Pass the stuffing and the retail earnings.

It’s two days until Thanksgiving, but there’s no break from the steady hum of retailers reporting. The “brick-and-mortar” stores still have something to say. Today’s menu includes Best Buy Co Inc BBY, Dick’s Sporting Goods DKS, and Dollar Tree Inc. DLTR.

Major stock indices looked flat to start Tuesday after yesterday’s record-breaking session. Trade remains top of mind with headlines suggesting more progress toward a possible phase one agreement between the U.S. and China. History has taught investors not to put too much hope into any quick resolution, but both sides might be feeling pressure to get something done ahead of the new year.

The Fed also stepped into the news cycle overnight after Fed Chairman Jerome Powell said in a speech that the Fed is “strongly committed” to maintaining 2% inflation. Some analysts interpreted this as another sign that rates won’t rise anytime soon. Dallas Fed President Robert Kaplan followed up Tuesday morning, telling CNBC that the Q4 economy looks “weak” due to businesses cutting inventories as a result of the trade war, but he expects a return to 2% growth in 2020. Rate policy is in the right place, he added.

Stocks don’t look too committed to any direction this morning, but considering the record-setting rally yesterday, it would probably be seen as a victory even if they hold current levels. Treasury yields fell slightly early Tuesday, with the 10-year yield back down to 1.73%.

Tuesday’s Retail Scoreboard Mixed

It’s been a pretty good retail earnings season despite some high-profile misses from Home Depot Inc HD and Kohl’s Corporation KSS. With unemployment at 50-year lows, it would be surprising not to see retailers doing well, and those that haven’t delivered the goods, so to speak, have seen their stocks get slammed.

Best Buy got things going with a solid quarterly performance, beating analysts’ consensus earnings and revenue estimates. It also raised guidance, and shares rang up 4% gains in pre-market trading. The company has done a great job keeping itself relevant and its stores updated.

Dick’s did even better in early trading, rising 13% in the pre-market after easily topping estimates and raising guidance. What’s interesting to see is how investors continue to reward retailers that beat, unlike last year when beating consensus often was met with a collective yawn.

Still, investors keep punishing retailers that miss, as DLTR found out early Tuesday. Shares crumbled more than 12% after the company came up short of analysts’ earnings expectations.

On the economic calendar, new home sales for October loom later this morning after existing home sales last week made a decent showing. Analysts look for new home sales to come in at a seasonally-adjusted clip of 710,000, according to Briefing.com. Last time out, sales slipped slightly month-over-month but rose sharply year-over-year, with sales of higher-priced homes sagging a bit. That could be an interesting potential countertrend to watch if it continues.

