The following was originally published by Brad Thomas on iREIT Investor.

Last week, Care Capital Properties Inc CCP listed shares on the New York Stock Exchange. The “pure play” assisted living REIT commenced operations by spinning off from Ventas, Inc. VTR and issuing around 84 million shares and OP units.

After a full week of trading, shares climbed by 1.56 percent, even after the meltdown on Friday.

CCP’s portfolio consists of 355 properties, predominantly skilled nursing (90 percent), senior housing (5 percent), specialty hospitals (4 percent), and loans (1 percent). The closest competitor is Omega Healthcare Investors OHI, with 560 properties (525 being skilled nursing). No other REIT has such exposure in skilled nursing. See my article on CCP HERE.

Including CCP there are now 17 healthcare REITs and I have researched most of them (excluding CHCT, a micro-cap REIT that is on my radar list now). Here’s a snapshot of all of the names (based on market capitalization):

Later this week I will be providing premium iREIT Investor subscribers with my “bracketology” rankings and specifically I will be focusing on the healthcare REIT sector. The goal for the bracketology research is to evaluate the durability attributes for each REIT and provide a scoring system based on critical strength-related metrics. I weight each REIT based on a number of key metrics and then conclude the research with a completed ranking report for each company.

While researching the growing list of healthcare REITs I have become more sensitive to the “pure play” REITs that own and operate assets within their “circle of competence”. As you know, I own several of these so-called “pure play” REITs as well as 2-out-of-3 of the diversified healthcare REITs.

The recently announced CCP spinoff from VTR got me thinking…

Should I focus on the “pure play” REITs that offer a cleaner story or should I simply focus on the diversified REITs that have demonstrated decades of solid performance? Simply put, should I look to build my own basket of “pure play” REITs or just leave it up to Debra Cafaro (CEO of VTR) or Lauralee Martin (CEO of HCP)?

How Many Eggs In The Basket?

First off, it’s important to discuss the importance for diversification. I can’t overestimate the importance of owning more than one REIT. Many of you know that one of my favorite REITs is Realty Income Corp O and this security represents around 7 percent of my Durable Income Portfolio. While Realty Income is well-diversified, with over 4,000 individual properties, I must not put all of my eggs in one basket.

The same goes for VTR, another blue chip REIT that I have over-weighted. The diversification appeal for VTR is similar to my attraction for Realty Income – VTR owns 1,600 properties (prior to the CCP spin-off) with a highly predictable earnings history.

As I contemplate the notion of building a “pure play” healthcare REIT basket I believe it’s critical to examine the operational acumen for each REIT. For example, within the assisted living sector there are two names to own: Omega Healthcare Investors Inc OHI and Care Capital Properties.

It’s important to remember that the assisted living sector is arguably the riskiest sub-sector in the healthcare space because of its reliance on government reimbursement. The more recent issues at HCP, Inc. and its primary tenant, HCR ManorCare, has validated the fear that unusually high tenant concentration within the skilled nursing sector is risky.

HCP has around 25 percent exposure with HCR ManorCare and around 21 percent exposure in Brookdale – again, that mean risks are elevated. Conversely, Ventas has de-risked its business model by spinning off 355 skilled nursing properties and essentially eliminating the higher-yielding component.

If I was building a “pure play” basket today I would own OHI vs. CCP. Both enjoy conservative debt metrics, but OHI is larger (more diversified) and has a longer track record for increasing dividends.

In terms of hospitals, there are essentially two players. One is the “pure play” hospital REIT, Medical Properties Trust, Inc. MPW and the other is Ventas, that just traded in its skilled nursing portfolio for hospitals leased to Ardent.

The tradeoff for Ventas is balanced – removing government pay risks for low-growth, high capital cost assets. I view the Ardent JV deal (with Sam Zell’s company, EGI) as tactical since the partnership should enhance earnings and provide a pipeline for growth in the highly fragmented hospital sector.

MPW shares have rebounded somewhat since the follow-on offering was announced and I’m glad I picked up more shares – closed at $12.69 on Friday.

