One of the best experiences I’ve had in my investment career was being partner and co portfolio manager with Raji Khabbaz. He’s a fantastic stock-picker and the two of us spent the better part of a decade discussing and debating investment ideas. Early in 2020, we spent a lot of time talking about Covid, trying to figure out how to position our portfolios for a potential disaster. No one knew how bad things would be or how long the problem would last.

There wasn’t a lot of data available at that point, but you could track the number of reported cases out of Wuhan, China on a daily basis. At the time, I remember the number of reported cases was around 80 thousand. The problem with that number is Wuhan has a population of over 12MM people, and the only places that were operating around the clock there were the hospitals and crematoria. I read reports of half a million cremation urns being delivered to Wuhan for a virus that has a survival rate well above 99%. There was no possibility that the city had only 80k cases. The numbers were clearly lies made up by the CCP (Chinese Communist Party) to make the situation look better than it was.

At one point, Raji and I were debating the numbers. I told him that I thought the 80k number and all Covid-related statistics out of China were lies. Raji agreed and still thought the virus reports were worth tracking. He suggested that seeing the rate of change might have predictive value. My response was that if the numbers are lies, why would we believe the CCP would give us anything that had value? There’s no rule that says that when someone lies to you, they have to lie in a directionally correct way. Raji acknowledged that point and then noted that right or wrong, the market was watching those numbers and that stocks were moving based on them.

On that point, we were in complete agreement. Wall Street is a weird place, and people will often trade based on numbers that are inaccurate simply because other people are trading based on those numbers. For those of you wondering why I’m leading with this story, it’s because we’re about to discuss the Federal Reserve and interest rate projections.

DKI Read the Fed Right:

Asset gatherers and others who benefit from price bubbles have been crying for the Federal Reserve to “pivot” to lower rates for the past two years. I’ve spent those two years saying the opposite. At DKI, we’ve understood that inflation is not under control, and that the Fed intended to deliver on “higher for longer” interest rates. Coming into 2024, market expectations were for six rate cuts with the first one in January or March. I said that wasn’t going to happen. When the market modified that to three cuts starting in June, DKI was clear in saying we were taking the “under” on rate cuts.

In the past two weeks, a CPI print came in both above expectations and above the prior month meaning we have accelerating inflation. Chairman Powell gave a hawkish speech indicating the Fed isn’t even considering lowering rates right now. More hawkish Fed Governors have said they think they might not need to cut rates at all this year. And even the more dovish Governors are now acknowledging that now is not the time to lower interest rates. (Hawkish means favoring higher interest rates. Dovish means favoring lower interest rates.)

As I write this, the NASDAQ has been down 5 of the past 6 trading days. It’s declined almost 7% in that time. After a year and a half of rising market indexes largely due to expectations of coming rate cuts, investors are starting to realize that higher inflation and higher rates are going to be with us for longer than they thought.

The bad news is this is going to create hardship for many Americans and is terrible for the country. The good news is that even in a bad economy, we’re still finding ways to invest successfully. DKI started writing about inflation in November of 2021. What I’m proud of is that instead of just pointing out the problem, we helped our subscribers invest in assets that have benefitted from higher inflation. If you want help protecting your portfolio from this kind of challenging environment, you’re welcome to subscribe. (Sorry for the intra-letter commercial, but we did a survey and found out that people who don’t read DKI materials don’t subscribe.)

We’ve made money by correctly predicting the actions of the Federal Reserve, but does that mean the Fed knows what they’re doing? Absolutely not.

The Blind Leading the Confused:

A quick and dirty summary of recent market reactions to the Federal Reserve looks like this: The Fed keeping the fed funds rate at or around zero combined with multiple rounds of quantitative easing created a large asset bubble in stocks, housing, cars, watches, and other luxury items. Fed rate hikes starting in January 2022 caused both the stock and bond markets to decline. Later in 2022 and through the beginning of 2024, expectations of coming Fed rate cuts (combined with incredible performance from a few mega-cap technology firms) sent the market back up to all-time highs. This happened despite the Fed neither cutting rates nor saying they would any time soon. Finally, a rising CPI combined with rapidly climbing interest expense, and some hawkish comments from Fed Governors in front of microphones, led the market to begin to fall again.

