The Non-Disinflation Issue

Lots of interesting news this week where we address these important questions:

-

Is the disinflation story done now?

-

Can the Japanese yen recover?

-

Are we finally about to get a Bitcoin ETF GBTC?

-

How much trouble can we expect for Disney DIS?

-

Is the employment situation better than we thought last week?

Ready for the week? Let’s dive in:

-

Oil Prices Are Going to Kill Disinflation:

Much of the market optimism this year has been related to excitement about disinflation. Disinflation is not a reduction in prices; but rather, a slowing in the rate of price increases. The primary reason for the decrease in inflation this year has been energy prices coming down from their 2022-highs. This week, Saudi Arabia and Russia both announced they will extend production cuts for months. As DKI predicted last year, the White House is having difficulty replenishing the strategic petroleum reserve after drawing it down to the lowest level in 40 years.

The White House said they’d refill at $70 oil. They didn’t do it.

DKI Takeaway: With energy prices going from huge declines to a y/y price increase, we expect the consumer price index will start to rise again. This makes a Federal Reserve pivot to lower interest rates less likely. While DKI can’t help you reduce the cost of filling your car or heating your home, we do have a number of stock picks that will benefit from higher oil prices. Premium subscribers can find that on the Current Recommendations page.

-

The Yen is Falling - Again:

Alone among the major central banks, the Bank of Japan has been trying to keep the yield on their 10-year government bond below 1%. They’ve succeeded, but at the cost of the currency. The yen is now falling towards 150 to the dollar, a huge problem for an island nation with few natural resources and a need to import energy.

If you don’t like inflation in the US, imagine seeing your currency do this.

DKI Takeaway: DKI started warning about a potential Japanese sovereign debt default in October of 2022 and had a section in our July letter titled “Is the Federal Reserve Going to Crash Japan”. Soon, the Bank of Japan will need to raise rates on its debt to protect the yen. At that point, higher interest expense on Japan’s massive debt will lead to budgetary problems and more currency printing. That leads to inflation and a weaker currency. There is no good way out of this spiral. A potential currency collapse of the world’s third largest economy is a market risk that’s currently being ignored.

-

SEC Loses Important Bitcoin Lawsuit:

Last week, the SEC lost a lawsuit filed by Grayscale, the company that runs the Grayscale Bitcoin Trust ($GBTC). The SEC had rejected Grayscale’s application to convert the trust into an exchange traded fund (ETF). The Court found that since the SEC had approved an ETF based on Bitcoin futures, it was applying a different or arbitrary standard in not allowing a spot Bitcoin fund.

With or without an ETF, Bitcoin issuance is approximately 900 coins a day. That will decrease.

DKI Takeaway: The SEC may choose to delay, but we think there will be spot Bitcoin ETFs sooner rather than later. The most likely scenario involves approving multiple ETFs including the ones from massive fund managers Blackrock and Fidelity. The supply of Bitcoin can’t expand to accommodate the coming institutional demand so the only thing that can adjust is the price. Additional commentary is on the DKI blog.

-

Disney – Zero Shareholder Value in Almost 10 Years:

Despite buying Lucasfilm to take over the massive Star Wars franchise, and turning Marvel into a superhero film blockbuster machine, Disney ($DIS) has created no shareholder value in almost a decade. The film franchises are producing lesser returns on bigger budgets, but the key issue is the loss of value at ESPN. The sports network used to be a $10 a month tax on over 100 million US cable subscribers, but streaming television is allowing people to cut the cord and avoid paying for content they don’t want.

A content machine that’s declining in value. Graph from TIKR.

DKI Takeaway: ESPN always had an abusive business model grabbing over $100/year from almost every household in the country regardless of their interest in sports. Ben Thompson at Stratechery gives an excellent description of the history. At Silver Arrow, we published a 50-page white paper in 2012 predicting disaster for the traditional television model including (and especially) ESPN. We were early and correct. You’re welcome to check out TV is Next on the DKI Blog.

