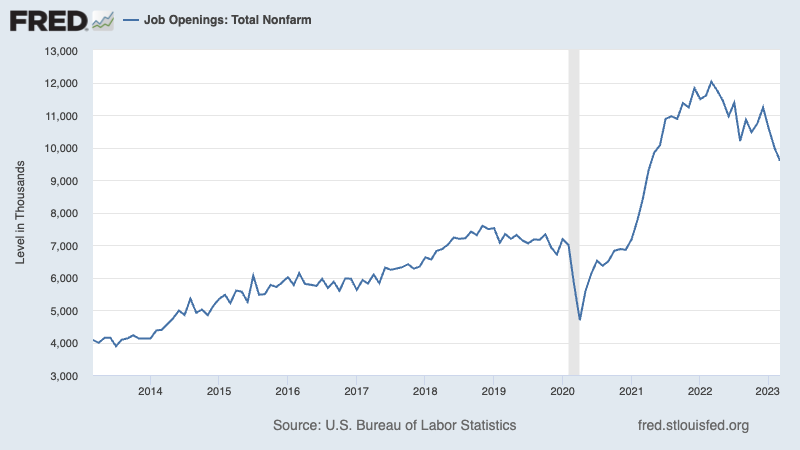

Jobs openings cool, layoffs pick up. The March Job Openings & Labor Turnover Survey confirmed that the labor market, while still hot, continues to cool. Job openings declined to 9.59 million in March, down from 9.97 million in February. This represented the lowest level of job openings since April 2021.

FRED

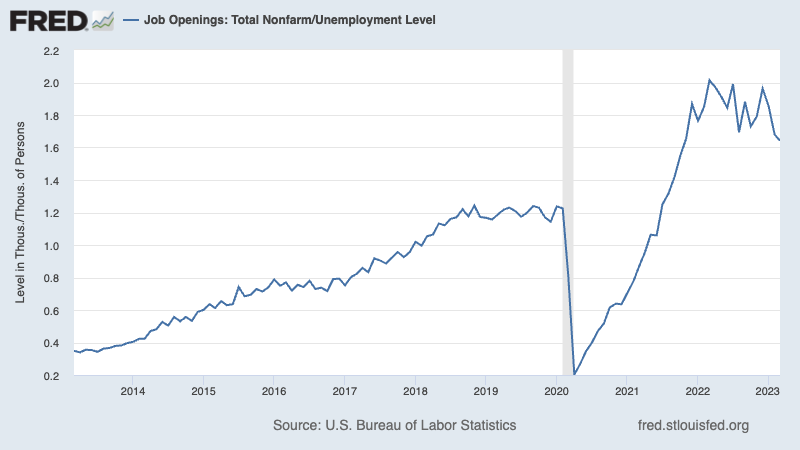

During the period, there were 5.84 million unemployed people — meaning there were 1.64 job openings per unemployed person. This continues to be one of the most obvious signs of excess demand for labor.

FRED

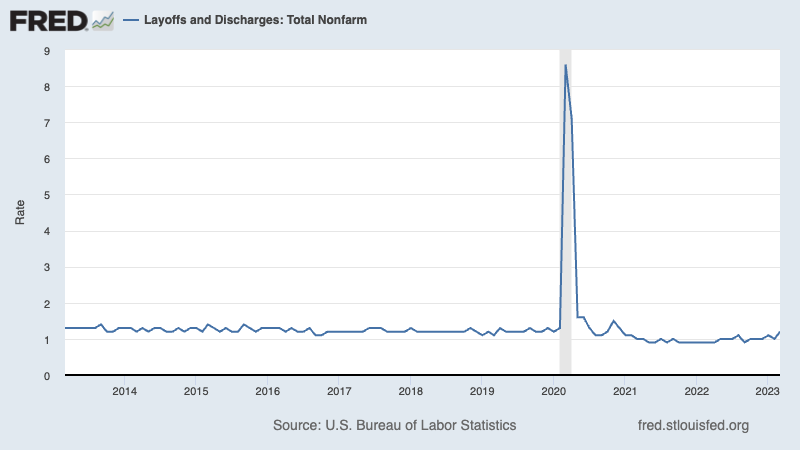

Employers laid off 1.8 million people in March. While challenging for all those affected, this figure represents just 1.2% of total employment. While this latter metric has ticked up in recent months, it’s mostly just normalizing back to pre-pandemic levels.