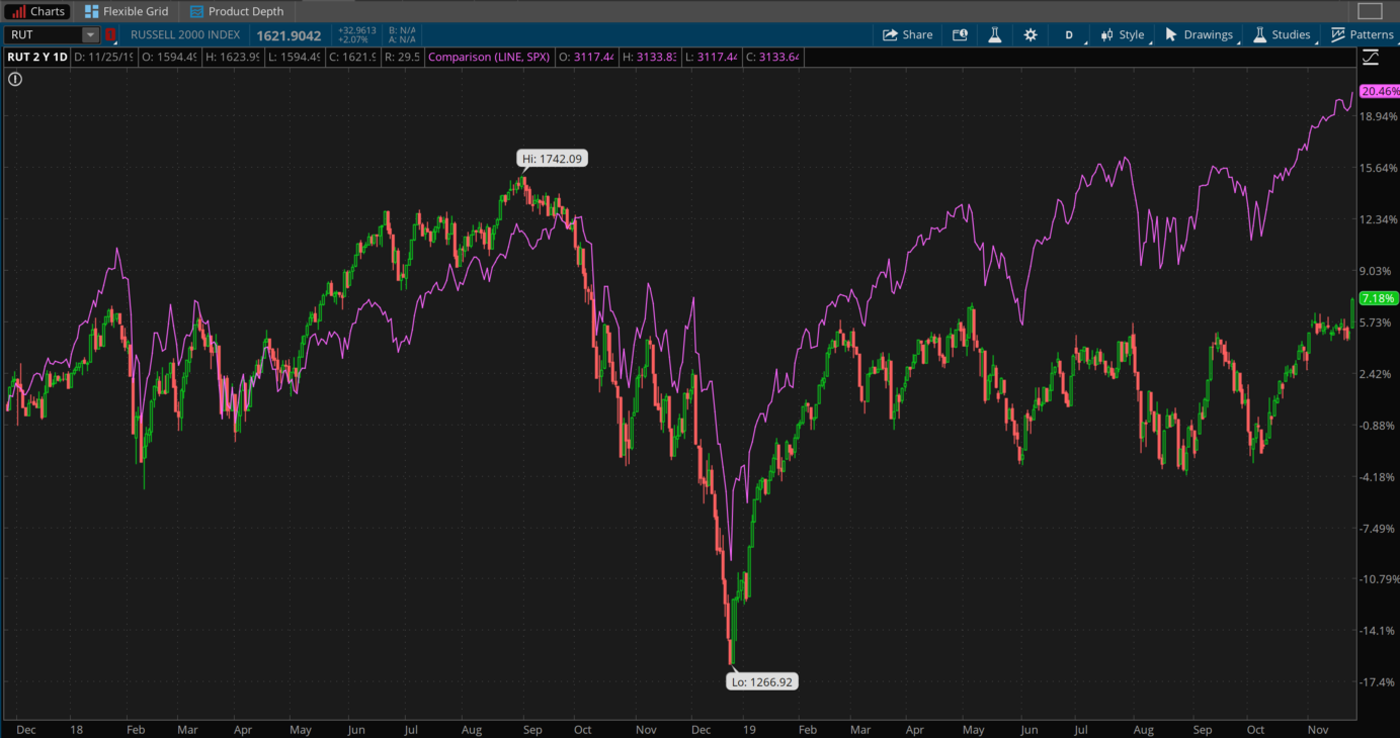

Small-Caps Fired Up

How often as a kid did your mom tell you, “If everyone else did (name the horrible deed) would you?”

Well, if the Russell 2000 small-cap index (RUT) were a kid, that’s how it might feel right now. Everyone else (all the other major U.S. stock indices) has made new all-time highs, but the RUT languishes well below its 2018 all-time peak of above 1700.

On Monday, the RUT looked like it was out to start catching up. It climbed more than 2% to outpace all the other major indices and post a new 12-month high, led by strength in regional banking, health care, and technology stocks within the index. The tech strength also showed up among bigger names to help the Nasdaq (COMP) shoot up 1.3% to a new record high, and the S&P 500 Index (SPX) and Dow Jones Industrial Average ($DJI) joined the club.

Once again, the so-called “FAANG” stocks had a nice day, with Netflix Inc NFLX gaining 1.6% despite a downgrade. Technology led all sectors Monday as the Semiconductors put on another performance to remember. Shares of Nvidia Corporation NVDA climbed nearly 5% after an analyst upgrade as investors contemplated recent strength in cloud data center growth and gaming.

Meanwhile, gold and volatility continued to edge lower amid optimism over a possible U.S./China Phase One deal. The Cboe Volatility Index (VIX) fell below 12. That’s about the lowest VIX has been all year. This weakness in volatility is starting to hurt some of the “risk-off” assets like Utilities and Real Estate where investors sometimes hide amid times of market turbulence.

Bonds aren’t doing much of anything to start the week. It looks like the 10-year Treasury yield has found a comfort zone right around 1.75% and keeps circling that level like a moth around a flame. It represents close to the low-end of the recent range. The dollar index, on the other hand, quietly creeps higher. It finished above 98.3 on Monday. The recent high is slightly above 99, so that could be a level to watch.

