In normal times, this afternoon’s earnings schedule would feel like fun and games with Walt Disney Co. DIS, Wynn Resorts, Ltd. WYNN, and Activision Blizzard, Inc. ATVI.

As everyone likely knows, things are far from normal, so there’s a new spin around these earnings and many others to come. Both DIS and WYNN likely saw some of their core businesses hurt badly by COVID-19 in the spring quarter, while ATVI might have benefitted from the same crisis. If you can’t go to a resort or a theme park, maybe you stay home and play video games.

The market’s taking a small breather ahead of the opening bell this morning, but major indices aren’t dramatically lower.

Though we have a big line-up of earnings after the close, it’s gotten to the point where about three-quarters of S&P 500 companies have reported. It looks like most were able to beat the low bar that analysts had set for them. Now the focus could be turning back toward headlines again, and one headline apparently making some nervous this morning is a rise in coronavirus cases globally.

Signs of some possible progress on stimulus talks in Washington could come into play today. It sounds like another round of $1,200 checks could be on the way, but other aspects of a possible deal are unclear. It’s really important from a market status that we get some sort of stimulus package.

Meanwhile, a little of the early softness could reflect more barking between China and the U.S., analysts said. This time it’s over the proposed Microsoft Corporation MSFT purchase of the TikTok app. Investors are getting pretty used to the two countries exchanging verbal barbs, however, and it’s probably not going to be a huge influence today.

Data’s pretty light today, with June factory orders the only one of real significance on the schedule. Analysts expect a 5.2% rise, according to research firm Briefing.com. That would be sequentially down from May’s 8% gain.

New Month, Same Tech Strength

So far the new month doesn’t feel much different from the old one, even if it’s just one session.

Tech stocks, which took a breather in mid-July for a couple of weeks, led the way again Monday as Apple Inc AAPL and MSFT surged. MSFT had wilted a little following earnings, but now seems to be finding the way with a hand from its FAANG cousins.

Seeing Techs start the week strong was kind of a dog bites man story. On the other hand, something that might be more significant was the S&P 500 Index’s (SPX) finish above 3290 yesterday. That’s the highest close it’s been able to muster since late February, and comes after it hit its head last week testing and failing to exceed the July high near 3280.

Though the less than 1% gain Monday for the SPX doesn’t look too huge, it’s sometimes a positive momentum indicator when an index or stock can take out a level that had posed some earlier trouble.

The last SPX close above 3300, which now looks like it might be a psychological resistance point, occurred on Feb. 20. That’s not far below the all-time closing high of 3386 posted a little earlier that month, all before this nearly six-month health and economic crisis.

Some of the positive feelings early this week came from headlines that show virus cases beginning to level off in some of the “hot zones” where they’d been rising so quickly through July. That said, the government has been warning about case growth in parts of the Midwest and rural South, and cases overseas have also been on the upswing. For instance, parts of Australia are now being hit hard. So it’s important for investors to consider the overall picture and not get too optimistic based on one or two days of news reports.

Aside from coronavirus, everyone seems to be focused on the struggles in Washington to agree on a new stimulus package. Some people might be wondering how stocks delivered such a nice rally Monday even as talks there dragged on.

It could be a case of investors feeling like they’ve seen this movie before. Though you never want to predict or get too confident, many investors appear to feel fairly certain that Washington will get something done. The market is basically rolling its eyes at all the competing headlines about a deadlock and thinking, “They’ll figure something out.”

Maybe that’s not going to be right, but it’s the impression now on Wall Street. If the impression starts to change, then it might be a bad day for the market.

Caution seemed to flag a little Monday, with bonds falling and gold still strong but under $2,000 an ounce. Still, bond yields aren’t much above the 2020 lows, and the dollar continues to look weak vs. where it was earlier this year.

The Cboe Volatility Index (VIX) finished Monday below 25, an important level lately. Finishes below 25 could signal less investor fear, but be on the watch for any swing back toward 30, especially if the stimulus talks start to really look pessimistic.

Two Earnings To Watch this Week After DIS

More than 20% of the S&P 500 is scheduled to report this week, so it’s easy to feel like you’re drowning in news. That’s why it can be important to focus on a few that arguably could tell us most about the underlying economy.

Last week was huge from an earnings standpoint as the FAANGs delivered big-time. Those earnings, however, didn’t really tell people much they didn’t already know, because most analysts were pretty sure the stay-at-home economy helped Tech.

