At the end of the first quarter of 2018, we spoke with GreenWave Advisors’ Matt Karnes, who said California cannabis sales could hit $2.5 billion in 2018, mostly in line with estimates out of BDS Analytics and Arcview Market Research.

Now that a year has passed since recreational marijuana sales commenced in the largest legal marijuana market in the world, we’ve decided to look back at the figures and how they compare with the estimates.

The Figures

Total 2018 recreational sales in California were about $1.2 billion, according to the state, which recently reported its fourth-quarter recreational cannabis sales tax collections.

Implied revenues for recreational cannabis sales were down 5 percent sequentially, to $339 million.

Medical marijuana sales were excluded from these numbers, as they are not subject to sales tax.

Assuming that roughly 40 percent of total sales are medical — based upon GreenWave Advisors’ channel checks — total California marijuana revenue was approximately $2 billion in 2018.

The Cannabis Capital Conference is coming back to Toronto April 17-18!

“As the state works through its ‘growing pains’ with respect to licensing procedures and as final regulations are implemented, we expect an acceleration in revenue growth for 2019 and beyond to reach its full potential of $6.5 billion by 2022,” Karnes told Benzinga.

“This estimate is lower than our original forecast of $2.5 billion,” Karnes said, addding that the illicit market continues to thrive, putting pressure on legal cannabis sales and prices.

The Golden State had about 650 licensed retail locations in the fourth quarter, a notable improvement from approximately 450 in the third quarter. The overall market remains underpenetrated, Karnes said.

To put the numbers in perspective: Colorado had approximately 540 retail licenses with a population of 5.6 million.

Rufus Casey, CEO of the third-party seed-to-sale tracking and compliance software company GrowFlow, said that while the California recreational cannabis program has officially started, “we are not seeing the implications of it from a revenue standpoint."

Highly regulated recreational cannabis tracking and compliance is still in a phase of licensee education, Casey said.

"With the implementation of the state Track-and-Trace program, we are confident that the state will be successful in preventing diversion and collecting the taxes that they had hoped to see this year.”

A Detailed Look

Another company that shared its data exclusively with Benzinga is Jane Technologies, an online marketplace operator.

After computing data for the state and for three individual regions — Northern California, Southern California – Los Angeles and Southern California — the company came up with the relative volume of online sales for various cannabis products, the frequency at which customers purchased and how much they spent.

While many factors contributed to regional differences, from local regulations to the availability of products on the black market, the transactions on the e-commerce platform reveal some notable trends.

A few findings:

- Southern Californians were bigger cannabis consumers this year than their northern counterparts: they purchased products more frequently and, in each transaction, bought more products and spent more money.

- Flowers were the bestselling cannabis category across the state, making up for 44 percent of all sales this year. Edibles, however, were notably more popular in Southern California, where they made up for 19 percent of all sales (in the San Diego region) compared to just 9 percent in Northern California.

- Among lineages, hybrids took the top spot across the state, accounting for the majority of sales (54 percent).

The tables below summarize the year for Jane's California business:

|

|

NorCal |

SoCal - LA |

SoCal - San Diego |

CA Total |

|

Flower |

47% |

40% |

35% |

44% |

|

Cartridges |

23% |

17% |

21% |

23% |

|

Extracts |

14% |

18% |

10% |

13% |

|

Edibles |

9% |

13% |

19% |

11% |

|

PreRolls |

5% |

6% |

7% |

5% |

|

Tinctures |

1% |

4% |

6% |

2% |

|

Topicals |

1% |

2% |

2% |

1% |

Jane California's 2018 online sales, cannabis lineages:

|

|

NorCal |

SoCal - LA |

SoCal - San Diego |

CA Total |

|

Hybrid |

54% |

55% |

50% |

54% |

|

Indica |

21% |

18% |

18% |

20% |

|

Sativa |

19% |

15% |

19% |

19% |

|

CBD |

5% |

11% |

14% |

7% |

Jane California 2018 online sales, frequency and size of purchases:

|

|

NorCal |

SoCal - LA |

SoCal - San Diego |

CA Total |

|

Days Btwn Purchases |

10 |

5 |

6 |

9 |

|

Average Basket Size |

$85 |

$113 |

$133 |

$92 |

|

Prods per Cart |

2.28 |

2.93 |

2.99 |

2.40 |

How Do Regulations And Taxes Come Into Play?

A commonly cited argument in favor of legalization is the tax revenue opportunity from the legal cannabis market. Given the popularity of legalization and the high demand for cannabis, sales of legal weed could result in a significant inflow to the state’s coffers.

In California, the state collected $82.3 million in sales taxes, $127.9 million in excise taxes and $18.1 million in cultivation taxes in 2018. Starting this year, the state will collect two additional taxes: a 15-percent excise tax on the purchase of cannabis and cannabis products and a cultivation tax on all harvested cannabis that goes into the commercial market.

In addition, cannabis businesses in the state face all sorts of fees that the state as well as local governments can levy.

“It's a very, very complex regulatory environment in California,” Beau Whitney, senior economist at New Frontier Data, told Benzinga.

An Inversely Proportional Relationship

Demand for cannabis was strong in California last year, but wholesale prices fell.

