The lame-duck Congress has a bill.

A coronavirus relief bill that is. Lawmakers passed an $892 billion stimulus package that includes funds for small businesses, bolstered unemployment benefits, $600 direct payments for most Americans— including dependent children—and a bailout for airlines.

Now it goes to the president, who’s expected to sign it into law, giving Main Street a lifeline amid economically damaging restrictions to combat the United States’ third wave of COVID-19.

Wall Street seems to be cheering the development, in hopes that the package might be enough to stave off the worst economic damage until vaccines can be widely distributed. It’s hoped that the stimulus package and vaccine rollouts will stimulate consumer spending, with the latter also freeing up businesses to re-open to pre-COVID levels.

But this morning the optimism seems relatively muted. Perhaps there are some lingering concerns about a new variant of the coronavirus that has prompted much of England to lock down and European Union countries to ban travel from the United Kingdom.

If that weren’t enough unsettling news from the U.K., the nation still hasn’t finalized a trade agreement with the European Union just days before the Brexit transition period is set to expire, casting uncertainty about the health of the European economy that’s in addition to coronavirus worries.

This morning, it seems like there’s still some momentum left from the impressive recovery in stocks yesterday. However, it does seem that there’s a bit of a tug of war between the risk-off and risk-on camps, as gold and the Cboe Volatility Index (VIX) are down but the dollar is up and the 10-year Treasury yield is essentially flat. The mixed signals may be a function of lingering worry about the new coronavirus strain.

We may continue to see some mixed signals in trading as we finish out the year as there could be some tension between profit-taking and a fear of missing out given the tailwinds at the back of the market.

Buying The Dip

Yesterday morning, we talked about how there could be a buy-the-dip mentality to help support stocks. That seemed to end up being the case during Monday’s session as U.S. equities ended up staging a pretty impressive recovery.

It was a bit like Mark Twain’s view of the weather in New England. Don’t like it? Wait a few minutes. It ended up being more like a few hours—but still, the week that began with a brutal overseas session amid worries over a new coronavirus strain in the U.K. ended up being a not-too-terrible mixed day.

All of the main three U.S. indices started off deeply in the red as worries about a new COVID-19 strain in the U.K. threw a wet blanket on optimism about a congressional stimulus deal and the emergency authorization of a second vaccine in the U.S.

But as the day went on, it seems that investors came to be less worried about the new strain, perhaps because the evidence doesn’t suggest that it is more lethal—even though it seems to be more contagious—or that it would undermine vaccine efforts.

That’s not to say there was no worry among investors, but it’s just that it might have been relegated to the more common kind that is concerned about lockdowns harming the economy rather than the initial concern that this new strain—which had been previously reported—could be a game-changer for the worse.

The recovery in the main three U.S. indices seemed to indicate that there may have been plenty of optimism as Congress neared an expected passage of a stimulus deal and distribution started for Moderna Inc’s MRNA vaccine on top of the Pfizer Inc. PFE-BioNTech SE BNTX vaccine.

Financials Outperform On Buyback Optimism

Even as COVID-19 worries eased, the market also got some help from the Financials sector, which was by far the best performing of the day after the Federal Reserve said banks will be allowed to do share buybacks in the first quarter, although there will be income limitations.

That’s welcome good news for a sector that has been pretty beaten up over the past year as low-interest rates have sapped its ability to earn money on longer-term loans and provisions to deal with potentially bad loans have sapped profitability.

At the end of the day, it seems that there are still strong tailwinds for the bulls in the form of stimulus and vaccines. The idea is that the stimulus may be able to tide over the economy until the vaccines are widely distributed and can really begin to help consumer spending.

That’s an argument in favor of the Santa Claus rally resuming. But that may have to contend with some year-end-profit taking as we round out the turbulent year that has been 2020.

