Despite a fierce blizzard dumping snow on the Eastern Seaboard, including New York City and Washington, D.C., markets remain open and the Fed meeting starts today.

Stocks could tip a bit lower this morning, but traditionally, there’s not much action when the Fed’s in session, and conceivably the inclement weather could also weigh on trading volume. Overseas indices are practically flat. Odds of a rate hike now stand at just above 95%, according to CME Fed funds futures, and there’s a better than even chance of a June rate hike to follow.

Of note, stocks have stayed pretty resilient despite the fact that a few weeks ago, not many analysts or investors had been expecting a March rate hike. A year ago, this kind of swing in expectations might have caused a sell-off. But today, investors seem focused on the fact that a Fed rate hike would arguably signal more confidence in the economy. It’s a very good sign, and shows that many investors appear to have faith in the stock market.

Though eyes remain on the Fed this week, there’s quite a bit of data on the way, starting with this morning’s February producer price index (PPI). The PPI reading came in at 0.3%, above analyst’s consensus expectations for 0.1%, but down from 0.6% in January. Tomorrow brings the consumer price index (CPI) for February (see below), along with February retail sales. Expectations for retail sales look a bit light, as analysts expect growth of just 0.1%, Briefing.com said. That would be down from 0.4% growth in January.

With a new blanket of white stuff coating the streets and a Fed rate hike seemingly baked in, volatility appears to be taking a holiday. The VIX, which climbed above 12 last week, was down to 11.67 Tuesday morning, not far from last week’s lows. VIX has remained below 13 since early January, compared with readings in the 20s through much of last year’s first quarter. It could be interesting to watch VIX tomorrow afternoon after the Fed releases its decision.

