The following post was written and/or published as a collaboration between Benzinga’s in-house sponsored content team and a financial partner of Benzinga.

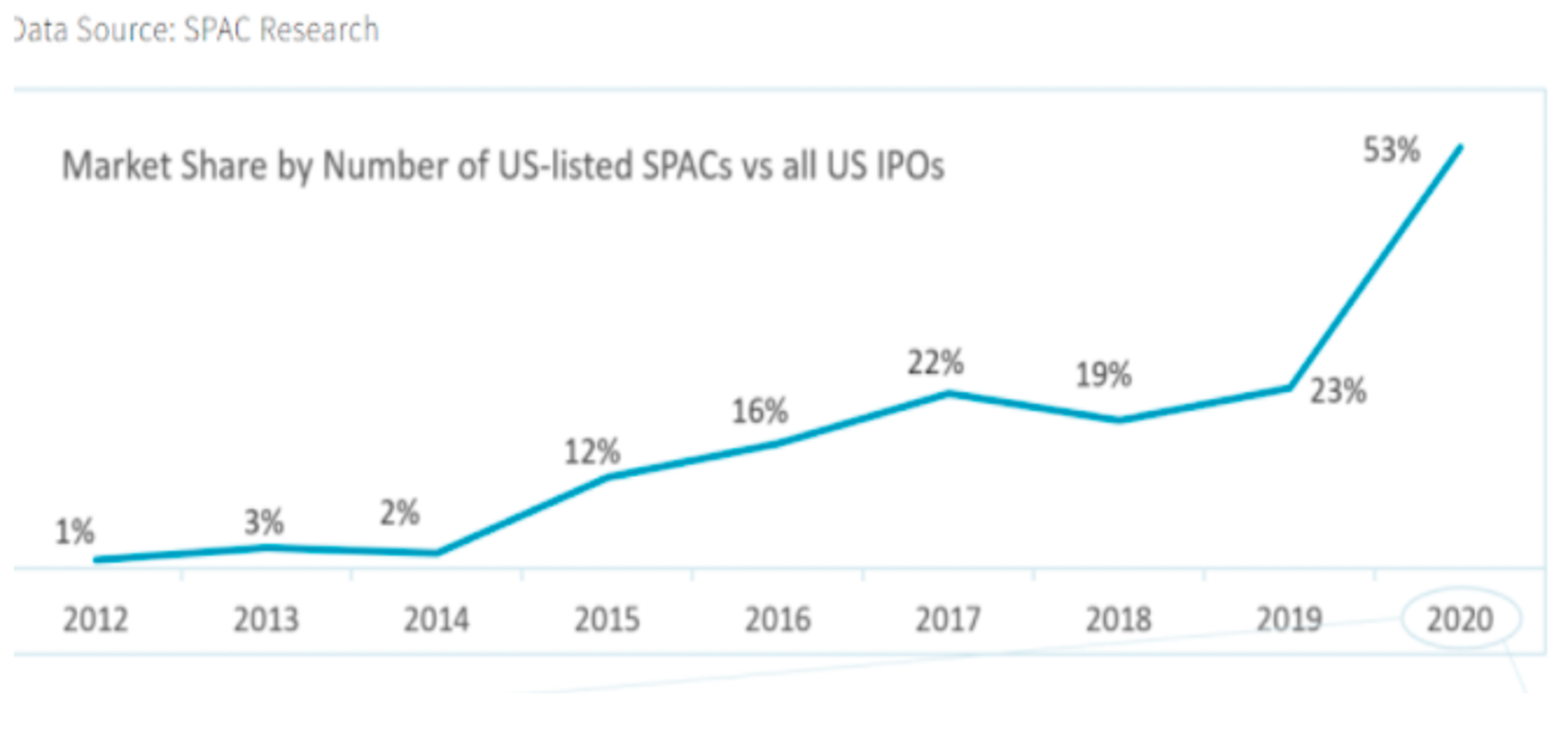

Special Purpose Acquisition Companies (SPACs) have leaped to prominence over the last eighteen months. The average size of a SPAC in 2020 was $335 million, nearly 10 times the amount in 2009. If in 2019 they raised $13.5 billion from 59 deals, 2020 saw $83 billion from 237 deals and latest reports indicate $38.3 billion from 130 SPACs in only the first two months of 2021. SPACs are even overtaking the traditional IPO route as the means to bring ambitious businesses to public status. So far this year, SPACs have taken in just less than double the amount raised by IPOs.

But before we jump on the bandwagon, let’s understand what a SPAC is and why they are fast becoming a preferred method of venture capital for a wide range of sponsors, from institutions like Goldman Sachs Group Inc GS and JP Morgan Chase & Co. JPM to seasoned deal-makers Bill Ackman and Michael Klein, to celebrities like Serena Williams or Shaquille O'Neal. We’ll also look at why a SPAC ETF could be a sensible way for retail investors to gain exposure to this growing phenomenon.