Starting this week we can hear more from companies focused on the “real” economy, especially Consumer Discretionary and Industrials. Their guidance will be interesting to watch the rest of the season, and hearing their outlooks is going to be important. Retail earnings are later this month and could be particularly telling.

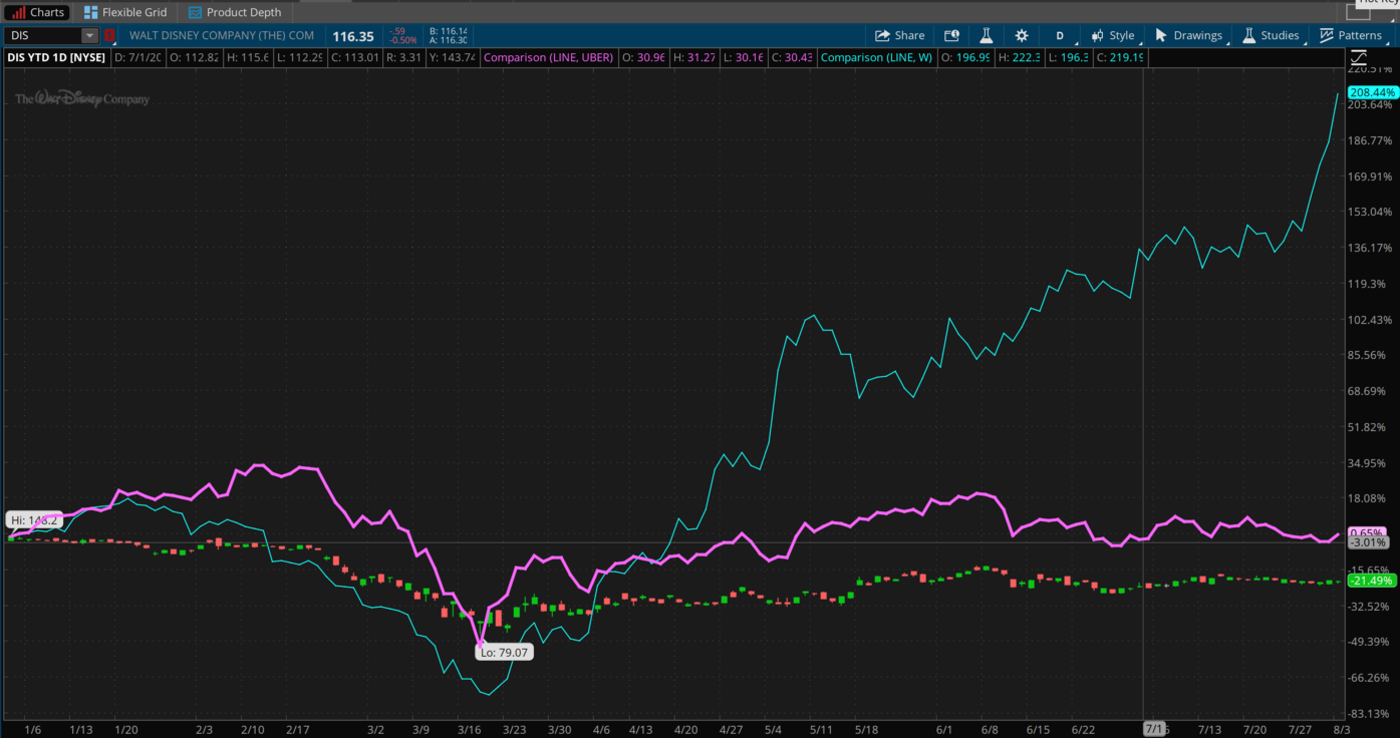

Before that, we’ll hear from Uber Technologies UBER and Wayfair Inc W, two stocks that really reflect the consumer economy. With UBER, the question is whether their delivery services, including groceries, were able to offset the expected weakness in passenger rides. With Wayfair, we’ll see if people stuck at home decided to do some renovation or upgrade their furniture.

W is expected to report tomorrow morning, while UBER is expected to put out its earnings after the close Thursday (see chart below).

First, however, there’s this afternoon’s earnings from DIS, another consumer-oriented business. In some ways, DIS might have benefitted from the lockdown, especially its streaming services. However, theme parks, resorts, and movies have probably suffered a lot, and the stock hasn’t come back to test its early 2020 highs.