Deere Season Starts Wednesday

Before turkey, there’s Deere & Company DE. The huge agricultural company is due out with earnings tomorrow morning, and investors might want to listen closely to the call for any new observations from its executives about the situation in China and how the trade war is affecting U.S. farmers.

Back in August, when DE last reported, the company’s earnings missed Street expectations and its CEO said a “high degree of uncertainty … continues to overshadow the agricultural sector.” Basically, the takeaway was that farmers were delaying equipment purchases due to that uncertainty.

Since then, we haven’t had any solid movement on the trade situation, so one question is whether farmers are still saving their money for better times. If you look at the price charts for corn and soybean futures recently, it doesn’t look like there’s much reason for them to be cheering, and that might mean more tough sledding for DE.

On the other hand, if there’s progress on a new North American trade agreement, that could potentially help industrial companies like DE, some analysts say. That’s not something that would have factored into DE’s recent quarter, naturally.

CHART OF THE DAY: HEY, WAIT FOR ME! The small-cap Russell 2000 Index (RUT-candlestick) made a new 12-month high Monday but remains well below its all-time high posted more than a year ago. Its progress has lagged behind the S&P 500 Index (SPX-purple line) over the two years tracked by this chart. A return to new peaks for the RUT might be a bullish development, showing that investors have begun embracing what can be riskier buys outside of the large-cap big name companies. Data Sources: FTSE Russell, S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Two Still a Tangle for 10-Year: Is it possible the 10-year yield could make another run at 2% before the end of the year? That’s a mark it couldn’t quite reach earlier this month and hasn’t touched in nearly four months. Now it’s treading water below 1.8%. Another push for 2% might not be out of the question if a trade deal looks more likely or if there’s solid manufacturing and jobs data early next month. Still, as one analyst said on the TD Ameritrade Network recently, it’s hard to see the 10-year yield climbing back above 2.25% anytime soon. There’s just too much quantitative easing pressing down yields in Europe and Japan, and that makes the U.S. bond market seem pretty attractive to many investors facing negative yields elsewhere. When those investors jump into the U.S. bond market for yield, that sends bond prices here higher and yields get pushed downward.

Targeting Two: Here’s another “2” question to contemplate: Can inflation hit the Fed’s 2% year-over-year target this Wednesday when Personal Consumption Expenditure (PCE) prices come out? The headline number has been trending just shy of 2%—the Fed’s target inflation level—for months, coming in at 1.7% year-over-year in September, down from 1.8% in August. Month-over-month, however, was flat in September.

Going into October’s report, analysts look for just 0.1% month-over-month growth, which means we’d have another month of annual inflation under the Fed’s target. The wild card, if there is one, is that the producer price index (PPI) rose a solid 0.4% in October. Some of that was driven by what might be short-term issues like energy costs, but if producer prices do keep rising, the concern is it could eventually translate into higher product costs for consumers.

Tepid GDP Seen Likely—Here and Across Pacific: The other big data report tomorrow morning is quarterly gross domestic product (GDP). This is the government’s second crack at estimating Q3 growth, with the last one coming in at a tepid 1.9%. The consensus estimate going into tomorrow is for no change from that, according to Briefing.com. If so, the economy would remain stuck at the lowest quarterly GDP growth since Q3 2016.

It’s possible the trade war is playing a part, along with slow overseas economic growth. It probably doesn’t help the U.S. economy that China—one of its biggest trading partners—is experiencing its slowest growth since 1992 at 6% in the most recent quarter. A think tank in Beijing said earlier this month that GDP growth in China could fall below 6% in 2020, and that’s in line with what the International Monetary Fund (IMF) is thinking. Meanwhile, economists here in the U.S. look for Q4 U.S. GDP to be just above flat, with the Atlanta Fed’s GDP Now indicator at 0.4%.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

Image by cocoparisienne from Pixabay

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.