Sponsors form a SPAC, a public company, with no operations of its own other than the promise to identify and merge with a target company within two years. Retail investors can buy individual shares in the SPAC for $10 each, with the potential to benefit from a rise in their value prior to or following a merger. Their shares in the SPAC will also transform into shares in the target company post-merger, with the associated potential of improved performance and enhanced valuation. SPACs were once considered suspect for the disproportionate benefits they bring sponsors and the risk to investors. However, as the credibility and liquidity of sponsors have risen, the market increasingly recognizes that the transparency and democratic access to M&A deals that SPACs offer can actually be a better indicator of long-term, big idea opportunities than the closed backroom deals that dominate the old-school IPO process.

As of end of December 2020

source: https://spacanalytics.com/

SPAC highlights include Chamath Palihapitiya’s SPAC, Social Capital Hedosophia Hldgs Corp IPOF, which raised over $650 million to merge with space tourism entrepreneur, Virgin Galactic Holdings Inc SPCE. Also Diamond Eagle’s $400 million blank check for DraftKings Inc DKNG, a digital sports entertainment and gaming company that blurs the line between sports betting, fantasy gaming, and esports. Recent developments indicate a potential deal between Michael Klein’s $1.8 billion SPAC, Churchill Capital IV, and luxury electric vehicle manufacturer, Lucid Motors. These deals bring potentially fruitful returns to the SPAC shareholders and offer the target companies a smoother, quicker, profile-boosting route to public status.

Macroeconomic conditions supporting the SPAC market seem likely to persist. Federal Government Covid-insulation policies, combined with very low-interest rates have created a cash-rich market, with investors searching for returns. In that context, smaller companies needing capital to weather the pandemic, or larger ones looking to expand or capitalize on the trend, could constitute attractive targets to the new SPACs being formed — one every 5 days this year! Combined with the internal developments within the sector that have seen changes in costs and SPAC structure to offer investors more flexibility, control, and potential returns, the momentum persists.

SPACs are disrupting traditional enterprise models and offering individual investors much earlier access to the M&A process. But despite the expansion, it is still hard to predict the winners and it is not always possible to know which are the best SPACs to buy. SPACs have opened up the PIPE (Private Investment in Private Equity) space to retail investors, but the savvy shareholder would do well to consider a diversified exposure to the SPAC space.

This is where Defiance ETFs SPAC ETF SPAK can offer targeted access to the SPAC boom, without overexposure to any one particular company or deal. SPAK tracks a rules-based, weighted index of the most innovative, liquid companies in the SPAC universe. It allocates 40% to the pre-deal blank check companies and 60% to the initial public offerings (“IPOs”) derived from the SPACs, giving investors access to the whole life cycle of a SPAC. No individual SPAC can make up more than 12% of the index, and not more than 45% of the index is constituted by securities that each comprise over 5%.

SPAK holds securities for two years post-merger to bring investors the full benefit of the SPAC mechanism. The fund is passively managed and is reviewed monthly to ensure that the ETF captures the potential dynamism of the SPAC space. SPAK seeks to harness the disruption, innovation, and democracy that SPACs bring to the M&A space while mitigating the risks involved in any single deal. Next-generation investors should consider the advantages of the balanced exposure that SPAK provides to the invigorated SPAC market.

The Funds’ investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company. Please read it carefully before investing. A hard copy of the prospectus can be requested by calling 833.333.9383.

Investing involves risk. Principal loss is possible. The Fund invests in companies that have recently completed an IPO or are derived from a SPAC. These companies may be unseasoned and lack a trading history, a track record of reporting to investors, and widely available research coverage. IPOs are thus often subject to extreme price volatility and speculative trading. These stocks may have above-average price appreciation in connection with the IPO prior to inclusion in the Index. The price of stocks included in the Index may not continue to appreciate and the performance of these stocks may not replicate the performance exhibited in the past. In addition, IPOs may share similar illiquidity risks of private equity and venture capital. The free float shares held by the public in an IPO are typically a small percentage of the market capitalization. The ownership of many IPOs often includes large holdings by venture capital and private equity investors who seek to sell their shares in the public market in the months following an IPO when shares restricted by lock-up are released, causing greater volatility and possible downward pressure during the time that locked-up shares are released. The Fund is considered to be non-diversified, which means that it may invest more of its assets in the securities of a single issuer or a smaller number of issuers than if it were a diversified fund. As a result, the Fund may be more exposed to the risks associated with and developments affecting an individual issuer or a smaller number of issuers than a fund that invests more widely. This may increase the Fund’s volatility and cause the performance of a relatively smaller number of issuers to have a greater impact on the Fund’s performance.

The Fund is new with a limited operating history.

SPAK is distributed by Foreside Fund Services, LLC.

Photo by Jason Briscoe on Unsplash

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.