FRED

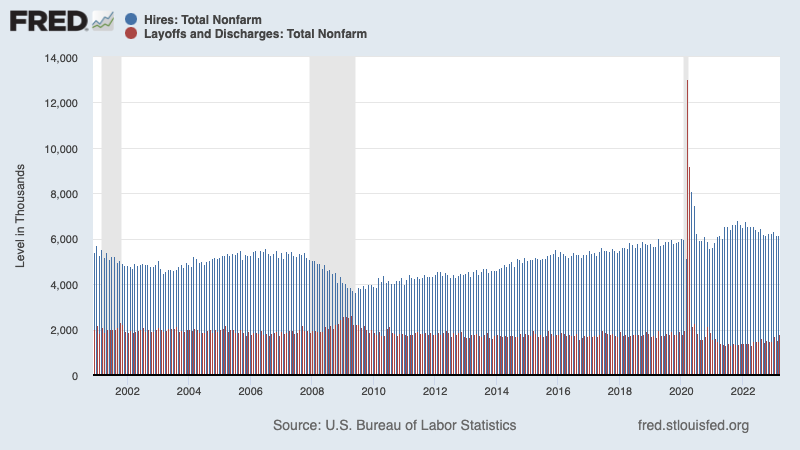

Hiring activity continues to be much higher than layoff activity. During the month, employers hired 6.15 million people.

FRED

Here’s JPMorgan on the JOLTS data: “The job openings and quits rates remain historically high, and the layoff rate remains historically low, but all three are moving in the direction of a cooler labor market.“

For more on the labor market, read: The labor market is simultaneously hot, cooling, and kinda problematic

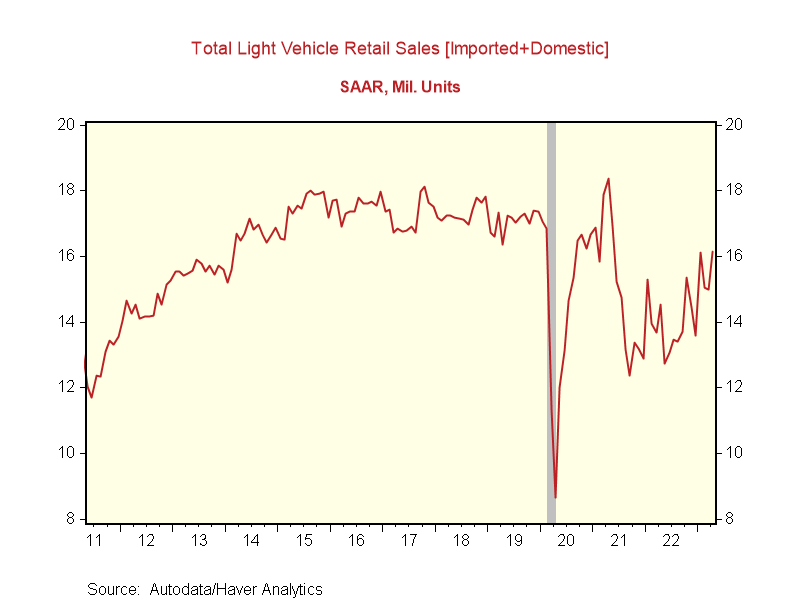

Car sales jump. Via Renaissance Macro economist Neil Dutta: “In April, total light vehicle retail sales advanced to 16.15 million units SAAR, according to Autodata, the highest since the early stages of the pandemic. As supply chains improve, more vehicles show up on dealer lots, we see some incentive activity return and unsurprisingly, sales respond. Of course, buyers right now have been waiting for months; they are motivated despite tough financing conditions.“

(Source: Renaissance Macro)

