Zinger Key Points

- Tesla appears to be refocusing on pricing as growth in deliveries slows.

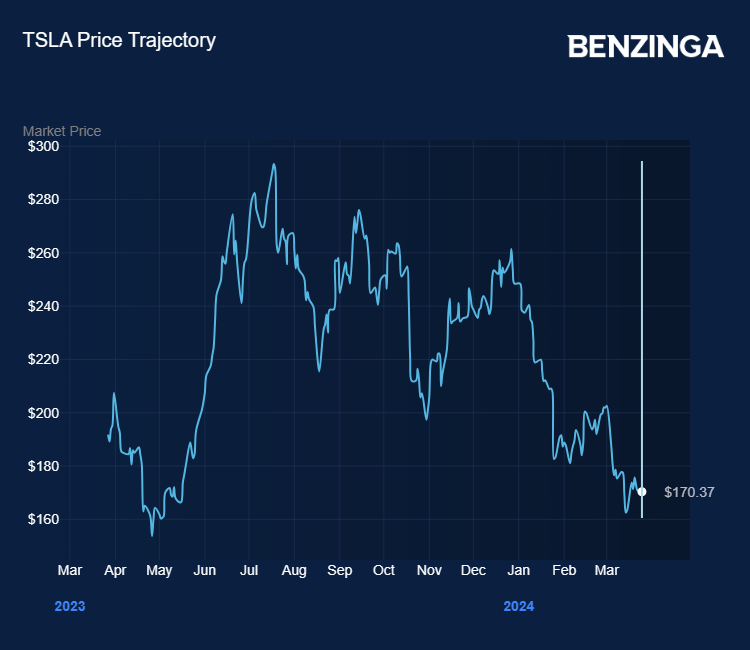

- Tesla stock is down nearly 32% so far in 2024.

- Get access to the leaderboards pointing to tomorrow’s biggest stock movers.

Tesla Inc TSLA appears to be changing its strategy after noting in its last quarterly earnings report that it was facing lower demand for electric vehicles and that delivery growth rates in 2024 would be “notably lower” than in 2023.

The company’s fourth-quarter earnings disappointed Wall Street expectations, with misses on revenue and profit as the company reported negative impacts from growth in vehicle deliveries that have lower average sales prices.

Tesla has already announced price increases in the U.S. and the eurozone for its most popular vehicle — the Model Y SUV.

Last week, the company announced plans to increase the Model Y’s price in the U.S. by $1,000 starting next month, and by up to 2,000 euros in certain Eurozone countries.

Also Read: Tesla Bear Wonders If Price Hike Warnings Are Signs Of Looming Production Slump

Latest Startup Investment Opportunities:

Production Slows

Meanwhile, there have been reports that Elon Musk is poised to announce Tesla is slowing production in China, partially due to competition from domestic producers such as BYD BYDDY and Nio Inc NIO, but also due to slowing growth in EV sales globally.

Colin Rusch, analyst at Oppenheimer, said: “With TSLA announcing planned price increases across geographies and reports surfacing about moderated production in China, we believe the company is working to deliver as many vehicles as possible before quarter end and managing supply/demand balance as it shifts focus toward maximizing value capture per vehicle away from unit growth.”

Is this a wise strategy, given that much of Tesla’s popularity has been built upon the relative affordability of its vehicles, compared with many of its competitors?

Rusch and his team at Oppenheimer believe that the company is setting the stage to increase the revenues it generates from software updates.

Rusch added: “We view TSLA as a leader in artificial intelligence for the physical world noting its leverage of uniform camera data into training systems for vehicles. We believe its wider release of Full Self-Driving 12.3 should accelerate training data collection and trigger incremental deferred revenue recognition in 1Q24.”

‘Transformational Technology’

Tesla’s stock has fallen nearly 32% in 2024, with the decline starting at the end of December, before the company’s weaker-than-expected results published on Jan. 24.

The Global X Autonomous & Electric Vehicles ETF DRIV, an exchange traded fund that tracks the makers of EVs and the chips and tech behind them, has performed better, but remains flat over 2024.

Oppenheimer lowered its 2024 delivery and revenue and profits estimates for Tesla, but retained its Perform market rating.

Rusch concluded: “We believe TSLA has the potential to be a transformational technology company and deliver outsized returns.

“We believe the company’s execution on Model 3 and Y volumes in the medium-term and cost reduction, largely from a battery perspective, are critical to realizing positive incremental operating margin and cash flow necessary to support sustainable profitability.”

Now Read: Tesla’s Growth Engine Stuttering? Deliveries Miss Looms As Analyst Questions High Valuation

Image generated using artificial intelligence with Midjourney.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.