Stay the course.

After three rate cuts in a row, the Fed decided to leave things alone Wednesday and take a little time to see how things play out heading into the new year. That doesn’t necessarily mean this rate cutting cycle is necessarily over, however, because the futures market still indicates decent chances of one more cut in the first half of 2020.

The Fed’s decision to keep its benchmark Fed funds rate at a steady 1.5% to 1.75% likely didn’t come as a big surprise to anyone following the market lately. Futures prices had odds of a policy change at around 2% going into this week’s meeting.

While chances of another cut in 2020 remain out there, the Fed kind of squelched that a little in its statement Wednesday, saying economic conditions show current rates at appropriate levels and likely to remain that way for a while.

What's Changed, (And What's Not Changed) Since Last Meeting

“The Committee judges that the current stance of monetary policy is appropriate to support sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective,” the statement said.

When the Fed talks about “sustained expansion” at current rate levels, that might be an indication it doesn’t feel much need to change anytime soon. However, the statement added that the Fed continues to watch labor market conditions, international developments, and inflation.

Also, the decision to keep rates unchanged was unanimous this time after a couple of meetings where there were dissenters both on the hawkish and dovish sides. Now it looks like hawks and doves are flocking together with rates at current levels. Maybe three cuts, totaling 75 basis points, were enough to make FOMC members feel like they’re at a comfortable place.

Last time out, the Fed cited “the implications of global developments” as one reason to lower rates. This time, it still included that language, but only to say it continues to monitor the situation. That could sound to some like maybe the Fed’s a little less worried about slow overseas growth weighing on the U.S. economy.

The Fed’s statement didn’t include any changes from last time regarding U.S. conditions, still citing economic activity “rising at a moderate rate,” along with a “strong pace” of household spending, but noting that business fixed investment and exports “remain weak.”

The Fed also continued to highlight a strong U.S. labor market marked by low unemployment and solid job gains. “We expect the job market to remain strong,” said Fed Chairman Jerome Powell, speaking in the post-meeting press conference. He noted that the Fed’s projections show unemployment remaining below 4% for the next few years. That would be unprecedented if it happened.

He said Fed members strongly believe inflation will hit the Fed’s 2% target in 2021, but noted that inflation pressures have been “unexpectedly muted,” which allowed the Fed to lower rates this year and help stimulate the economy. Adjusting to economic changes, he added, is one of the Fed’s responsibilities as it tries to maintain maximum employment and price stability.

The Fed continues to purchase Treasury bills to “maintain an ample level of reserves,” Powell said. Operations have gone well so far, with pressures in the money market “subdued,” he added. The Fed is ready to adjust that policy as appropriate to keep the Fed funds rate in the target range

Follow The Bouncing Dots

Looking ahead, the Fed’s economic projections for 2020 don’t look all that different from where they were in its last quarterly forecast back in September. It still forecasts gross domestic product to rise 2% next year and inflation to grow 1.9% year-over-year in 2020. It reduced its unemployment rate projection to 3.5%, from 3.7%, for next year.

The updated “dot plot” from Federal Open Market Committee (FOMC) members, maps out where each of them sees rates going in the years ahead. For 2020, every member projects rates to stay below 2%. About half expect rates to top that level in 2021, with chances that they could rise to around 2.5% by mid-2022. This seems to indicate the Fed thinks the economy will remain relatively stable, with slow but steady growth the next few years.

The stock market didn’t have a big reaction to the Fed’s announcement, and that’s not really going to come as a shock. Investors basically got just what they expected. The 10-year Treasury note yield still traded near where it had been all morning, around 1.8%. Gold gained slightly, but crude oil remained down.

Looking out toward the next Fed meeting at the end of January, investors price in about a 91% chance of rates staying in place, according to CME Group futures. Chances of a rate cut rise to around 14% at the March meeting, and to 35% by June. Some analysts have said if the Fed does make another rate move in 2020, it’s likely to come sooner rather than later so the Fed won’t be accused of having influence on the November presidential election.