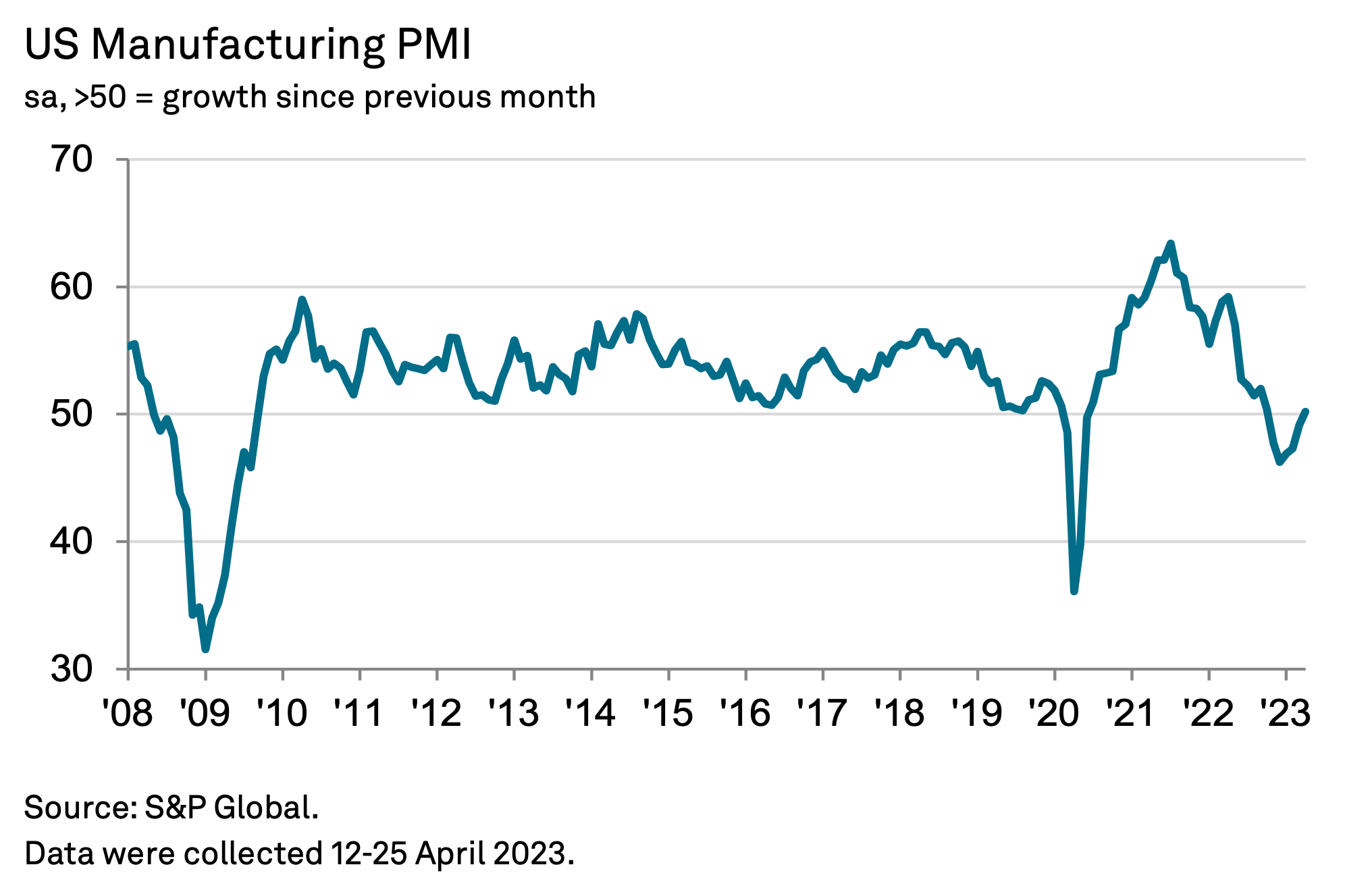

Manufacturing surveys improve. From S&P Global’s April U.S. Manufacturing PMI (via Notes): “US manufacturing output has regained some encouraging momentum at the start of the second quarter, having stabilised in March after four months of decline. While the upturn is in part linked to greatly improved supply chains, helping reduce backlogs of orders, April also saw a welcome upturn in new order inflows for the first time since last September.“

(Source: S&P Global via Notes)

