(Monday market open) Big retailers take center stage this week, with earnings expected from Home Depot HD, Target TGT, and Walmart WMT, among others. Fittingly, July’s Retail Sales report is also on tap, putting the consumer in focus as investors await Wednesday’s release of minutes from the last Federal Open Market Committee (FOMC) meeting.

The bulk of earnings season is over and volume could be light, as some folks fit in vacations between earnings and back-to-school time. When volume thins, volatility can ignite. Anyone trading this week should take that in context and not let unusually quick intraday moves knock them off stride.

As noted last week, stocks haven’t gotten much traction on recent rallies and the so-called “mega-caps” have flagged. This could reflect historically firm valuations and recent agency downgrades to banks and U.S. credit. Still, “buy the dip” has been evident. The dollar and Treasuries began Monday slightly higher, possibly a sign of defensive sentiment.

With earnings almost finished, the coming weeks could turn focus squarely toward macroeconomic trends, especially as the Federal Reserve’s Jackson Hole conference approaches later this month. Also, geopolitics might get more attention. Last week’s announcement of more limitations on U.S. tech investment in China made it clear that despite recent talks, tensions remain high.

Major indexes are coming off consecutive lower weeks—the first time that’s happened all year for the tech-packed Nasdaq Composite (COMP). Stronger-than-expected wholesale inflation readings Friday sent long-term Treasury yields near 10-month highs, and technology shares extended their recent slide.

Morning rush

- The 10-year Treasury note yield (TNX) inched lower to 4.16%.

- The U.S. Dollar Index ($DXY) rose slightly to 102.94 and is at one-month highs.

- Cboe Volatility Index® (VIX) futures rose to 15.62.

- WTI Crude Oil (/CL) slipped to $82.76 per barrel.

Just in

Some of today’s Treasury and dollar strength could reflect fresh worries about China’s property market after Country Garden, one of China’s largest real estate developers, suspended trading in 11 of its onshore bonds Monday, according to media reports. This raised concerns about another potential speed bump in China’s slower-than-expected recovery. China’s July Retail Sales are due early Tuesday (late Monday U.S. time), and analysts expect a rebound from June’s weakness.

Stocks in Spotlight

Big box week: As major retailers report, investors might want to hear about the impact on stores from record increases in credit card debt and the imminent return of student loan payments. Another question is whether discretionary spending held up in Q2.

One element possibly working in retailers’ favor is improved consumer sentiment seen in recent data. That, along with low unemployment, might help sector earnings bounce back from mixed results in the previous quarter. Slowing inflation growth could also be a tailwind.

Things kick off before Tuesday’s open with Home Depot HD. The home-improvement chain’s fortunes remain closely tied to the current interest rate environment, with the 30-year mortgage rate still above 7%, according to the Mortgage Bankers Association.

Home Depot’s previous earnings report in May might be one the company would rather forget. It missed Wall Street’s revenue expectations, lowered guidance, and said shoppers were delaying large projects and buying fewer big-ticket items, CNBC reported then. The company also cited poor weather and falling lumber prices (which didn’t bounce back this summer).

Also on the corporate side, Tesla TSLA cut prices in China, Bloomberg reported. That put pressure on automobile stocks and raised more questions about China’s economy.

What to Watch

Step to the counter: No major economic data is expected today, but tomorrow the U.S. government will release its July Retail Sales report before the open. Last week’s Federal Reserve data showing rising Q2 credit card balances burnished ideas that retail spending may be on the upswing. Stronger consumer sentiment in recent reports, including last Friday’s, reinforced impressions of consumer health.

Analysts expect monthly Retail Sales growth of 0.4% overall and stripping out automobiles, according to Trading Economics. That would be up from 0.2% for both in June. The data don’t take inflation into account, meaning some of July’s gain could reflect higher gas prices that month. Still, this would be the fourth straight monthly rise in retail spending if analysts are correct.

It’s a busy data week even after Retail Sales. Wednesday features minutes from the last Federal Open Market Committee (FOMC) meeting, along with July Housing Starts and Building Permits. There are also some U.S. Treasury auctions scheduled today. Recent auctions have put pressure on Treasuries, causing yields to rise.

Eye on the Fed

Futures trading indicates an 9% probability that the FOMC will raise interest rates by 25 basis points next month, according to the CME FedWatch Tool. The probability of rates being 25 basis points higher than they are now after the November meeting is near 38%.