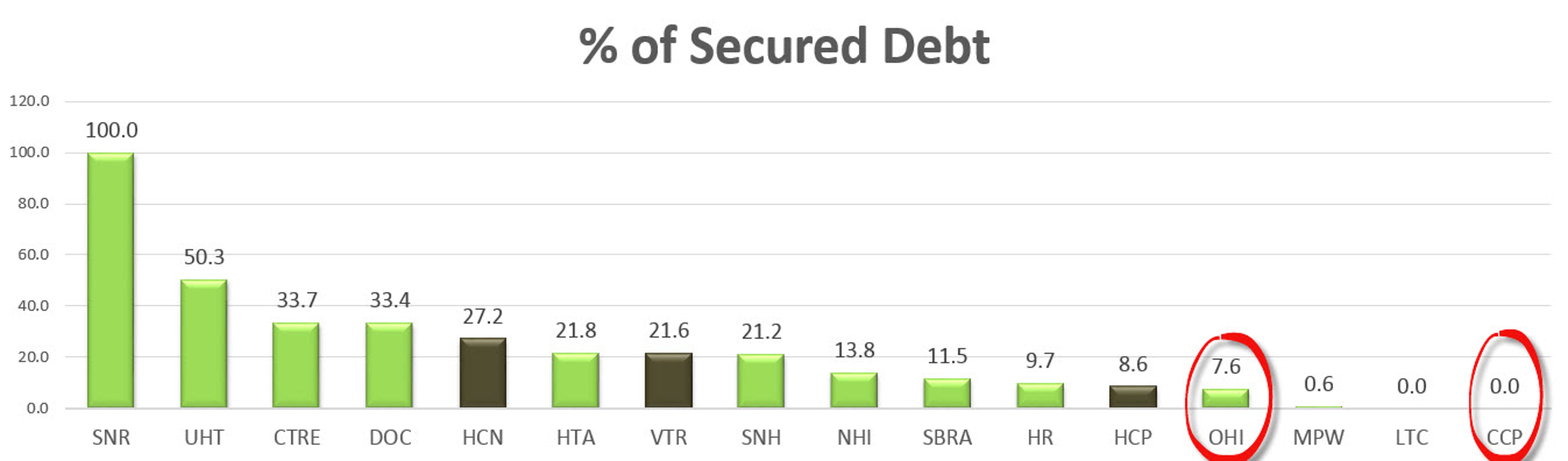

In terms of balance sheets, there is really no comparison. VTR is rated BBB+ by S&P and MPW is rated BB+. Here’s a snapshot comparing the debt profiles for all of the healthcare REITs:

Moving on to Senior Housing we have a similar comparison. There is just one “pure play” New Senior Investment Group Inc. SNR – see my latest article HERE. If you view the debt chart above you can see that SNR has elevated leverage and that’s one reason the shares are trading at a low multiple. Nonetheless, if you can stomach the leverage, SNR offers an attractive dividend yield of 9.1 percent.

Moving onto to arguably the safest healthcare sector is MOB, or medical office buildings. There are 3 “pure play” MOB REITs and I own 2 of them: Healthcare Trust Of America Inc HTA and Physicians Realty Trust DOC. I prefer MOBs over typical office buildings because of the driving forces in healthcare, namely the Affordable Care Act which provides enhanced physician demand.

If I were picking HTA over DOC today I would suggest HTA based on the fact that the company is covering its dividend and also because HTA is investment grade rated (BBB by S&P). Also, HTA recently announced a dividend increase ($.295 per share) of 1.7 percent (from the prior payment).

Overall I consider OHI, MPW, SNR, and HTA to be the best candidates for the “pure play” healthcare basket. The average dividend yield for these 4 REITs is 6.75 percent compared with the average dividend yield for the 3 diversified healthcare REITs of 5.27 percent. Excluding HCP (trading with higher risk due to the assisted living exposure) the other 2 diversified healthcare REITs are yielding an average of 5.0 percent.

In other words, there’s a 175 bps dividend premium for owing the basket of 4 “pure play” healthcare REITs (6.75 percent vs. 5.0 percent) and while that seems like an attractive value proposition, the benefits of owning shares in Ventas cannot be denied.

The only pure play (in my basket) that has successfully managed to increase dividends during the last recession is OHI. MPW cut its dividend and HTA and SNR were not publicly listed REITs during the financial crisis. So while the average 6.75 percent dividend yield may suggest sound investment acumen, the real power in Ventas is the skillful risk management practices that is the brand equity difference – or what I would refer to as the margin of safety.

Mr. Market has clearly telegraphed the message that SNR and MPW are riskier securities, while OHI and HTA appear to be valued appropriately (OHI owns higher risk government-pay related properties and HTA owns lower risk medical office buildings). So it would seem reasonable to assume that VTR should trade at the mid-point of the broader valuation spectrum.

However, in addition to a successful track record for managing risk, VTR also has an exceptional record of dividend performance. The company has increased its annual dividend by an average of 9 percent over the last 4 years and the company said it expects to increase its dividend by 10 percent this quarter.

The Bottom Line: Ventas is “pound for pound” one of the best REITs to own and while there are benefits to owning “pure play” REITs, I consider the pros for owning VTR shares superior to the advantages of owning pure play healthcare REITs. Given the successful spin-off last week I am reiterating my STRONG BUY on the shares.

Editor’s Note: I currently own shares in VTR, HTA, HCP, OHI, DOC, CCP, and MPW. I maintain over-weight positions in the healthcare REIT sector and many of my selections were purchased over two years ago. I am continuing to add shares to select positions when there is market mis-pricing.

Sources: SNL Financial and FAST Graphs.

Disclaimer: This article is intended to provide information to interested parties. As I have no knowledge of individual investor circumstances, goals, and/or portfolio concentration or diversification, readers are expected to complete their own due diligence before purchasing any stocks mentioned or recommended.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.