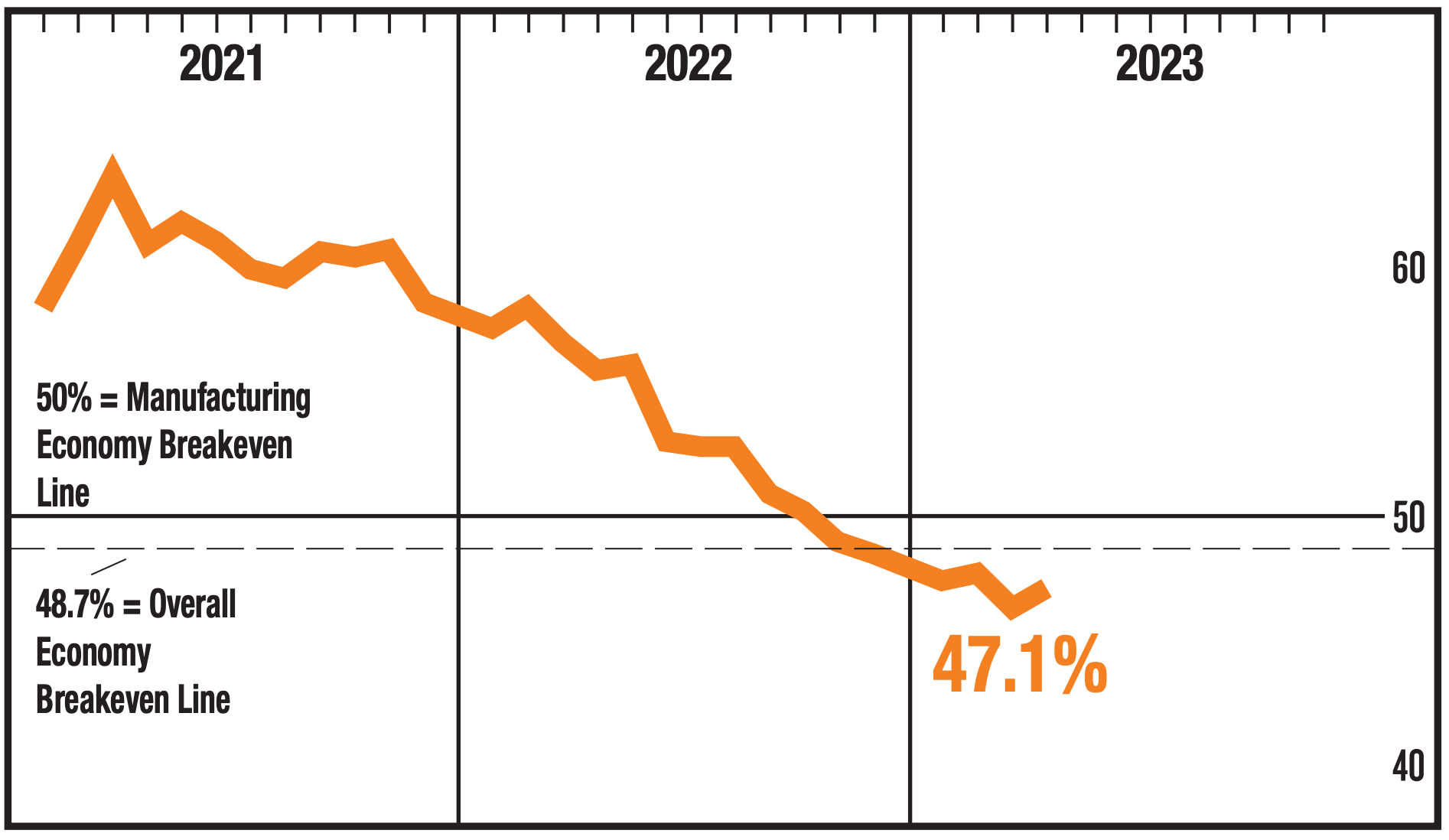

While the ISM’s April Manufacturing PMI (via Notes) signaled contraction for the sixth consecutive month, the headline index ticked up month-over-month with improvements in key categories including new orders, production, and employment.

