(Friday market open) A mild October U.S. jobs report Friday doesn’t appear likely to dent recent market optimism about interest rates. The benchmark 10-year Treasury note yield fell another 10 basis points immediately after the data, potentially loosening pressure on stocks.

Jobs growth was 150,000 in October, the Bureau of Labor Statistics (BLS) reported, and unemployment edged up to 3.9% from 3.8% the month before. Wages rose just 0.2%, below analysts’ expectations, and the government removed 101,000 jobs it had previously tallied for August and September.

Analysts had expected October jobs growth of 180,000, according to Trading Economics. Wages had been expected to rise 0.3%. The 150,000 jobs added in October was down substantially from a revised 297,000 in September, and also from a revised 165,000 in August.

“The jobs data looked weak across the board relative to expectations, but a 150,000 print is still relatively strong,” says Kevin Gordon, senior investment strategist at Schwab. “It’s just some of the trends that still look worrisome—particularly the unemployment rate, which is now up by 0.5% over the past six months. We’ve never seen that kind of move to the upside without already being in a recession.”

Chances of a December rate hike fell to 10% on Friday after the report from 20% on Thursday, according to CME futures.

Today’s jobs data came on the heels of Wall Street’s four-day win streak that lifted major indexes to two-week highs, fueled by interest-rate optimism. Stocks had a mixed overnight performance, with the Nasdaq (COMP) falling as Apple AAPL shares slipped 3% following earnings. The iPhone maker’s results were dragged down by weaker-than-expected revenue out of the greater China region.

The S&P 500® Index (SPX) closed above 4,300 on Thursday for the first time since October 18, clawing back above its 200-day simple moving average after posting a five-month low last week. Investors are increasingly confident the Fed’s quarter-point increase in late July might have been the last of the current tightening cycle, and the 10-year Treasury note yield fell to three-week lows near 4.55% by Friday morning. They tumbled further after the October jobs data. Volume was above average yesterday across Wall Street and gains were broad across various sectors, possibly a sign of strong conviction in this rally.

The major indexes start Friday up 4% to 5% for the week, making this the best weekly performance in about a year.

Morning rush

- The 10-year Treasury note yield (TNX) fell 11 basis points to just under 4.56%.

- The U.S. Dollar Index ($DXY) dropped to 105.35.

- Cboe Volatility Index® (VIX) futures fell to 15.3.

- WTI Crude Oil (/CL) rose 1.2% to $83.50 per barrel.

Just in

Though today’s mild Nonfarm Payrolls report is just one month of data, not a trend, it could strengthen ideas that the economy is responding to the Fed’s tighter monetary policy—a bullish development for interest rates. Slower jobs growth can reflect an economy that’s cooling, keeping inflation on simmer. Inflation has already decreased dramatically from a year ago as the Fed raised rates to 20-year highs, but so far it hasn’t appeared to have had a negative impact on the labor market. .

Digging a bit deeper into the report, annual wage growth was 4.1%, still relatively high and above the 4% pre-report average analyst estimate. It was down from 4.2% in September, however. Wages are closely watched for possible inflationary impact, though Fed Chairman Jerome Powell said this week that wage growth wasn’t a major driver of recent inflation.

Also, the 0.2% monthly wage rise is more indicative of current conditions, and was below expectations, notes Collin Martin, a director of fixed income strategy at the Schwab Center for Financial Research.

The biggest areas of October jobs growth were health care and government, which both added more than 50,000 positions. But manufacturing employment fell 35,000—more than analysts had expected and another sign of weakness on that side of the economy following soft data earlier this week. However, that sector saw an impact from the autoworkers’ strike, so the weakness might be temporary. Construction employment trended up, which aligns with strong recent demand for new housing.

Stocks in spotlight

Apple (AAPL) shares gave back some of their recent gains after the company reported slightly better-than-expected earnings late Thursday. Revenue fell year-over-year for the fourth quarter in a row, but less than analysts had expected. iPhone revenue of $43.8 billion slightly beat Wall Street’s thinking and was up from a year ago, but Mac revenue slumped.

The company’s services revenue, a key margin support factor, beat expectations and rose 16% from a year earlier. For the current quarter, Apple expects revenue to be similar to the same quarter last year, an outlook below Wall Street’s thinking. This could be one element dragging the stock this morning.