That isn’t always the case, however. The Fed lowered rates as late as August in the 1992 election year, and raised rates in June, August, and September of 2004 before that year’s election. More recently, it chopped rates sharply ahead of the 2008 election as the economy entered a deep recession.

Taking A Stand

Today’s decision comes after the Fed lowered rates at its previous three meetings. We’ve seen a major reversal from this time a year ago, when the Fed last delivered a rate hike and had the market fretting about a possible rate-related economic slowdown.

The economy has slowed since then, but expectations are starting to look a little rosier as the more accommodating rate environment boomerangs around the economy. This is a process that can take a while, which is why some of the latest data might just now be starting to reflect this year's cuts, which totaled 75 basis points in all.

Current events like strong holiday sales, last week’s amazing jobs report, and great housing numbers—which investors saw confirmed by home builder Toll Brothers Inc TOL earnings report earlier this week—are all potential signs of the lower rates working their way through into business and consumer wallets.

While the Fed always has to walk a tightrope between possibly easing too much and helping create an inflationary environment and tightening too much and strangling a growing economy (something some analysts think it came close to last year), it’s arguably in a sweeter spot now. Inflation remains benign (see more below), and the economy is starting to show some signs that it might be ready to pop back from relatively low growth readings the last few quarters.

Closely Watched GDP Estimate Up Sharply

For instance, the Atlanta Fed’s GDP Now indicator, which not so long ago projected very slim growth below 0.5% in Q4, has now climbed to 2%. The jobs report and wholesale trade numbers played into the sharp hike in the metric, one of the quickest bounces in GDP Now seen in awhile.

However, 2% growth isn’t necessarily the kind of muscle many investors had hoped for. It’s down from readings that hit 3% last year, and may be getting smacked around by the trade war with China.

If a Phase One deal is reached and some of the tariffs either don’t go into effect or get rolled back, it might be interesting to see if growth picks up. A more solid economic growth profile accompanied by low inflation and continued strong jobs gains would likely make a nice stocking stuffer for any stock market bulls in your family. It would certainly make the Fed’s wish list for 2020.

This morning’s Consumer Price Index (CPI) data for November didn’t appear to bring inflation back to the front pages, with just a 0.2% core price increase. Core CPI year-over-year is 2.3%, which is a little above the Fed’s 2% target. That said, the Fed is thought to keep a closer eye on the core Personal Consumption Expenditures (PCE) price index for its inflation readings, and that remained well below the target, coming in at 1.6% year-over-year for October.

The November PCE data are scheduled for a week from Friday, so that might be something to keep an eye on for any possible impact on the Fed’s future thinking around inflation. Tomorrow’s producer price index (PPI) is also on the horizon (see more below). For now, inflation fears seem distant.