-

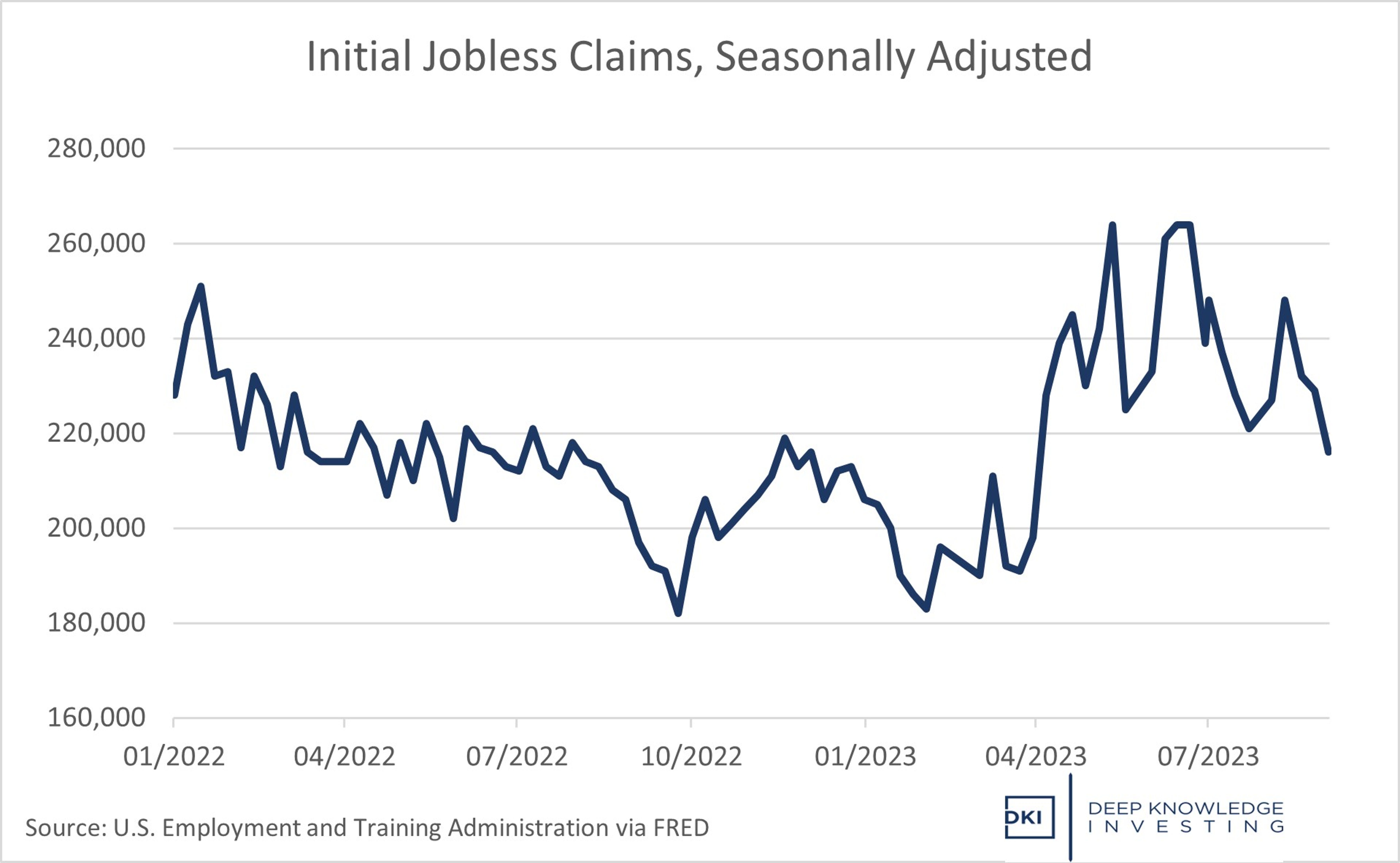

Unemployment Down – More Mixed Data:

DKI has been pointing out the inconsistency in macro trends for almost a year now. This week, we saw initial jobless claims of 216k (seasonally adjusted) which was down from last week’s 230k. Total claims of 1.679MM were down by 40k. Labor costs are up more than 2%, but productivity is up even more at 3.5%. All of this was better than expectations.

Pretty big drop in the last few months.

This trend is positive as well with a still-low unemployment rate.

DKI Takeaway: Last week, the market was up on weaker employment news because people thought it would make the Federal Reserve less likely to raise interest rates at the September meeting. The market was down on this positive unemployment news because a stronger employment market and higher wages might lead to more rate hikes. As of today, DKI agrees with market consensus that says the Fed will hold firm in September, but we still continue to believe Chairman Powell: “Higher for longer”.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.