FOMC Minutes Wednesday afternoon will likely get a close look from investors. The FOMC’s decision to raise rates 25 basis points was unanimous, but it’s possible the minutes could shed light on any debate about whether to raise rates again later this year.

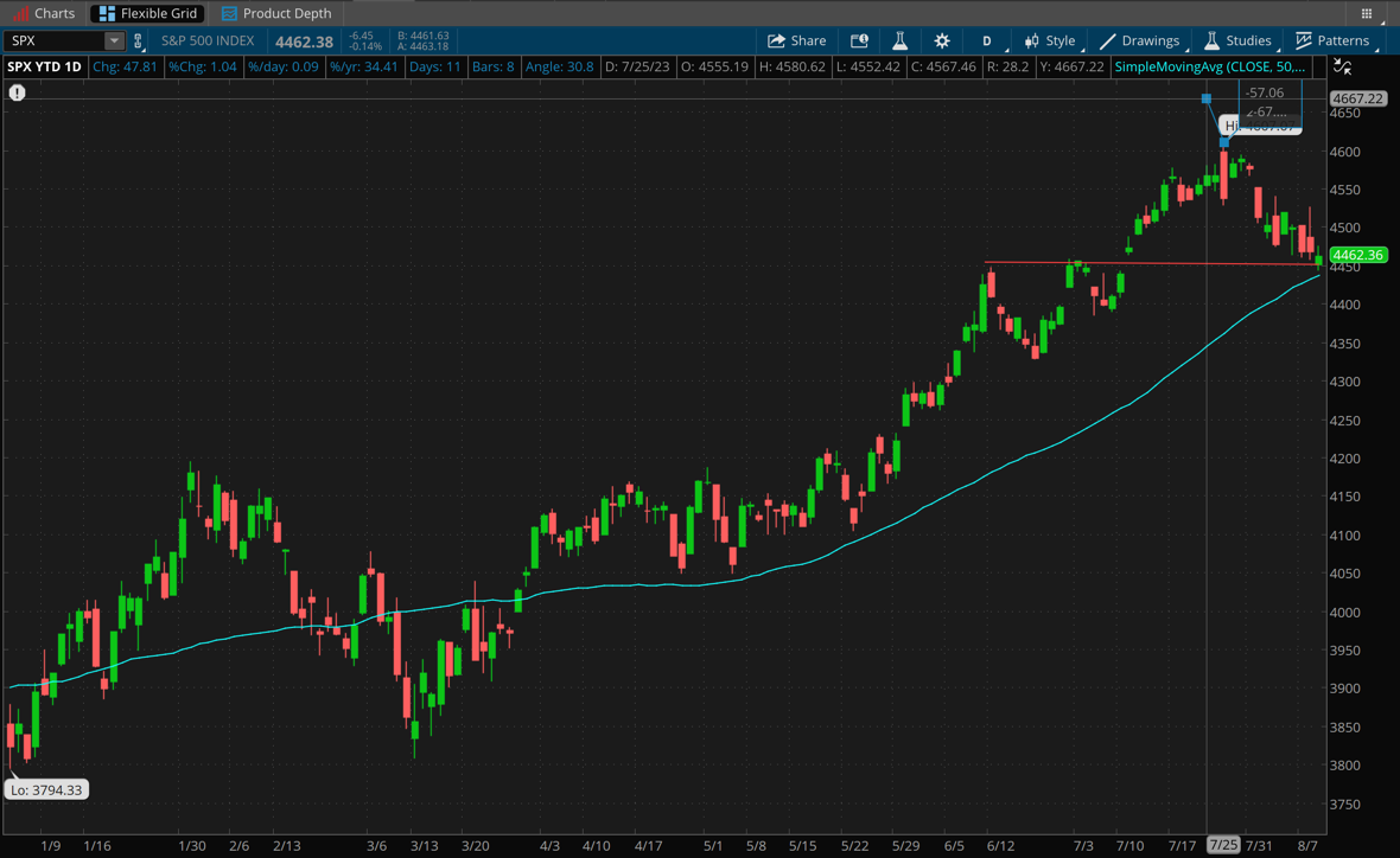

Talking Technicals: The 20-day moving average (MA) near 4,530 is a technical level to watch for the S&P 500® Index (SPX). Potential technical support is near 4,450 and below that at the 50-day MA near 4,438. The tech-heavy Nasdaq 100 (NDX) broke below its 50-day MA on Friday—the first major index to do that.

