Growth Scare Ahead

“Consequently, if consumption and nonresidential investment holds up, with the worst of the residential investment and inventory contraction complete, and the government outlays exceeding receipts by 6% of GDP, a recession of any consequence is a low probability outcome.”

2023 Outlook: 9 to 4, but then what, December 3, 2022

This was the short version of our economic outlook a year ago, we will detail our 2024 expectations in detail next week, needless to say, our outlook is less sanguine for 1H24 than it was for 1H23. In the holiday shortened week the equity market followed favorable seasonality higher, however, the front-end of the Treasury curve drifted back towards 5% and with the Treasury Department selling $54 billion of 2s and $55 billion of 5s on Monday and $39 billion of 7s on Tuesday, we suspect weak bank demand will make these auctions in the soft underbelly of the curve a tough sell and consequently will put pressure on the entire curve. The last couple of belly of the curve (2s, 5s & 7s) auction weeks have resulted in pressure on longer maturities. We continue to be wary of Treasury rallies that are not led by 2s, which requires a confirmation of a Fed pause and ultimately a full pivot.

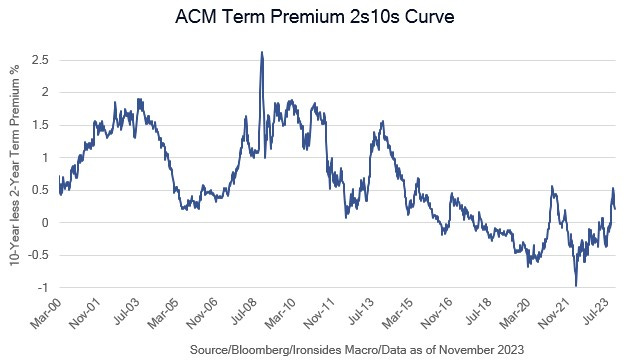

As a follow-up to last week’s note, Necessary and Sufficient, we were asked for additional clarity on our view that the Treasuries valuation was stretched. While term premium models are somewhat controversial, they remain historically low. We suspect Fed holdings of nominal and inflation protected Treasuries are suppressing rates and inflation compensation (breakevens).10-year real rates (TIPS) averaged 2.1% during the pre-financial crisis globalization period when China and Japan were accumulating Treasuries to suppress their exchange rates and grow exports. A return to either the pre-financial crisis foreign central bank demand for Treasuries or post-financial crisis QE regime is unlikely anytime soon and of course the elephant in the room is the stock of government debt and its expected growth rate. Given the outlook for supply and demand, the term premium and real rates should be higher than pre-financial crisis. Finally, nominal and inflation protected 10s at 4.5% and 2.2%, implying inflation at 2.3%, infers a return to the Fed’s target, an outlook we think is unlikely without a major improvement in the federal debt and deficits.

A growth scare could stabilize the Treasury market, but only after the Fed confirms a full pivot. As we discussed last week, a greater than expected increase in the unemployment rate is the most likely catalyst for FOMC rate cuts in 1H24. While the front-end of the Treasury market will respond favorably to an unemployment rate above 4%, it seems likely the equity and credit markets are likely to struggle until the FOMC loses the higher for longer, Ghost of Arthur Burns, language in every participant speech and appearance. If the November employment report starts this process, favorable seasonality might be an offset to growth and earnings concerns, however, in 1Q24, the combination of fixed income government and private sector supply and a growth scare could be a toxic mix. For this reason, we think it is too early for small caps or financials.

Figure 1: Both the 2-year and 10-year Adrian Crump & Moench term premiums are negative; the 10-year model made it 48bp in October, it is back in negative territory after the rally.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.