(Source: ISM via Notes)

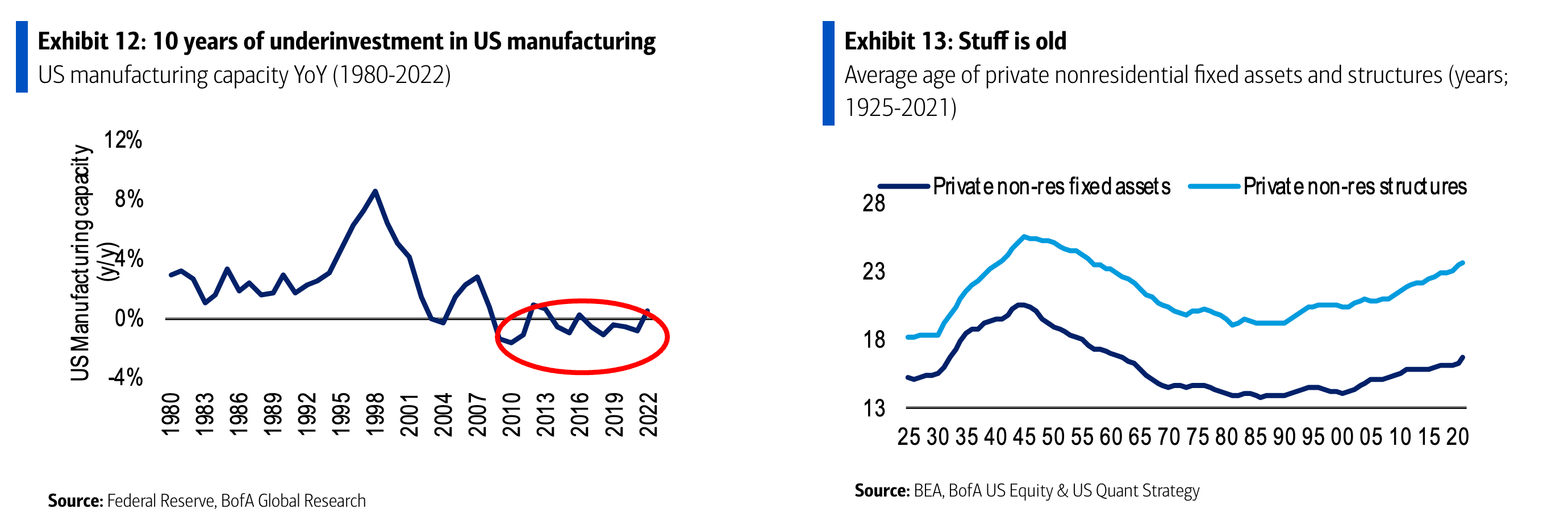

Outlook for business investment is bullish. From BofA: “We are bullish on capex, particularly in the old economy capex after 10+ years of underinvestment. Re-shoring is also big secular tailwind - mentions of re-shoring +128% YoY. But it might not be just the old economy capex. The emerging AI cycle suggests potentially an everything capex cycle — AI mentions +85% YoY. Tech capex accelerated to +39% YoY so far vs. +3% in 4Q, led by Microsoft. Overall, 1Q23 capex is tracking +9% YoY so far (down from +18% YoY in 4Q), but excluding GOOGL (-36% YoY in 1Q, but guided to flat YoY capex for the full-year 2023), capex is +13%.“

(Source: BofA via Notes)

