Mark Twain once quipped, “Everyone complains about the weather, but no one ever does anything about it.”

Well, these days everyone probably would complain about inflation if it ever reappeared in a major way, but the Fed promises it won’t do anything about it until employment is on track toward whatever “normal” was before the pandemic.

As Wall Street analysts expected, the Fed didn’t change rates or make any other policy changes coming out of this week’s Federal Open Market Committee (FOMC) meeting that ended this afternoon. Rates stayed near zero, where they’ve been for over a year, and the Fed remains committed to its $120 billion a month bond-buying program designed to keep borrowing costs low and refuel the economy coming out of the pandemic.

At first blush, this looks like a pretty dovish meeting, and Fed Chairman Jerome Powell made clear the Fed isn’t talking about any decline in asset purchases or increase in rates. There were three things investors were curious about going in—asset purchases, rates, and inflation—and Powell was dovish on all of them.

Treasury yields actually began to fall as the Powell press conference went on this afternoon, with the 10-year yield edging down toward 1.61% to 1.62%. That’s down a few basis points from this morning’s two-week highs.

There was no change to the Fed’s commitment, outlined last month, to basically stand on the sidelines “for some time” if year-over-year inflation stays “moderately” above what has been the Fed’s long-term goal of 2%. Core inflation, per the Personal Consumption Expenditure (PCE) prices report, was 1.4% in February, the most recent month tracked. However, consumer prices are already rising more than 2% on a year-over-year basis.

Optimism Club: Fed Sees Positive Signs For Economy

There were a couple of changes in the Fed’s statement from last time, with the Fed now saying employment has “strengthened.” Arguably, you could see that as an improvement from “turned up” in its March statement. The statement noted some inflation, but again said it’s likely to be “transitory.” March consumer prices rose 2.6%, the highest year-over-increase since August 2018.

In another change, the Fed’s statement now says sectors most adversely affected by the pandemic remain weak, but have “shown improvement.” The public health crisis still weighs on the economy, the Fed said, but no longer on employment or inflation.

Still, inflation doesn’t seem to be a really big concern now for the Fed, judging from how the statement and press conference went. They seem basically comfortable with inflation staying above 2% for the rest of the year because that will be against very easy comparisons to a year ago, when we had the big slowdown due to Covid. The Fed apparently believes we’ll have to wait until next year to get a reliable sense of what inflation is doing

The stock market had been mixed earlier Wednesday and stayed that way after the Fed’s decision and as investors waited for Powell to start his press conference. The S&P 500 Index (SPX) actually made up some ground and turned green after the statement. Earnings continue to be solid but the SPX hadn’t really gone anywhere since earnings season started, possibly an indication that a lot of the strength in earnings was already built in.

Basically, this meeting looks like a placeholder. That means attention could focus more on the big earnings reports from Apple AAPL and Facebook FB coming up later today, along with the gross domestic product (GDP) report and Amazon AMZN earnings due tomorrow.

One thing Powell isn’t ready to do is chip around the edges of the Fed’s program to support the economy.

Asked directly in his press conference if it’s time to taper its $120 billion bond-buying program, Powell replied, “It is not time.” He added that the Fed has promised to give investors plenty of warning before that starts to happen and that it will continue the pace of asset purchases until it sees “substantial further progress” on its goals.

“Economic activity in hiring just recently picked up and it will take time before we see substantial further progress,” Powell said.

Everything Powell and company said today needs to be seen in the light of data they (and investors) didn’t have six weeks ago when the Fed last met. March jobs growth of 916,000, accompanied by a 9.8% jump in March retail sales, probably helped shape the Fed’s thinking ahead of Wednesday’s announcement. Vaccination progress and the stimulus checks also have affected the economy since that March meeting, so it’s interesting to see how that affected the Fed’s outlook.

Despite all the improvement, remember that the Fed has its eye on the “adjusted unemployment rate,” which includes laid-off workers incorrectly classified as “employed but not at work,” in addition to those who have recently dropped out of the labor force—meaning those who’ve stopped looking for work, Barron’s noted.

As of March, the adjusted unemployment rate had declined to 9.1%. That’s a long way from the official 6% unemployment rate, and far, far from full employment. It’s numbers like this that the Fed is trying to balance with some of the more sparkling recent economic and earnings data. In his press conference, Powell noted the uneven improvement in employment, especially in the services sector. Progress ahead, he said, depends on progress against the virus.

Fed Foot Seen Off The Inflation Brake

This twist in Fed policy, where it waits to respond to inflation instead of trying to get ahead of it through any tapering of its $120 billion a month of bond buying (let alone raising rates), appeared to confuse Wall Street after the Fed announced it last month.