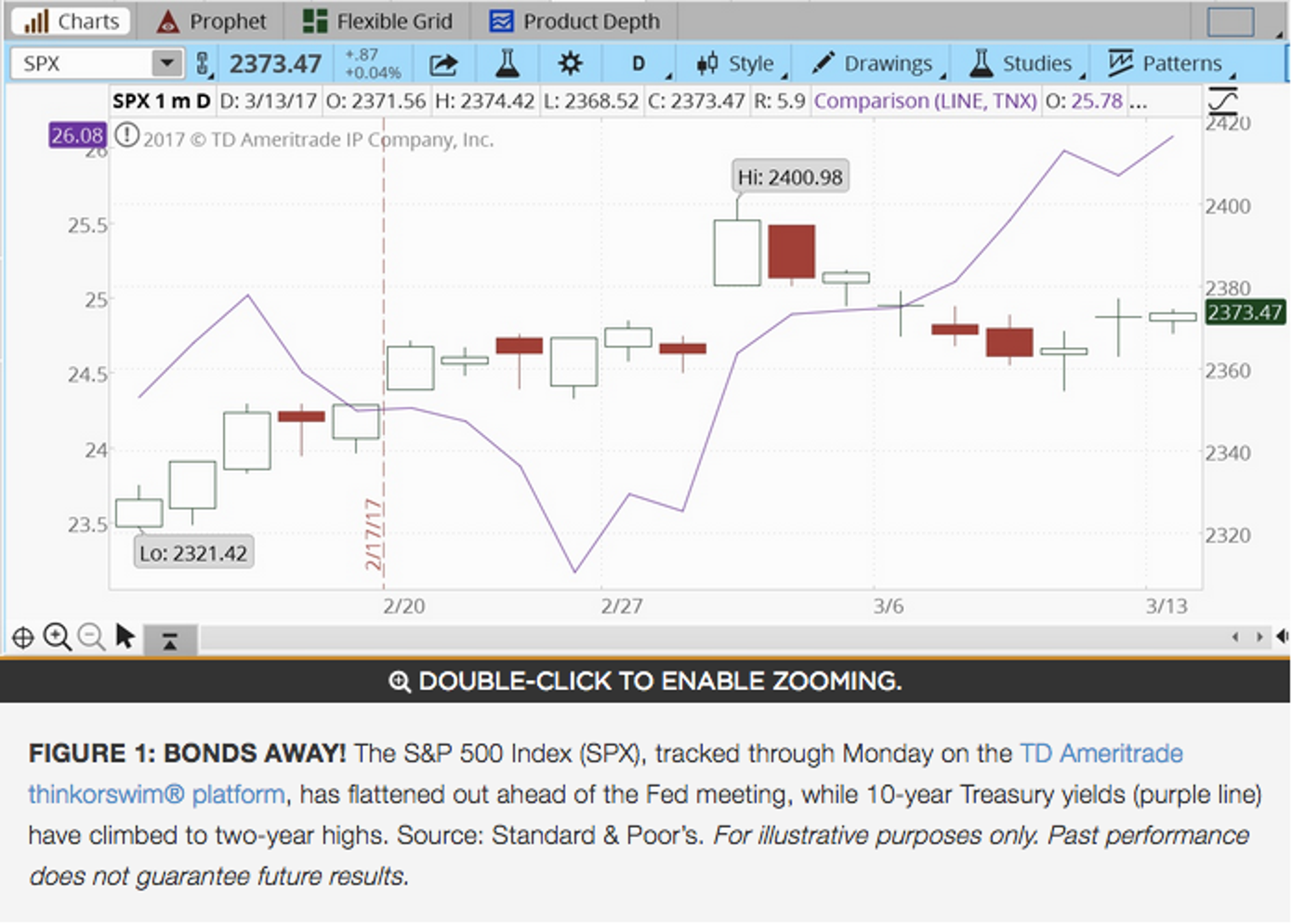

From a technical perspective, resistance for the S&P 500 Index (SPX), appears to be around 2380, near the highs of last week, and beyond that, at the all-time high and the nice round number of 2400, posted on the first day of this month. Support is still well below the market at around 2352. There is an old market adage, "The trend is your friend". This isn't so much about getting long or getting short as it is around fighting the market. Picking a top or picking a bottom on a market is really difficult.

Oil prices stayed near three-month lows amid forecasts for even more U.S. shale production and another gain in the U.S. rig count. There’s a lot of scuttlebutt, too, about whether OPEC countries are sticking to production quotas and how long Saudi Arabia might be willing to keep its production low. The price of gasoline, as tracked by the government, has been pretty stable this winter at around $2.30 a gallon. That’s above this time last year but still a relative bargain, and could help many industries, though not necessarily the energy sector.

Meanwhile, the dollar has trended steady to slightly higher over the last few days, but hasn’t made any big moves. Perhaps the currency could get more direction after the Fed announcement. Gold fell sharply over the last week as a pending U.S. rate hike seemed to grow more apparent, and remained near the psychological $1,200 an ounce mark early Tuesday.

Some positive economic data came out of China this morning. China's industrial output, a proxy for economic growth, expanded 6.3% in the first two months of the year from the same period a year before, MarketWatch reported. That was better than analysts had expected. Fixed asset investment grew 8.9%. However, retail sales were below estimates.

Once, Twice, Three Times…

The Fed has telegraphed three rate hikes this year, with the first likely to take place tomorrow. And Fed futures prices, which arguably represent the market’s best odds maker, forecast about a 50% probability of the Fed coming through and executing all three. But what if job and inflation growth picks up even more and the Fed decides to go beyond three in 2017? There’s actually about a 25% chance of that happening, the futures market suggests, and it would put the Fed funds rate above 1.5% by the end of the year, compared with zero going into December 2015. Though that would be a pretty dramatic two-year change, it wouldn’t be the fastest the Fed has ever raised rates. Some of the recent stock market sluggishness may reflect growing concern that the Fed could get more aggressive. The Fed’s announcement tomorrow is likely to provide more color on the longer-term rate outlook, including whether the Fed is considering more than three hikes in 2017.

Longer-Term Rate Picture

Though 2017 remains a question mark, it’s also interesting to look at what the Fed has done in past rate-tightening cycles. The average rate-hike cycle since World War II consists of slightly more than five hikes, with rates going up by 2.23 points on average, said Sam Stovall, of CFRA. But the most recent hiking cycle, which lasted from 2004 through 2006, saw rates go up 17 times. Stovall believes rates will end this year between 1.25% and 1.5%, and that the cycle we’re in will finish with interest rates at around 2.25%. Even that level would be rather low, historically, so perhaps market fears and headlines about the “end of cheap money” are overblown. Some of the sectors that traditionally have performed best during rate hiking cycles include info tech, energy, and consumer discretionary, Stovall said, though past performance doesn’t necessarily point toward future results. The worst performers have been consumer staples, telecommunication services, and utilities.

Consumer Prices Seen Relatively Flat

After a surprisingly large jump of 0.6% in January, things look calmer for the consumer price index (CPI) in February. Data due early Wednesday are expected to show just a 0.1% rise, according to analysts’ consensus estimates compiled by Briefing.com. With energy and food prices stripped out, the estimate is slightly higher at 0.2%. Also, PPI was higher than expected Tuesday, so it’s worth checking to see if CPI also produces an upside surprise. One interesting metric to watch is food and beverage prices, which edged up 0.1% in January but had been flat the previous four months. Cheap food prices, some analysts say, could be making grocery shopping more attractive for many consumers, with possible negative consequences for restaurants.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.