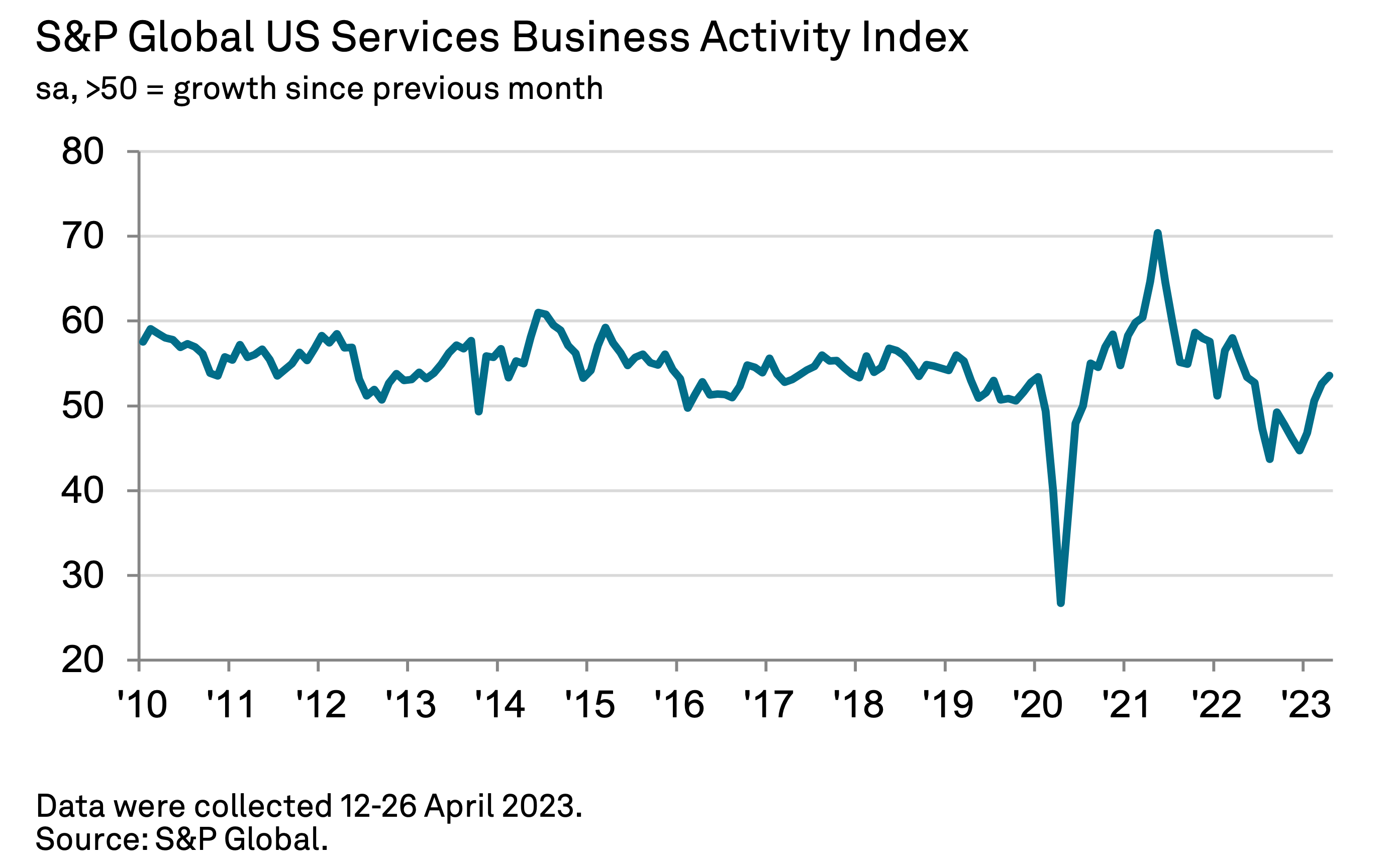

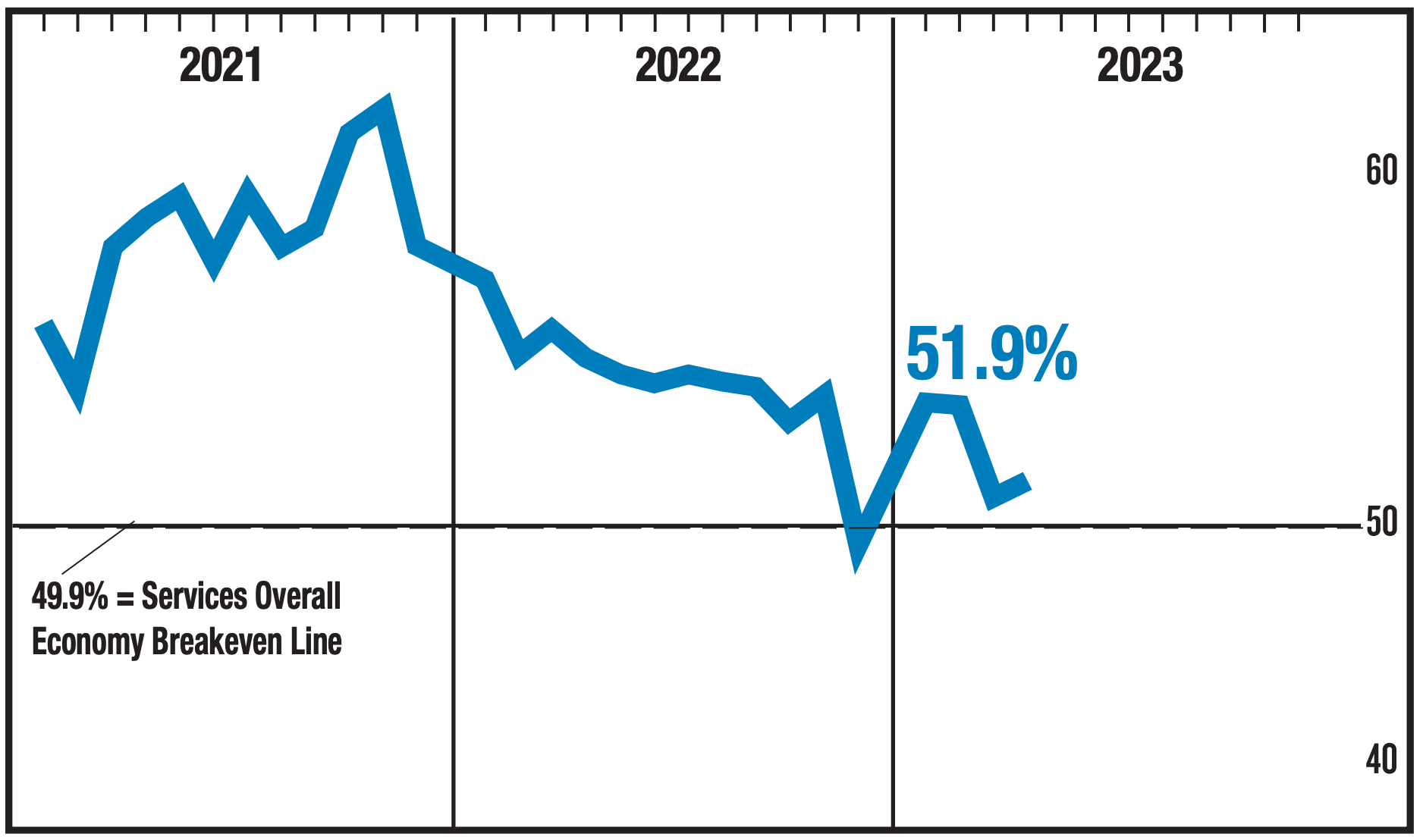

Services surveys improve. From S&P Global’s April U.S. Services PMI: “April saw an encouraging acceleration of service sector growth which, combined with indications of a renewed upturn in manufacturing, suggests the economy has regained some momentum at the start of the second quarter. Companies have reported an improvement in confidence compared to the gloomier picture seen late last year, with service sector companies also benefiting from a post-pandemic tailwind of spending shifting from goods to services, notably among consumers.“

(Source: S&P Global)

The ISM’s April Services PMI signaled acceleration in activity driven by improvements in new orders. Employment cooled but continued to signal growth.

(Source: ISM Services)

Supply chain pressures ease. The New York Fed’s Global Supply Chain Pressure Index

— a composite of various supply chain indicators — fell in April and is hovering at levels seen before the pandemic. It's way down from its December 2021 supply chain crisis high. From the NY Fed: “Global supply chain pressures decreased again in April, falling to 1.32 standard deviations below the index’s historical average. The March value was revised downward from 1.06 to 1.15 standard deviations below the index’s historical average. There were significant downward contributions from Euro Area delivery times, Euro Area stocks of purchases, and Korean delivery times. While the overall index declined, there was a notable upward contribution from Taiwan stocks of purchases.”

(Source: NY Fed)

For more on why normalized supply chains haven’t resulted in cooler inflation, read: What Fed Chair Powell said about the relationship between profit margins and inflation

Debt ceiling warning. Treasury Secretary Janet Yellen (via Notes) warned the U.S. could default on its debts “by early June, and potentially as early as June 1, if Congress does not raise or suspend the debt limit before that time.”

A version of this post was originally published on TKer.co

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.