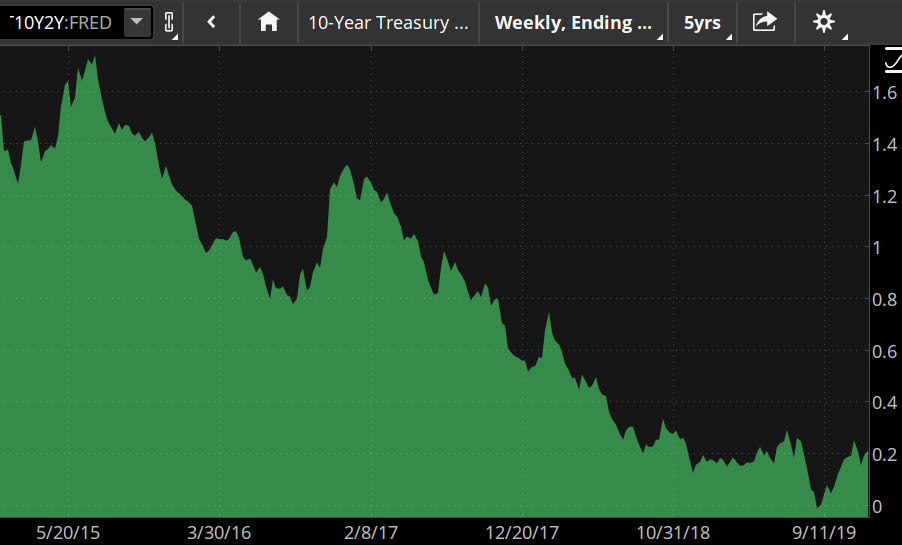

CHART OF THE AFTERNOON: EYE ON THE CURVE. Over the past five years, the trend in the spread between 10-year Treasuries and 2-year Treasuries has been toward narrowing. And it wasn't too long ago—a little over three months ago—that if flipped negative for a brief period. In recent days, it's pushed past 20 basis points a couple times, but seems to have stalled. With the Fed on a rate pause and inflation apparently muted, perhaps the 2-10 spread has found its comfort zone. Data source: Federal Reserve's FRED database. Image source: The thinkorswim platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results. FRED is a registered trademark of the Federal Reserve Bank of St. Louis. The Federal Reserve Bank of St. Louis does not sponsor or endorse and is not affiliated with TD Ameritrade.

Bund (Not Bond) Watch: It’s been nearly five months since the 10-year Treasury yield last had a “2” as the starting number, back in late July. The yield has been pivoting around 1.8% for a while now. One factor potentially pushing against any quick test of 2% is the fact that German bund yields remain at nearly negative 0.3%.

That’s a big gain from where they were late last summer, but still low enough to probably make U.S. bonds appear attractive to many overseas investors, keeping yields under pressure. We’ll see if this week’s ECB meeting sheds any light on the economy there, but no interest rate policy change is expected, analysts say.

German yields fell below zero more than six months ago. Back in 2018, however, they stayed above zero the entire year and U.S. yields marched to 3% and above. Correlation isn’t causation, but it’s hard to argue there wasn’t a connection there. Some analysts think Europe and Japan (along with China) can enjoy improved economic growth in 2020.

If that happens, maybe then we’ll see a real move higher in U.S. yields as overseas investors put money back into their own economies. Still, many analysts forecast a ceiling of around 2.25% in the 10-year yield for 2020. We’ll have to wait and watch.

Brexit Back in the Mix as Election Looms: One thing that might be a concern for Powell and for investors is the possibility that Brexit could come back into the news right after the new year. British voters elect a new parliament tomorrow, which media reports say could help determine whether and how the U.K. exits from the European Union. Polls show the Conservatives leading. If that party wins enough seats, it could support a plan by its leaders to leave the EU by Jan. 31. If it loses, the country might face another referendum on the issue later next year.

Between the parliamentary election and this week’s European Central Bank meeting, investors might want to keep a sharper eye than normal on the pound and the euro. The pound has climbed vs. the dollar over the last three months and was up again on Wednesday, but the euro’s been kind of flat and fell vs. the dollar Wednesday.

Inflation and the CEO: Wednesday’s consumer inflation reading looked pretty benign, and analysts expect more of the same early Thursday from the November Producer Price Index (PPI). The average projection, according to Briefing.com, is for core and headline PPI to rise 0.2% from the previous month, down from 0.3% and 0.4%, respectively, in October.

PPI can often reflect what businesses see on the ground, so to speak, and whether their costs are rising. This can be important to track because rising costs often get passed along to consumers. Or, if not, they can cut into profit margins, hurting earnings. Year-over-year PPI fell in October after a few readings earlier this year that looked a little hot.

The potential downside of a low PPI, however, is that it could reflect softer business spending. The latest Business Roundtable quarterly economic outlook survey tracking CEO plans for capital spending and hiring and expectations for sales over the next six months slipped slightly. “CEOs remain cautious in the face of uncertainty over trade policy and an associated slowdown in global growth and the U.S. manufacturing sector, which is currently contracting,” the Business Roundtable said in a news release.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

Image by Gerd Altmann from Pixabay

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.