It's clear that just like the Covid infection numbers out of Wuhan, the market responds to its interpretation of what the Fed will do or what people think the Fed should do. Few people are asking the question of whether the Fed has any idea what they’re doing, or do they make things up as they go along. Fortunately, the Federal Reserve releases the “dot plot” four times a year. In the dot plot, Fed Governors make their predictions regarding their near-term and longer-term expectations for the fed funds rate.

If Fed Governors knew what they were doing, and their analysis was predictive, we’d see interest rates a year or two out match the prior dot plots. If Fed Governors have no idea what they’re doing, then we’d expect to see a wide divergence between Fed projections and future results. Because the dots on the dot plot are anonymous, we can evaluate the data without engaging in any political or personal narratives. The projections either turn out to be close and right, or divergent and wrong.

For recent years, we track the change in the Fed’s opinion of future interest rates. We calculate the mean, the median, and the mode. We track all three statistical averages because the opinions of individual Fed Governors differ wildly. Even though the Fed typically moves interest rates .25% at a time, it’s common for dot plot estimates to be multiple percentage points apart. The mean is the average of all dots in the dot plot. That means that a couple of Fed Governors who have opinions far above or below their peers have an outsized influence. The median is the center point where half the Governors surveyed will be above the estimate and half will be below. The mode is the most common answer.