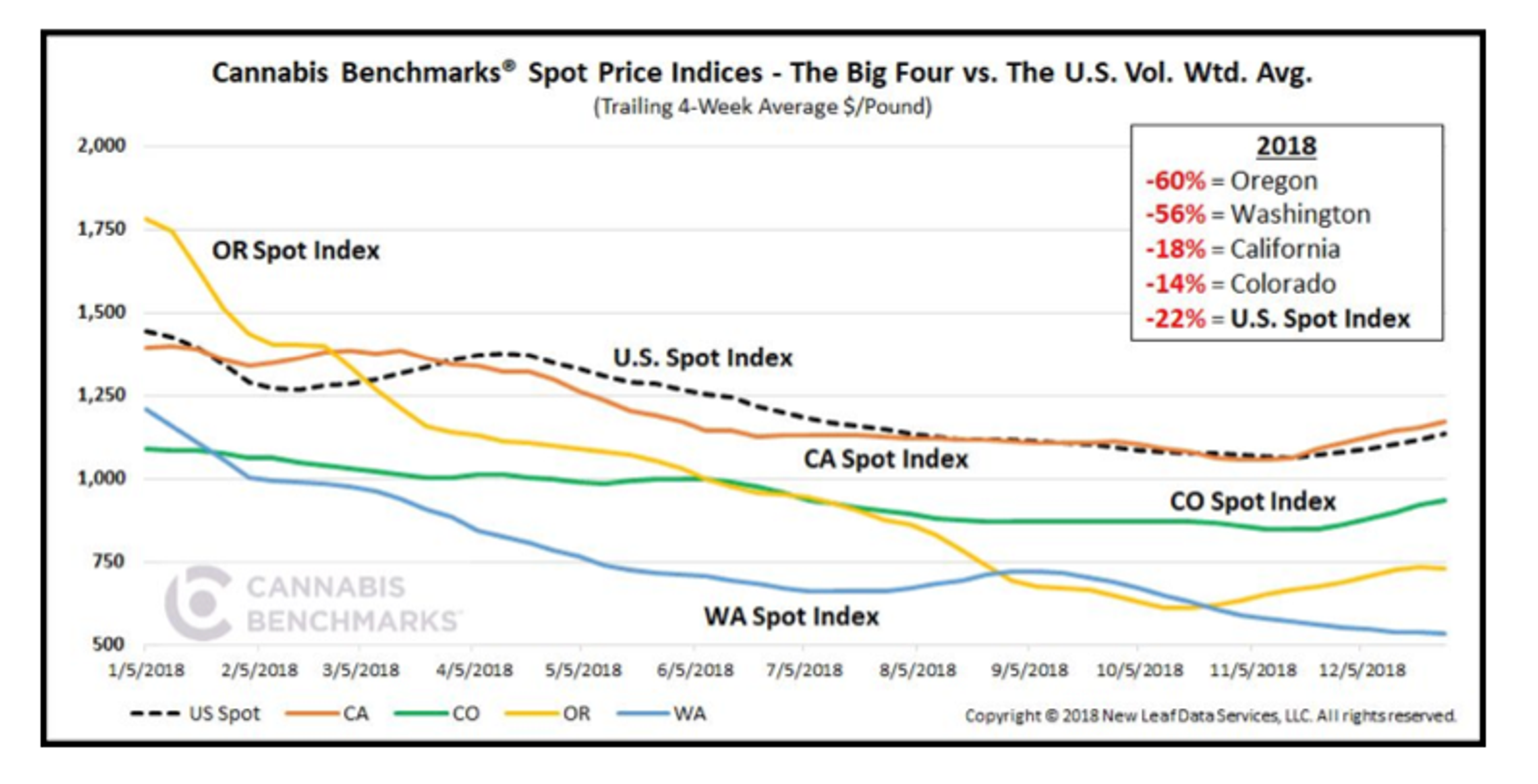

The wholesale price for cannabis in California opened 2018 at $1,455 per pound and closed at $1,196 per pound, averaging $1,197 per pound for the year, according to Cannabis Benchmarks.

The chart below shows the trailing four-week averages of the U.S. Spot Index, as well as those for the “Big Four” markets of California, Colorado, Oregon and Washington.

“Overall, wholesale pricing trended downward to varying degrees this year. Apart from upward momentum in the second halves of the first and fourth quarters, the trailing four-week average of the U.S. Spot slid downward consistently in 2018," Cannabis Benchmarks CEO Jonathan Rubin told Benzinga.

“Despite similar seasonal growing patterns in the West Coast states, the behavior of supply side rates was unique in each of those markets. Expanding and increasingly competitive markets on the West Coast, along with good outdoor growing conditions in 2018, provided ample opportunity for wholesale price erosion," Rubin said.

California's composite spot price stayed higher than Oregon and Washington and underwent less price erosion as the state rolled out its licensed, compliant recreational market, the CEO said.

Benzinga Cannabis writer Alex Oleinic contributed to this report.

Photo by Javier Hasse.

Related Links:

Why Banning 'Marijuana' From The Cannabis Industry Doesn't Work

California Cannabis Laws In 2018-2019: What You Need To Know

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.