That’s the case with a lot of travel and consumer company stocks, which is easy to forget when you see the Nasdaq (COMP) trading well above where it was at the start of the year, bolstered by big-Tech.

The DIS call could be pretty interesting as investors hear more detail about the pandemic’s effect, but it wouldn’t be too surprising if executives remain uncertain about how the rest of the year might go. The pandemic is just so unpredictable, and no one knows when or if a vaccine or significant treatment will hit the market.

With DIS and other consumer-oriented companies reporting now (along with retailers later this month), it might be a good idea to keep pricing in mind. It’s not just about moving units, it’s about the price those units fetch. Will companies have to discount? If retail firms don’t see enough demand occurring, they often have to cut prices.

If that happens, it could generally speak to a consumer who’s a little cautious and not willing to pay up for clothing and other items. People who don’t want to pay up for clothing because they’re worried about or have lost their jobs are even less likely to want to pay more for (or even buy) major items like cars and washing machines. Those products are what really drive the consumer economy—which makes up more than two-thirds of the total U.S. economy.

CHART OF THE DAY: A SUMMER’S TALE: This year-to-date chart of Disney (DIS—candlestick), Uber (UBER—purple line) and Wayfair (W—blue line) arguably shows where investors’ minds are regarding the pandemic as these three prepare to report. They apparently think DIS and UBER are suffering while W is getting support from people stuck at home upgrading their living space. Data Sources: New York Stock Exchange, Nasdaq. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

From the Factory Floor: If the recent resurgence in coronavirus both in the U.S. and overseas is hurting factories, it hasn’t shown up in the data yet. A European survey Monday showed manufacturing activity across the euro zone expanded last month for the first time since early 2019. There was also positive manufacturing data from Asia.

Here at home, yesterday also brought some positive news from the factory floor as the closely-watched ISM Manufacturing Index for July rose to 54.2%, up from 52.6% in June. Anything over 50 is considered expansion. It’s true, of course, that July was kind of a Jekyll and Hyde month, helped by reopenings early on before the virus roared back by mid-month and caused some new closings. Still, we have to go with the data we get, and this report looked good.

New orders and production from the ISM remained pretty robust in July, the ISM said, but research firm Briefing.com warned investors not to get too excited by the July data because so much demand uncertainty lies ahead.

However, for the moment the better manufacturing data seems to be supporting crude oil, which had edged down to near $40 a barrel earlier Monday but ended the day near $41.

The Gold-Tech Alliance: Wondering about the market’s recent behavior? Let’s probe a little further. First, gold continues to be a beast, trading near a record high $2,000 an ounce. The dollar index, meanwhile, is getting clobbered. This may seem like a commodities and currencies situation from a high level, but it’s also connected to the Tech rally in stocks.

Here’s a possible reason why: Right now, real yields (calculated by subtracting inflation from the nominal Treasury yield) are negative, so some investors appear to be retreating from U.S. assets and into foreign currencies and bonds, as well as gold. This in turn can put more pressure on the dollar. That’s the first part of the equation.

However, the negative yields could also possibly be helping stocks as people look for places to put their money that deliver some return and even possibly safety, though stocks are never considered a truly “safe” investment. Those seeking perceived safety seem to be turning to gold. Those willing to take more risk appear to be putting money into high-flying Tech names in the COMP. However, there may be a “safety” play at work here, too.

One thing about these big Tech names that seems compelling to many investors is the amount of cash they hold on their balance sheets. It might seem counterintuitive considering these are growth-oriented stocks, but when the risk meter turns upward, sometimes it’s the overleveraged that become the overexposed. A strong balance sheet can be an antidote of sorts.

Could Beaten-Down Sectors Be Due for a Comeback? The major rally in some of the FAANGs since earnings last week could potentially set up a profit-taking situation. Nothing’s guaranteed, naturally, but it’s not unusual to see investors rotating in and out of stocks after they make a run. They often take profits and find something that’s a little more beat-up and rotate into that.

So what’s “beaten up” right now? Energy and Financials often come to mind. They’re the two worst-performing SPX sectors over the last month. More recently, Materials has played a little defense, which actually seems a bit weird when you consider it includes many of the mining stocks that would seem to be on track to benefit from recent rallies in gold and silver.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Travis Gergen on Unsplash

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.