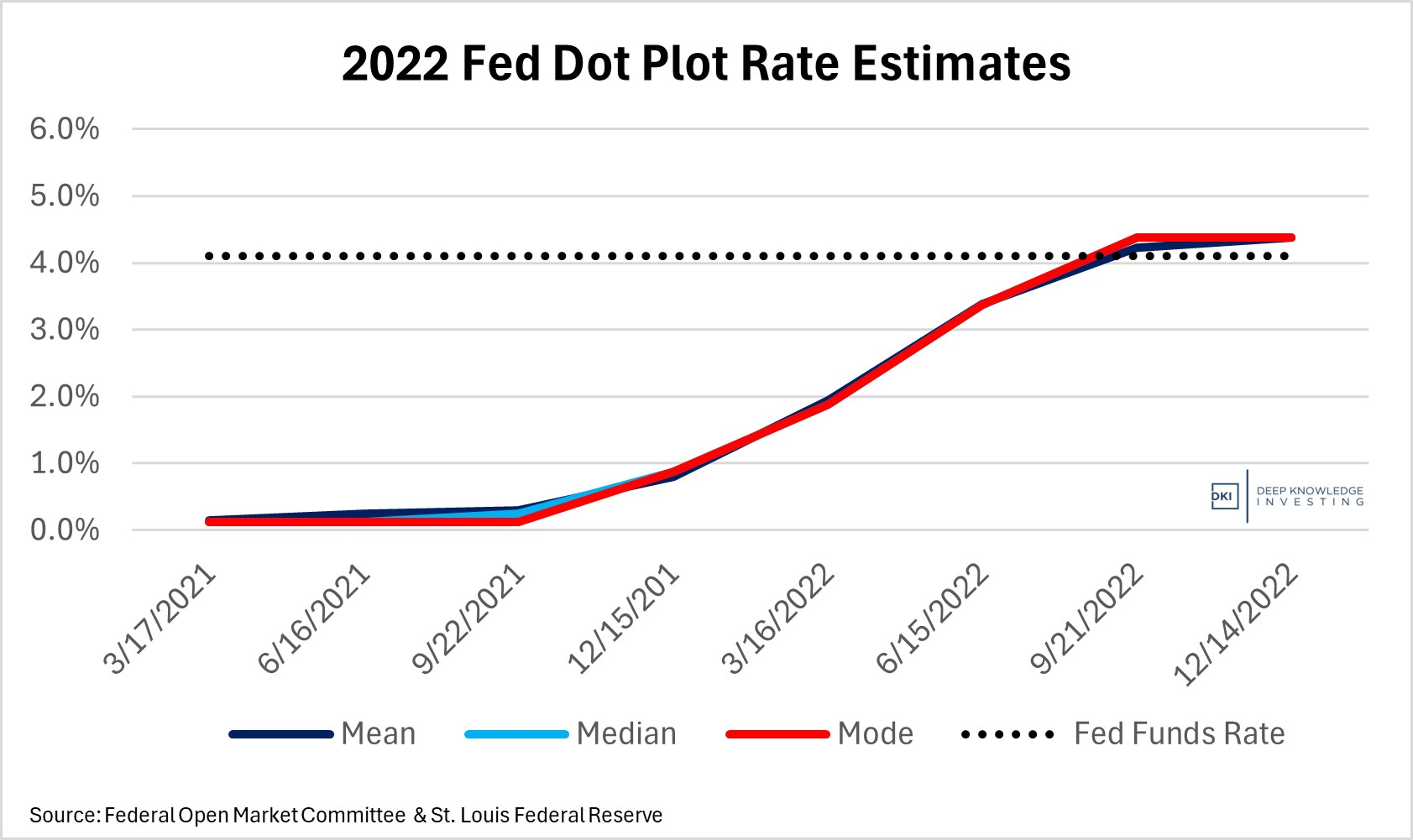

2022:

Three quarters into 2021, the Fed expected interest rates to remain just above zero. This was when Chairman Powell, and Treasury Secretary, Yellen, were still saying inflation would be transitory. By the end of 2021, the Fed still expected rates just a year later to be below 1%. In January of 2022, the Fed began its hiking cycle and by the end of ’22, the fed funds rate was at 4.1%. Worth noting: Not only were committee members off by approximately 4% a year before the end of 2022; but also, it wasn’t until three months before the end of the year that the Fed dot plot was accurate.

Summary: Wrong by more than 4% one year out. Still wrong six months out. I offer a reminder that these projections came from the most senior and powerful economists in the United States. The conclusion is that 2022 was an epic failure for the Committee.

2023:

In early 2021, we started tracking Fed projections for the end of 2023. The median and the mode were right around zero meaning most Fed Governors expected rates to stay ultra-low through the end of ’23. The higher mean is because a smaller number of Governors anticipated a limited increase in rates. Again, it took until early in 2023 for the Fed to get locked in on the 5.3% rate where they ended the year.

Summary: Wrong by more than 5% from the beginning of the chart. This time, the Committee was pretty close about a year in advance. Still not great, but better than in 2022.