Walt Disney DIS takes center stage next week amid an otherwise quiet period for corporate data following recent earnings from the biggest tech and communication services firms. The action returns in mid-November when major retailers open their books ahead of the holiday shopping season. Uber UBER is another well-known company reporting next week.

Banks and other financial companies led yesterday’s gains, with the KBW Regional Banking Index (KRX) surging more than 5%. Energy and retail shares were also strong. Small-cap stocks outpaced their larger counterparts, with the Russell 2000 Index (RUT) jumping 2.5%. That was a change from recent weeks when the Russell 2000, with its heavy exposure to financials, featured some of Wall Street’s worst performance.

What to watch

Next week: There’s a dramatic fall-off in news and events the first full week of November. Central bank meetings and jobs data are over, and earnings season is close to two-thirds complete. Things are happening, just not the high-level ones that often cause volatility.

Monday’s Fed Senior Loan Officer Opinion Survey (SLOOS) provides the latest quarterly glance into the standards of bank lending and business and household demand for loans. See more below.

Monday also brings two U.S. Treasury bill auctions, with 3-month and 6-month Treasuries on the block. Results could help set the tone for Treasury yields, which rose after recent auctions showed waning demand for new U.S. debt. A 10-year note auction next Wednesday could also have a market impact.

Eye on the Fed

Early today, futures trading pegged chances at 90% of the FOMC holding its benchmark funds rate at the current 5.25% to 5.50% target range following the December 12–13 meeting, according to the CME FedWatch Tool. That’s up from 80% chances of a pause dialed in yesterday before the jobs report. Chances of rates staying on pause following the FOMC’s January 30–31 meeting are 84.6%.