CHART OF THE DAY: WEDGE SHOT. The S&P 500 Index (SPX—candlesticks) is now tracking in a very narrow range between technical support at the 4,450 level (red line) where it bumped its head earlier this summer and resistance above 4,530 near the 20-day moving average. If 4,450 is breached on a move downward, the 50-day moving average (blue line) sits just under 4,440 and has been a support point for months, but will it hold again? Data source: S&P Dow Jones Indices. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Thinking cap

Ideas to mull as you trade or invest

Stick the landing: Friday’s July Producer Price Index (PPI) report threw a bit of a wrench into the “soft landing” scenario. It was above Wall Street’s expectations, with 0.3% monthly growth in both headline and core PPI (which strips out food and energy) for July versus the 0.2% average estimate. Both numbers also rose from June—an unwelcome sign for bulls that inflation can also trend higher, not just lower as it has most of the year. Fresh gains in the services sector helped accelerate PPI in July. The initial market reaction on Friday was a continuation of the week’s pattern where stocks moved lower and Treasury yields rose. However, the initial decline in stocks found buyers, perhaps in part because elements of the core PPI’s increase in July appeared to be possible one-timers. This could make the August PPI report even more important, helping confirm whether the slight July PPI boost was transitory. A better-than-expected preliminary August Consumer Sentiment report from the University of Michigan later on Friday also provided Wall Street a bit of support. The report showed lower inflation expectations, a welcome development. Remember, though, that higher PPI often takes time to trickle down to consumers.

Yield the floor: Treasuries arguably called the shots last week. Thursday’s early rally, for instance, turned tail midday when Treasuries plunged and yields (which move opposite of the underlying note) skyrocketed. The same dynamic could hold true this week, with many investors cautiously eyeing a 10-year Treasury note yield near 2023 highs. Moves above 4.1% in the 10-year yield appeared to rattle stocks late last week, and anxiety could mount if the yield approaches its 2023 high of 4.206%. The 9-month high yield from last November near 4.23% is another level to watch, while the 2022 high of 4.33% looms above. Any move above that and you’re talking about territory last reached more than 15 years ago. Higher yields typically mean rising borrowing costs for consumers and corporations, and often hurt growth-oriented companies in sectors like energy, housing, biotech, and information technology, which depend more on easy access to capital. Higher yields can also hurt “defensive” sectors like utilities and health care, offering investors yields that compete with dividends.

Competition mounts: Price-earnings is one way to figure out how expensive stocks are historically. Another is to check the spread between the stock market’s earnings yield (the inverse of price-earnings, or P/E) and the 10-year Treasury note yield. The S&P 500 earnings yield was 4.59% as of last week, according to Bloomberg, down from well above 5% a year ago as earnings growth slowed (earnings yield is calculated by dividing earnings per share by the stock price). The 10-Year Treasury note yield recently was 4.1%, up from around 2% when the Fed hiked beginning in March 2022. This means the gap has closed quite a bit, “This is crucial because it shows another way in which equities look expensive,” says Kevin Gordon, senior investment strategist at the Schwab Center for Financial Research. “For a considerable period of time when yields were pinned lower, equities always looked attractive to the bulls who relied on this metric. That is no longer the case; bonds are now giving stocks a run for their money.” Or to put it another way, the era of TINA (There Is No Alternative) could be over, for now.

Calendar

Aug. 15: July Retail Sales, August Empire State Manufacturing, and expected earnings from Cardinal Health (CAH) and Home Depot (HD).

Aug. 16: July Housing Starts and Building Permits and expected earnings from Target (TGT) and Cisco (CSCO).

Aug. 17: July Leading Economic Indicators and expected earnings from Walmart (WMT), Applied Materials (AMAT), and Ross Stores (ROSS).

Aug. 18: Expected earnings from Deere (DE) and Estee Lauder (EL).

Aug. 21: Expected earnings from Zoom Video (ZM).

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post was authored by an external contributor and does not represent Benzinga's opinions and has not been edited for content. This contains sponsored content and is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.