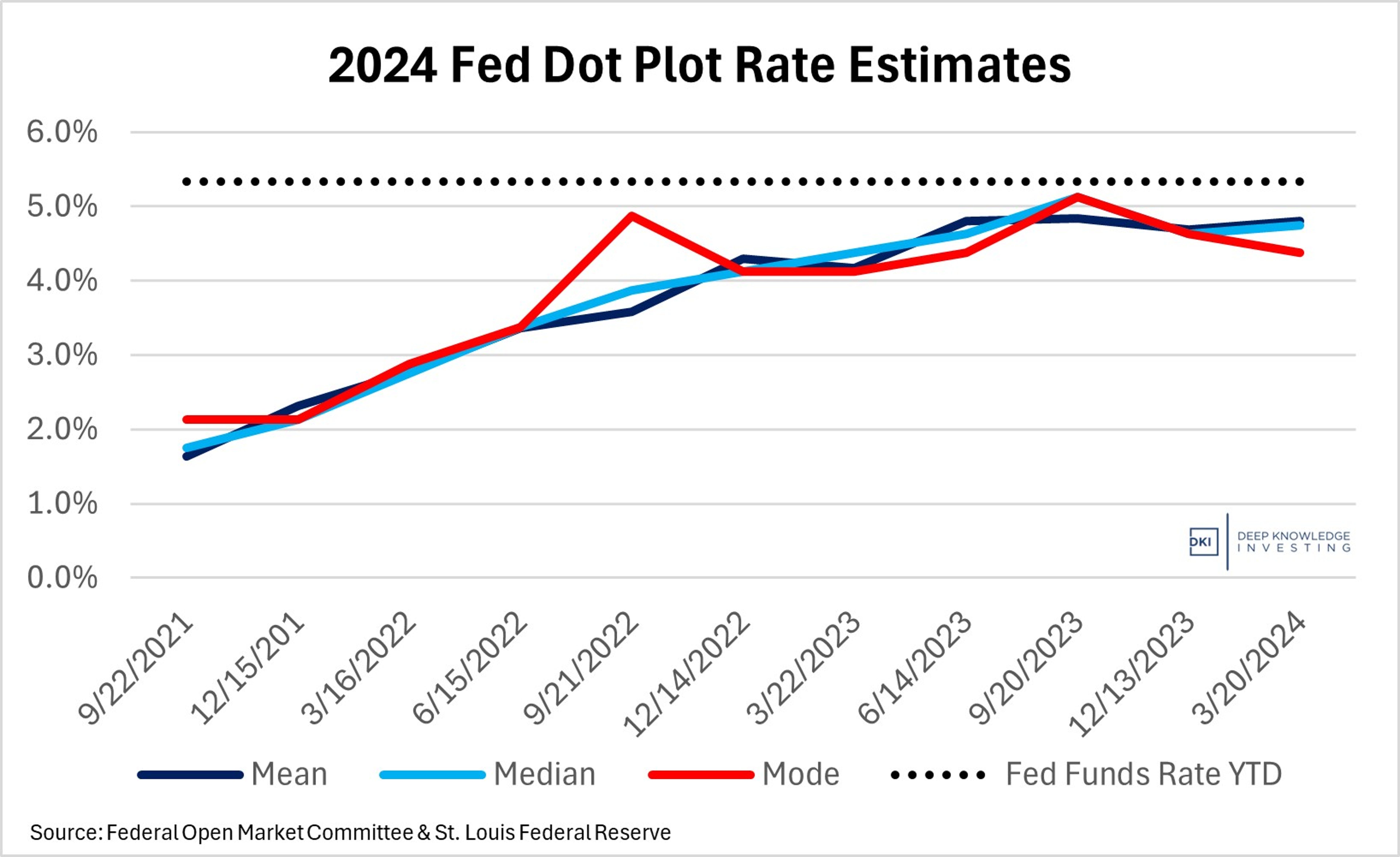

2024:

While we don’t have a final fed funds number for 2024, this graph shows how inaccurate the Committee has been. The first 2024 estimates became available in late 2021 and were more than 3% below the current (and projected) fed funds rate for the end of this year. By late 2022, several members of the Committee began to realize that higher for longer was going to extend well into 2024. That’s why the mode approached the current fed funds rate in September of ’22. Then, everyone started to get more dovish until raising projections again in late 2023. It’s an easy bet that the next dot plot is going to be more hawkish than the one we saw in March of ’24.

Summary: Not a good job by the Committee. They were off by more than 3% to start. A few Governors started to get a handle on things a year later, but by the end of 2022, they were still off by more than 1%. That’s a big difference for an institution that tends to make .25% incremental changes.