Initially, the 10-year Treasury yield continued rolling up gains, reaching a post-Covid high of 1.78% at the end of March. Then it paused, falling to near 1.5% by mid-April. This might have been more of a pause after the long rally, not necessarily a response to the Fed. Or maybe it indicated falling inflation worries because of the Fed’s continued reassurance that any inflation would be “transitory,” to use “Fed-speak.”

Now, the pendulum is swinging slowly back. The 10-year yield touched 1.63% heading into today’s Fed meeting, up nearly 10 basis points from last week’s low and the highest reading in two weeks. What gives?

As we noted in this morning’s column, the sudden change might reflect investors coming to realize that the Fed is serious about sitting back and letting inflation rise. Maybe there were doubts at the beginning, but nothing anyone at the Fed has said since the mid-March meeting sounded much different, so the central bank isn’t just jawboning. Despite initial skepticism, the Fed really seems serious about letting inflation run, so now it appears the market is building in more expectations for rising prices.

Additionally, announcements from companies including 3M MMM and Coca-Cola KO that they’re feeling the impact from higher raw materials and logistics costs, might also factor into the recent yield rise.

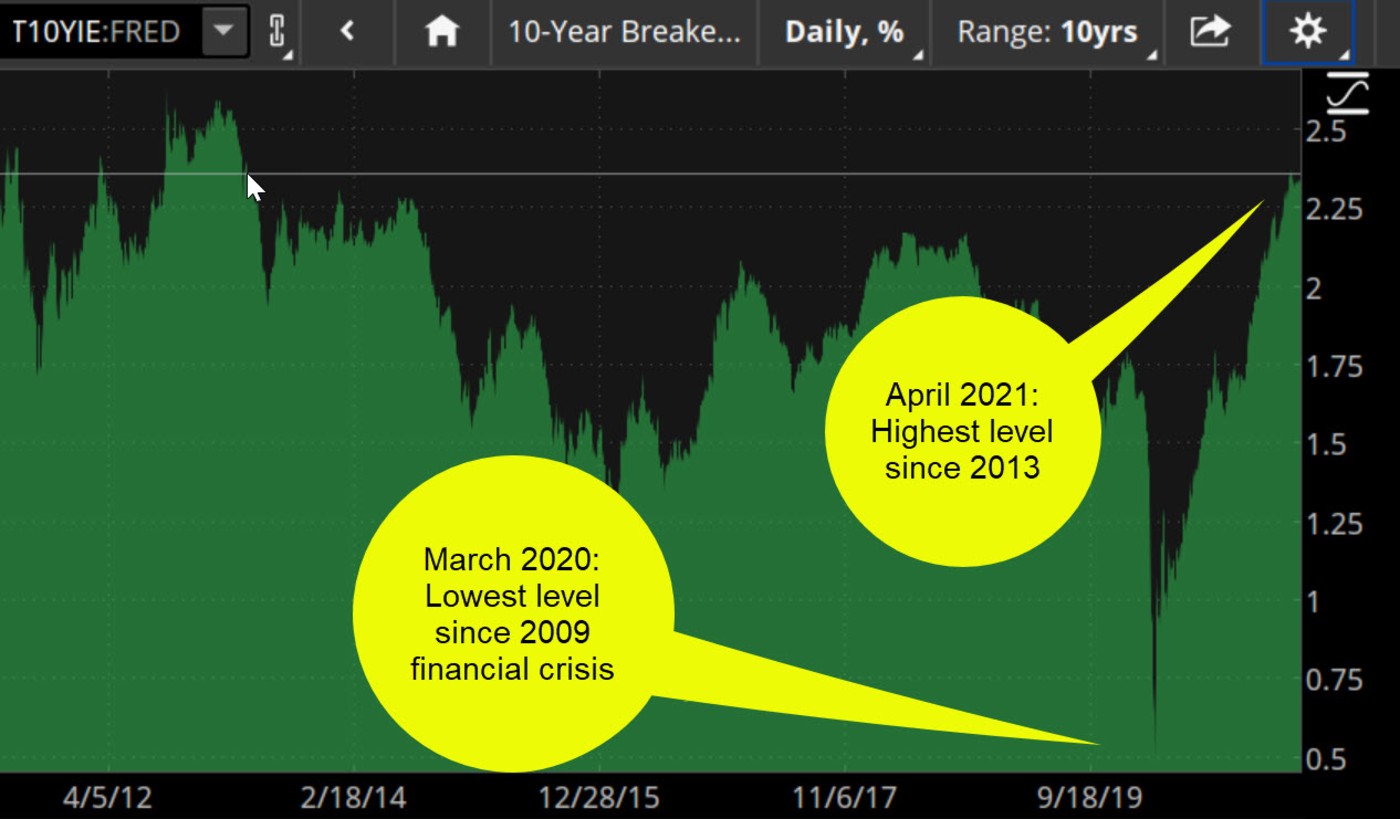

You can see how investors reacted if you track the 10-year breakeven inflation rate. It recently rose above its late-March peak and crossed above 2.38%, the highest it’s been since 2013 (see chart below).