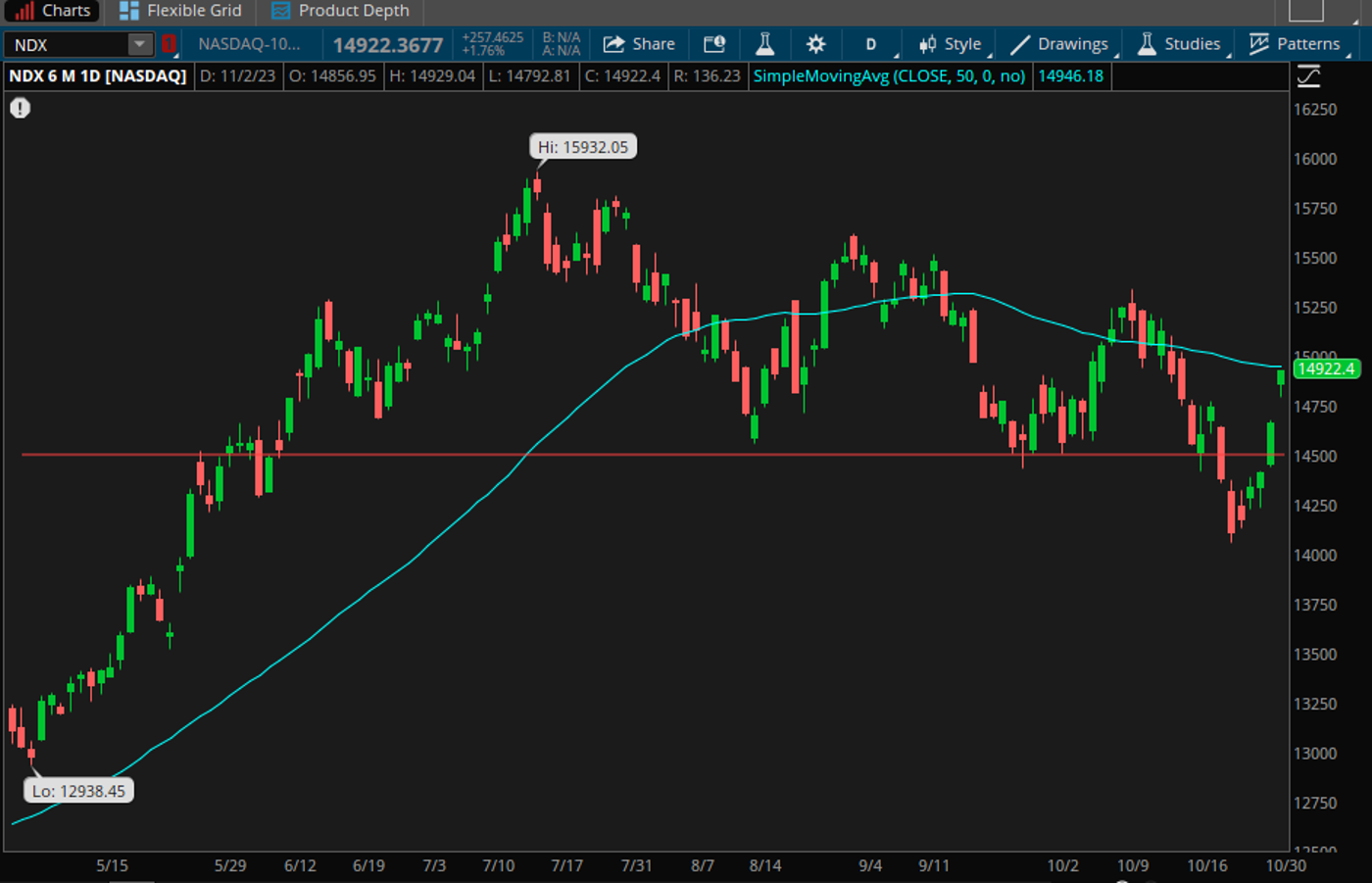

Talking technicals: The Nasdaq 100 (NDX) is now above the prior key support level of 14,500, breathing life back into technology and other growth sectors following sub-par post-earnings reactions from mega-cap tech. “Earnings this week from companies such as Advanced Micro Devices (AMD), Shopify (SHOP), Lemonade (LMND), and Super Micro Computer (SMCI) likely helped validate the artificial intelligence (AI) secular growth story,” says Nathan Peterson, director of derivatives analysis at the Schwab Center for Financial Research. Near-term resistance is at the 50-day simple moving average of 14,946.

Thinking cap

Ideas to mull as you trade or invest

Survey says: The Fed’s Senior Loan Officer Opinion Survey (SLOOS) is drawing more attention lately after last spring’s bank failures. The new survey is due out at 2 p.m. ET Monday. “Lending conditions are currently restrictive,” says Schwab’s Collin Martin. “Banks are tightening their lending standards and charging higher rates (spreads), while demand is down. So, it’s coming from both sides: banks are not lending as much, and borrowers are not as interested in borrowing. The previous report showed that conditions tightened even more, but the pace of tightening had slowed. Next week will be interesting to see if that trend continues.”

Lending matters: A tighter loan environment tends to be tough for growth companies that need loans to finance new hiring, construction, and product development, and for small-cap companies and small businesses that tend to be more dependent on loans in general. About 46% of U.S. employees work for small businesses, according to Forbes, so a long-term tight loan environment ultimately could affect employment conditions. However, if loan growth slows, it could mean the market is doing some of the Fed’s job for it without as much need for additional rate hikes.

Cloud counting: Cloud growth is often considered a barometer of business conditions, reflecting corporate demand for data storage, analytics, and more recently, AI. One way an emerging recession might reveal itself could be slowing cloud demand. Based on earnings to date, Q3 cloud demand appeared relatively strong despite Alphabet’s (GOOGL) disappointing growth. Microsoft’s Azure sales reaccelerated to outpace Wall Street’s expectations, and guidance looked solid. Amazon, the sector leader, reported a 12% rise in Amazon Web Services (AWS) revenue, in line with analysts’ expectations. However, that number might not have captured all the growth. Amazon said on its earnings call that several new deals signed in September didn’t show up in Q3 numbers. “We’re encouraged by the strong last couple of months of new deals signed,” an Amazon executive said. However, Amazon also said it’s seen “elevated cost optimization” versus a year ago from cloud customers. Generative artificial intelligence (AI) continues to be “top of mind for most companies,” Amazon added. The cloud seems bright enough now, and a demand pullback some companies cited earlier this year didn’t lead to recession.

Calendar

Nov. 6: Fed Senior Loan Officer Opinion Survey.

Nov. 7: September Consumer Credit and September Trade Balance, and expected earnings from D.R. Horton (DHI), Uber (UBER), Zimmer Biomet (ZBH), eBay (EBAY), and Rivian (RIVN).

Nov. 8: September Wholesale Inventories and expected earnings from Biogen (BIIB) and Walt Disney (DIS).

Nov. 9: Expected earnings from Illumina (ILMN) and Becton Dickinson (BDX).

Nov. 10: University of Michigan Preliminary November Consumer Sentiment.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.