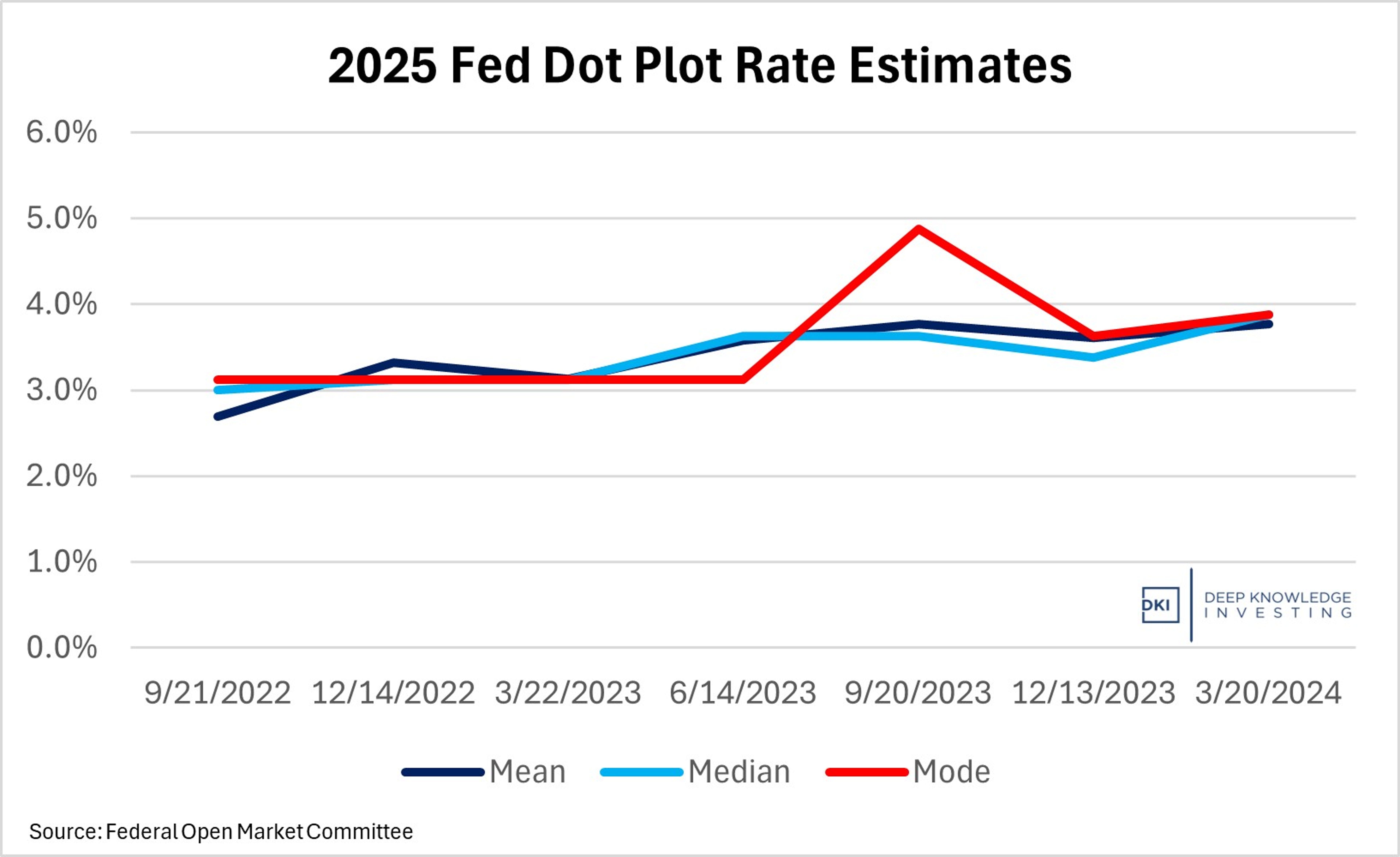

2025:

Within just a year, estimates for the 2025 fed funds rate moved by more than 2%. Right now, the Committee expects rate cuts of around 1.5% over the next 20 months. If there’s one thing that is clear from the rest of this section, the Fed has no idea what interest rates will be next year.

What do we do with this:

Despite having inside information on their own process, the Federal Reserve is unable to predict interest rates even a short time in the future. While that limitation is apparent, the market still trades up and down based on what an individual Fed Governor is saying on a particular day. What do we do when the market is using a non-predictive metric to set asset prices?

In our case, we’ve been able to use Fed-speak to make money because they’ve provided a framework for how they make interest rate decisions. As early as 2022, it was clear that Chairman Powell wanted to be the next Paul Volker, the former Fed Chairman who raised the fed funds rate to almost 20% to kill inflation. He didn’t want to be the second coming of Arthur Burns, Volker’s predecessor who relaxed interest rates too soon before getting inflation under control.