Yield Climbing Even If Fed Stands Still

The market is continually pricing in higher inflation, and that trend seems to be moving higher and has recently popped. It had sort of topped out with a projected inflation rate of 2.35% back in March, but it’s finally above a level it couldn’t get above before.

Where does this potentially take us? Well, maybe back toward a possible test of the 1.78% high recorded by the 10-year Treasury yield a month ago. Most analysts see the yield at well above 2% by a year from now, according to Barron’s. The wild card in the near-term may be overseas rates. The 10-year yield’s premium to the benchmark German Bund yield remains very wide, a factor that may draw investors into U.S. bonds and keep pressure on yields here, at least in coming weeks.

At the end of the day, investors will probably want to know what all this might mean for the stock market. Traditionally, higher yields mean tougher times for growth stocks like Technology, while signaling a stronger economy that could help cyclicals like Financials and Industrials. Over the last month, those two sectors have trailed the big growth ones like Technology and Communication Services. Maybe the wind is shifting.

CHART OF THE DAY: TIRE PUMP. Market conditions—and some encouragement from fiscal and monetary authorities—have pushed the 10-year breakeven inflation rate to above 2.3% in recent days, the highest level since 2013. Quite an accomplishment considering the rate had fallen to a post-financial crisis low at the front end of the Covid pandemic last year. Breakeven inflation is the 10-year average inflation implied by the market, calculated by subtracting the current 10-year rate in Treasury Inflation-Protected Securities (TIPS) rate from the 10-year Treasury rate. Data source: Federal Reserve’s FRED database. Chart source: The thinkorswim® platform. future results. FRED® is a registered trademark of the Federal Reserve Bank of St. Louis. The Federal Reserve Bank of St. Louis does not sponsor or endorse and is not affiliated with TD Ameritrade. For illustrative purposes only.

No Bronze Medals: Earnings continue to look very good, but companies aren’t getting rewarded much for beating estimates. Take the example of Goldman Sachs GS, which absolutely crushed expectations earlier this month and saw its shares barely rise. Meanwhile, companies that miss on earnings or especially on revenue are getting hurt more than companies that exceed are being helped.

Beyond the numbers, what investors arguably want to hear is a good story going forward. Facebook FB, Amazon AMZN, and Apple AAPL—all of whom report today and tomorrow— are three of the biggest companies by market cap, so it’s very important for investors to pay close attention to what they say about the coming quarters. At this point, you can’t get away with not giving future projections. Those companies that decline to put out new guidance will likely continue getting hurt.

Taking the Long View: We’re caught up in worries about an overheating economy, partly because Wall Street is so focused on the here and now. This emphasis on the quarter or the year, rather than the long-term, can sometimes cloud investors’ views of things that matter down the road. Take the Census announcement this week, which showed the U.S. population growing just 7.4% in the last decade, the lowest for any decade since the Great Depression. This isn’t necessarily good news for investors.

As the Washington Post pointed out, we have an “aging population and fewer new workers than needed to generate economic growth (and) pay taxes…” While the U.S. economy remains dynamic and there’s still lots of entrepreneurial power, lack of population growth could be one reason for the slowing economies of Europe and Japan over the last few decades. No one’s saying that’s about to happen here, but it’s worth keeping in mind when you consider relatively weak gross domestic product growth since the financial crisis of 2008.

Key Inflation Read Too Late For Fed: We’re not done with data yet this week. Key inflation readings are due Friday with the March Personal Consumption Expenditure (PCE) price report. It’s kind of a shame the Fed didn’t get to see this ahead of today’s meeting conclusion, since it’s a report the central bank is known to keep close tabs on. They’ll have to wait like the rest of us. Last time out, in February, PCE prices barely registered, with the headline up 0.2% and core up 0.1% month over month. For March, that’s expected to change, with Wall Street’s consensus projecting 0.5% headline growth and 0.3% core growth, according to research firm Briefing.com. Core, if you remember, is the number after subtracting volatile food and energy prices. Also, keep an eye on the year-over-year inflation reading. It’s been 1.4% or 1.5% since last October. That’s a number we might see jump over coming months as it compares with Covid-weighted weak inflation from last spring.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image Sourced from Pixabay

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.