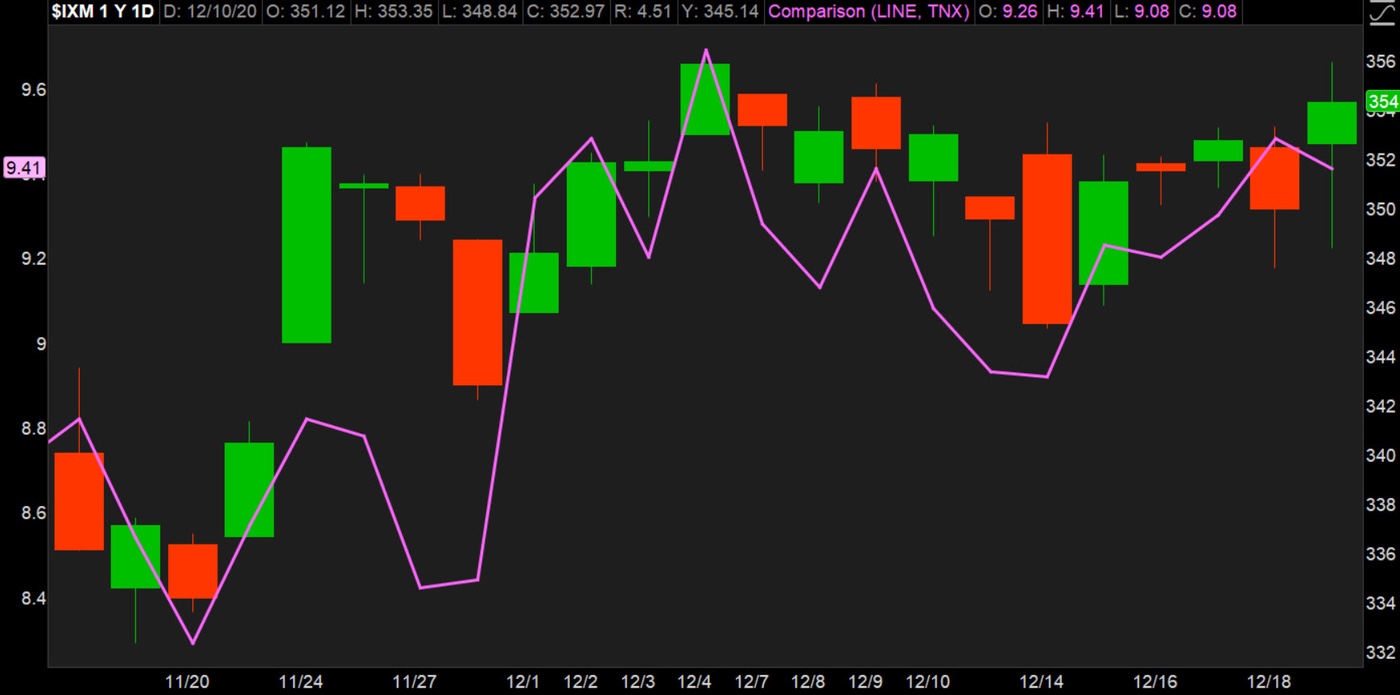

CHART OF THE DAY: A GOOD DAY FOR THE BANKS: The Financials sector ($IXM—candlestick chart) was the best performing of the 11 sectors in the S&P 500 Index (SPX) on Monday. It was interesting to see that happen even as the yield on the 10-year Treasury, as represented here by the 10-Year Treasury Note Yield Index (TNX—purple line), slipped. Often, banks are pressured when longer term yields fall. But on Monday, excitement about the Fed letting banks resume share buybacks, subject to income limitations, in the first quarter was enough to counteract that. Data sources: S&P Dow Jones Indices, Cboe Global Markets. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Investors Tap Brakes on Tesla: After all the hoopla that helped take Tesla Inc TSLA shares to a record high last week ahead of its inclusion in the S&P 500 Index (SPX), some investors may be scratching their heads as to why shares of the electric vehicle maker ended up falling nearly 6.5% in its debut day in the broad benchmark. For one thing, it seems like investors and traders were viewing today as a good day to take some profits after the automaker rose nearly 6% and hit a record high Friday. Even with Monday’s fall, there’s still plenty of potential profits to be taken as the stock was up more than 676% year to date through Monday’s close. It also seems the selling may have been exacerbated by a Reuters report that Apple Inc AAPL is aiming to produce a passenger car that could include its own battery technology.

New Inflation Reading: Tomorrow, investors are scheduled to get the latest reading on the Fed’s preferred inflation gauge, the core personal consumption expenditure price index. A Briefing.com consensus expects the November reading to show a 0.2% month on month gain. Recall that last time the core PCE price index was unchanged on the month, bringing the core index to a 1.4% year-on-year gain. That’s well under the Fed’s target of 2%, and with the third wave of the pandemic ratcheting up in the U.S. during November, it seems unlikely that inflation would have moved radically higher during the month.

Will Vaccine Bring Short Inflation Spike? Speaking of inflation, there is a school of thought that once the vaccines have been widely distributed we might see a temporary inflation spike. The theory is that people would be able to return to pre-COVID levels of shopping even as supply may not bounce back as fast. The welcome surge in consumer spending might be exacerbated if people go on spending binges to make up for being cooped up a lot in 2020. Prices might rise if supplies are tight compared with the surge in demand, as there might be lingering capacity issues as firms try to ramp up (kind of like last spring’s run on toilet paper and hand sanitizer, only instead of Consumer Staples, it might be Consumer Discretionary and other variable-demand items). And remember, the Fed has embarked on a new policy of afterage inflation targeting, meaning it will allow inflation to run hot to make up for times, like now, when it’s been below target.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Martin Katler on Unsplash

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.