To us, that meant that as long as inflation continued to be an ongoing problem, we could count on the Fed to maintain its policy of “higher for longer”. As long-time DKI readers know, we were early and right that inflation is not transitory, not under control, and has been understated. While everyone in Washington DC wanted to blame Covid, supply chain disruptions, and President Putin, DKI understood that the true cause of inflation was massive money-printing out of DC. That left us with a clear view of the real inflation problem and an understanding of how the Fed would react to that data once they started to see what we saw.

This is how we used an unreliable dot plot that is not and will never be predictive to make money for our subscribers. We didn’t need the Fed to be accurate. We just needed to know how they’d respond to future data. As a result, we set up the DKI portfolio to benefit from higher inflation which has paid fantastic dividends to the community here. Or as DKI subscriber, David, humorously described it:

Do you want to be miserable about inflation, or do you want to make money from it?

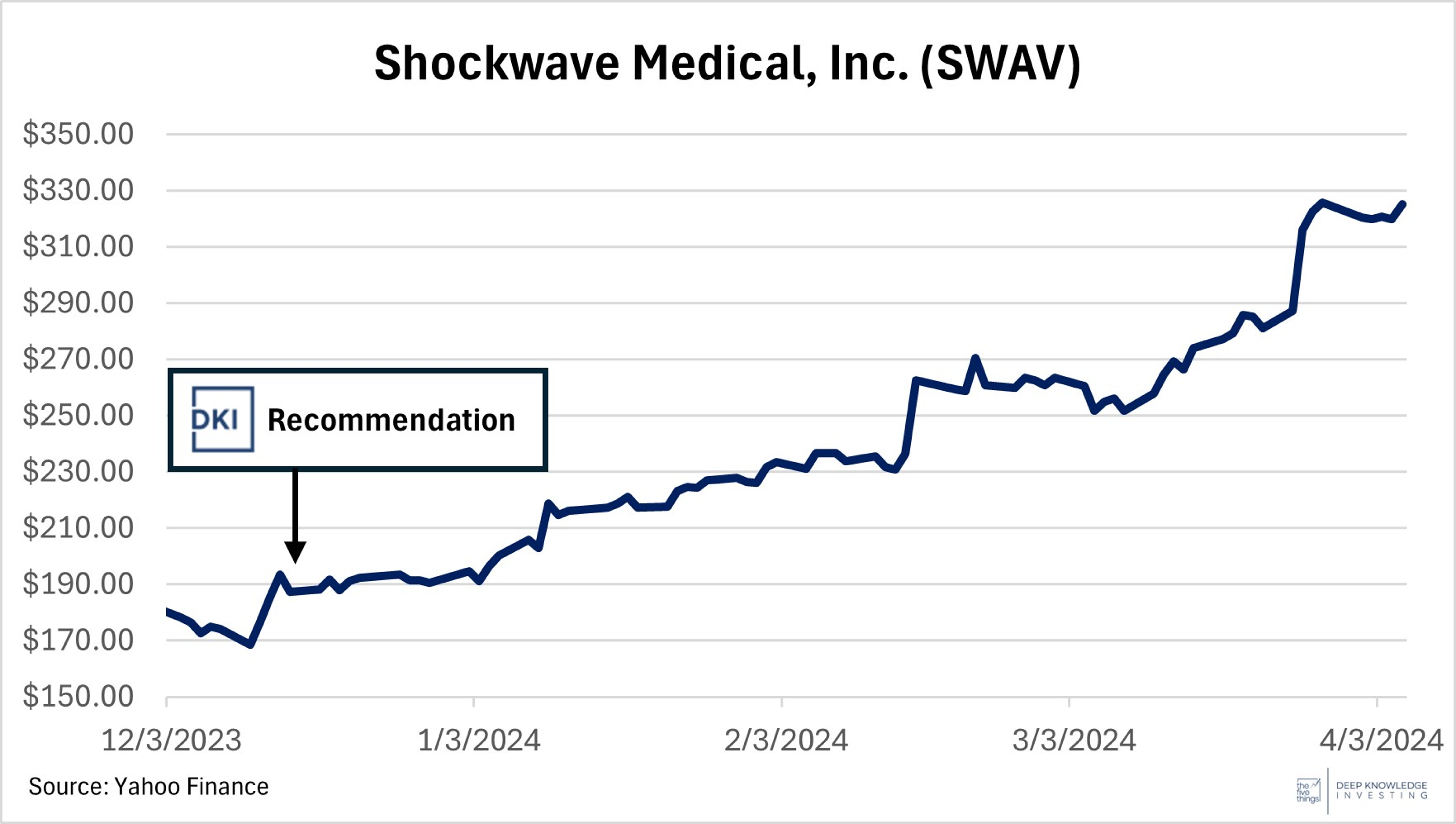

Shockwave ($SWAV):

DKI recommended medical device company, Shockwave Medical SWAV in December at $190. Our thesis was that the company would be bought for more than $300. Earlier this month, Shockwave signed a definitive agreement to be acquired by Johnson & Johnson $JNJ for $335 in cash. DKI subscribers made more than 70% in under four months.

Credit to Dr. Paul Thompson and the DKI Board. This was a team win.

We’d like to offer a round of applause for cardiologist and DKI Board Member, Dr. Paul Thompson and interventional cardiologist, Dr. Dan Fram, who were instrumental in suggesting the idea and explaining the medical implications of Shockwave’s devices. They generously did a webinar for DKI subscribers explaining $SWAV’s technology and why the company had the best solution for cardiac stents that were difficult to place due to excessive calcification. That clarity enabled many of us to take larger positions in what turned out to be a huge money maker.

This is the second DKI portfolio company to be acquired following Houghton Mifflin which was bought for more than 4x DKI’s initial purchase price. If that’s of interest to you, you’re welcome to subscribe. Otherwise, we’ll be happy to keep informing you after the fact. The next portfolio addition will be available to subscribers in the next few weeks.

