Ka-ching! Amid swirling investor anxiety over the state of the world economy, it seems that consumers are offering the market a bright spot by continuing to spend at the cash register and online.

Walmart Inc WMT shares jumped over 6% after the retailing giant reported earnings, revenue, and same-store sales that beat expectations. It also boosted its full-year guidance. Meanwhile Chinese e-commerce heavyweight AlibabaG Group Holding Ltd BABA also advanced more than 3% after beating on both the top and bottom lines.

The BABA report offers an encouraging counterpoint to official Chinse data that showed disappointing retail sales numbers in the Asian nation. And the WMT news offers a silver lining for traditional retailers after yesterday’s down moves in Macy’s Inc M and Kohl’s Corporation KSS among others following a dismal earnings report from M.

The upbeat outlook from WMT helped stocks reverse course after a bruising day yesterday, and better-than-expected retail sales data from the United States also helped improve the mood among investors. July retail sales rose 0.7%, and excluding auto sales they jumped a full 1%. A Briefing.com consensus had expected a 0.3% gain for both data points.

But perhaps the most encouraging thing to help shift sentiment this morning was tariff sentiment in China after an official said the Asian nation is hoping the U.S. will meet it halfway on trade issues. That came after a Chinese statement threatened trade countermeasures.

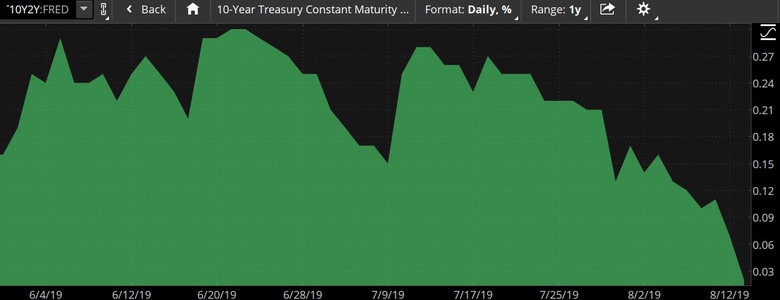

Meanwhile, the closely watched spread between the 2-year and 10-year Treasuries has returned to a more normal state, but it’s still narrow a day after the yields inverted and caused investor worries about a recession to ratchet up sharply.

In short, while there have been some encouraging signs this morning, the day is young and we’ve already seen a wide range in the major indices. One thing remains clear: markets are still on edge.

Wednesday Market Wrap

That’s understandable given the drubbing stocks took yesterday as the U.S. bond market flashed a signal for a potential recession, adding to investor worries stemming from disappointing economic data out of China and Germany.

After a brief but strong rally Tuesday on the announcement that the White House would delay tariffs on some goods such as laptop computers and cell phones, the market plunged Wednesday as the yield on the 10-year Treasury slipped below that of the 2-year.

This so-called inversion has been a signal that has preceded most recessions since WWII, contributing to investor jitters as the heightened volatility that has plagued the market since last week continued. (Investors may want to keep in mind that past performance doesn’t guarantee future results.)

The ratcheted-up anxiety followed German GDP data that showed Europe’s largest economy contracted by 0.1% during Q2. Also, official figures revealed Chinese industrial production slowed to the slowest rate since 2002, and retail sales growth there was below expectations.

Investors appeared to have flipped the risk-appetite switch to “off,” selling stocks and crude oil futures and looking for relatively safer assets. Among these, market participants bought gold futures, pushing the metal’s price on the futures market to its highest settlement since April 2013.

Meanwhile, investors also bought U.S. government debt, which is also often seen as a safe haven amid market turmoil, and the 30-year Treasury fell to a record low. It has since dropped below 2% in an indication of more safe-haven buying and has spent much of the morning gyrating above and below the 2% line.

Financials Sector Takes It On the Chin

Falling yields left bank shares vulnerable, and the Financials sector fell sharply. It can be harder for banks to earn money when they can’t charge as much interest on longer-term loans compared to the shorter-term rates they pay out to depositors.

The Energy sector was also particularly hard-hit as oil prices faltered on fears about demand as the global economy shows signs of weakening. A rise in U.S. inventories when analysts had been expecting a decrease also pressured oil.

Although equity investors were running for the exits (or at least taking some money off the table), there may be a silver lining on the horizon. Amid the market turmoil, investors became more optimistic about a larger rate cut by the Fed next month, boosting the probability for a 50-basis-point cut to more than 25%.

It was also interesting to note that former Fed chief Janet Yellen told Fox Business Network that this time around the yield curve inversion “may be a less good signal” of a recession. “The reason for that is there are a number of factors other than market expectations about the future path of interest rates that are pushing down long-term yields,” she said.

As we’ve noted before the 2-year/10-year spread isn’t a perfect recession predictor, and much of the buying in the 10-year Treasury recently may be trade-based rather than solely from worry about the economy. Investors may also want to keep in mind that there tends to be a lag between an inversion and a recession, and during that time the market can actually gain ground.

Will Consumer Strength Last?: The further evidence that the U.S. consumer remains strong is encouraging. With consumer spending accounting for the biggest single chunk of gross domestic product, that segment of the economy is crucial, especially given the economic headwinds from the trade war. President Trump this week gave a nod to that importance when he said his administration was pushing back tariff implementation on certain goods to make sure there isn’t an impact on consumers during the heart of the Christmas shopping season. But if those tariffs on certain electronics, clothing, and footwear do end up going into place in December, we’ll have to see how much extra cost the U.S. consumer is willing to bear before deciding to not buy as much in stores and online.

Technically Speaking: With all the market anxiety going on right now, it might be easy to forget that the S&P 500 Index (SPX) isn’t all that far away from record high just above 3,000 hit late last month. And we’re still a good bit above the low we saw in June around 2730. It’s arguable that stocks may trade within the 2700-3000 range for some time. The trade war seems to be putting a cap to the upside while decent consumer spending, gross domestic product and jobs data seem to be keeping a floor under the market from an economic fundamentals perspective.

Information from TDA is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

Image Sourced from Google

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.