Zinger Key Points

- KeyBanc holds AT&T at 'Hold' with mixed Q4 results; Verizon seen as more promising due to stronger subscriber and revenue growth.

- Oppenheimer and Raymond James optimistic on AT&T; highlight its successful shift to connectivity and potential in wireless and fiber.

- Today's manic market swings are creating the perfect setup for Matt’s next volatility trade. Get his next trade alert for free, right here.

KeyBanc analyst Brandon Nispel maintained a Hold rating on AT&T Inc T.

The analyst noted that the 4Q results were mixed. Total Wireless service revenue in Mobility and Business Wireline revenue were below expectations, and adjusted EBITDA was below consensus for these two segments.

While subscriber phone net adds of 526K beat expectations, phone net adds decelerated year-on-year.

From his point, 2024 guidance appears achievable but not necessarily conservative or beatable.

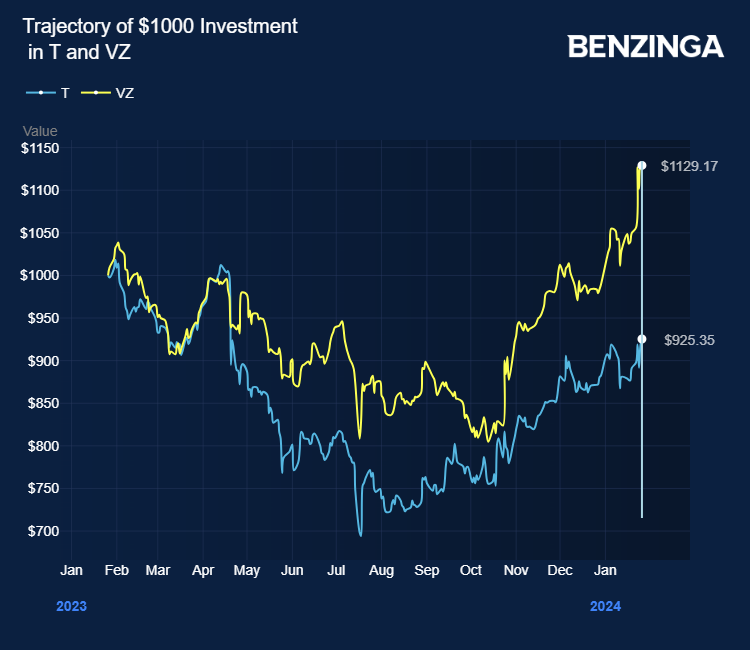

The analyst noted better prospects for Verizon Communications Inc VZ, which is accelerating subscriber growth, Wireless service revenue growth, and adjusted EBITDA growth.

Verizon’s more incredible broadband subscriber growth and less exposure to Business Wireline provide a higher-quality asset base. Verizon’s free cash flow is of higher quality, given AT&T’s contribution from DTV.

The analyst projected first-quarter revenue and EPS of $30.53 billion and $0.51 for AT&T.

Oppenheimer analyst Timothy Horan maintained a Buy rating on AT&T with a price target of $21.

Horan noted that AT&T has successfully transitioned itself to a pure connectivity provider, a 2-3 year process that pressured it to underperform the market and peers.

It has significantly improved its wireless network, which covers 210 million+ POPs with the mid-band spectrum, and is now selling FWA to monetize excess capacity.

AT&T is also the most significant and fastest-growing fiber builder, which supports unique converged cross-sell opportunities.

Positively, management signaled it is looking to get more aggressive in underpenetrated markets in SMB and value-oriented consumers. AT&T has had the most consistent go-to-market offer, likely helping keep churn low and keeping flowshare relatively stable compared to peers.

Horan noted AT&T’s 15% fiscal 2024 free cash flow yield and ~7% dividend yield as attractive. He projected first-quarter revenue and EPS of $30.81 billion and $0.55.

Scotiabank analyst Maher Yaghi had a Sector Outperform rating with a price target of $22, up from $21.

The analyst’s valuation approach in telecom is based on free cash flow and not EPS. After analysis of AT&T’s results, he tweaked his free cash flow estimates higher for 2024 and 2025.

His estimated year-end net debt/EBITDA for both years is also lower. The improvement in cash generation is supported by continued growth in EBITDA, and the cadence for free cash flow generation in 2024 will likely be less back-end loaded vs. 2023—all positive signals, as per the analyst.

As a result of his estimate changes, he had slightly increased his target on the stock given the attractive valuations of the shares trading and a dividend yield of 6.5%. The analyst projected first-quarter revenue and EPS of $31.42 billion and $0.53.

Raymond James analyst Frank G. Louthan reiterated a Strong Buy rating on AT&T with a price target of $25.

The analyst noted AT&T as undervalued with upside potential backed by the wireless growth and free cash flow ramp, bringing investors back to the name.

The two critical factors that move the carriers’ stocks are wireless subscriber growth and earnings growth, and AT&T is guiding to a decline in earnings this year, the analyst flagged.

Louthan noted that the additional pressure should be a low point as Nokia Corp NOK accelerated depreciation and the last two years of capital spend began showing up. EPS will likely return to positive, operational-driven growth in 2025.

Favorably, free cash is growing and will likely fall within the $17 billion – $18 billion range, which would be slightly up year-on-year, though below his prior estimate of $18.8 billion.

Price Action: T shares traded higher by 0.17% at $17.21 on the last check Friday.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.