Time to Wrap it up for This Month:

DKI has started to partner with sponsors to reach our growing audience of investors and financial professionals in the weekly 5 Things and these monthly letters. If you’re interested in connecting with hundreds of family offices and thousands of individual investors, please reach out at IR@DeepKnowledgeInvesting.com. The open rate for our emails is around 2x – 3x the industry norms.

DKI has started to increase our video content focusing on each week’s 5 Things to Know in Investing. Robb Fahrion of Flying V has been a fantastic host, and intern, Andrew Brown, continues to find ways to improve video quality and distribution. Andrew has also started to write part of the 5 Things and is becoming a regular on-air guest on the video version. For those of you who prefer watching to reading, please check out our YouTube channel and feel free to leave your comments and thoughts there as well. Recent guests have included Tracy Shuchart on declining oil inventories and Enrique Abeyta on predictive signals in technical investing. DKI Board Member, Howard Freedland joined us with some thoughtful and calming commentary on the new real estate broker commission rules. Check out who we have lined up to join us on camera in the coming weeks.

DKI has a partnership with Tidal (@leadlagreport on Twitter). If you’re a financial advisor with more than $50MM under management, please reach out to us so we can arrange for you to get a premium subscription to Deep Knowledge Investing at no cost to you through Tidal. Michael Gayed runs the program, has been a great partner and friend, and is an expert on conditions-based investing. A chat with him and a subscription to DKI both provide great value

and definitely qualifies as a store of value.

If any of you have questions, concerns, or thoughts regarding issues we should address in a future depth report, please feel free to reach out to me at IR@DeepKnowledgeInvesting.com.

If you think a friend, RIA, family office, or portfolio manager would be interested in this monthly commentary, please feel free to pass it on to them. Also, if you send this letter to more than 5 people, please get in touch and let me know.

Thanks for being part of Deep Knowledge Investing,

Gary Brode

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.