(Tuesday market open) Inflation isn’t giving up easy, rising moderately in January and likely further reinforcing the Federal Reserve’s rate hike plans. Investors didn’t show much love for the January Consumer Price Index (CPI) data, initially sending stock index futures lower.

CPI rose 0.5% month over month and core CPI rose 0.4%. That was roughly in line with Wall Street’s forecasts but still moderate growth from a historic standpoint. Analysts had expected CPI to climb 0.4% month over month and core CPI to rise 0.4%, according to a Reuters survey.

The data felt like a mixed bag. Investors will probably cheer the core monthly number coming in as expected, but some “sticky” inflation items like food away from home, recreation, and furnishings kept rising faster than forecast. On the plus side, used car prices kept falling, and so did medical services.

It’ll be interesting to see how Wall Street digests these numbers throughout the day because even though headline came in as expected, individual line items are all over the place. The overall report didn’t really land in one camp or another. Keep an eye on the CME FedWatch Tool today to see how the futures market thinks the data might affect rates.

In other news today, changes are afoot at the Fed. President Biden has decided to name Fed Vice Chair Lael Brainard as his top economic adviser, according to Bloomberg. An announcement could come as soon as today and raises another question—who will fill Brainard’s position at the central bank?

Morning rush

- The 10-year Treasury yield (TNX) was down 3 basis points at 3.68%.

- The U.S. Dollar Index ($DXY) fell to 102.86.

- Cboe Volatility Index® (VIX) futures slipped to 19.36.

- WTI Crude Oil (/CL) was near steady at $78.97 per barrel.

Stocks in spotlight

- Coca-Cola KO poured investors a cool glass of earnings this morning, coming in right as expected on earnings per share (EPS) and beating Wall Street’s revenue estimates. It even had some operating margin improvement, something good to see in the current environment where many companies find their margins under stress.

- While KO’s guidance also was above expectations, the company continues to struggle with currency headwinds despite the dollar’s recent retreat. There’s also the question dogging most consumer products companies right now: How much pricing power do they still have after the last two years of inflation? Some consumer-facing customers like supermarkets and restaurants have asked suppliers not to raise prices further because they don’t feel they can pass those higher costs along to their customers.

- KO shares rose about 1% in premarket trading, which was nice enough but couldn’t compete with 16% premarket gains for data-analytics software firm Palantir PLTR, which reported its first profitable quarter late Monday. PLTR expects to stay profitable through 2023.

- Cisco CSCO is one to watch tomorrow afternoon. Like many info tech stocks, CSCO shares racked up some nice gains since bottoming last fall but haven’t gained the traction to take out last summer’s highs. The company is normally a good bellwether for tech industry health in general because its components go into so many pieces of the puzzle.

- Another one to watch is Airbnb ABNB after today’s close to see if the travel surge has started to sag. Shopify SHOP is expected late Wednesday. SHOP struggled with a strong U.S. dollar in its last earnings report, but dollar strength has dissipated since then. No guarantee that represented a tailwind, but we’ll find out tomorrow.

What to watch

There’s no break from the data this week. After today’s CPI figures, January Retail Sales arrive tomorrow.

Last month’s Retail Sales report was a real downer on Wall Street after a poor December reading. It was one of the first times in recent months in which the market treated bad news as bad news instead of rallying on hopes of a Fed pause. Some believe December’s data suggests a return to more normal market behavior now that rates are nearing the Fed’s peak projection of slightly above 5%.

If the same sentiment holds for January’s retail numbers, it’s possible the market could get a boost. A huge month-over-month increase of 1.7% is the consensus on Wall Street, according to Briefing.com, the first rise since October. Much of that forecast reflects an anticipated rebound in auto sales, which slumped in December. Without autos, analysts expect a 0.8% bump in January Retail Sales, still a good showing. However, a rise in gas prices during January might be reflected in tomorrow’s data.

One more category worth watching is home furnishing and furniture store sales, which crumbed more than 2% in December. A better showing might reflect improvement in the housing market.

Speaking of which, January Housing Starts and Building Permits are due Thursday. We’ll preview the forecast numbers here tomorrow.

That housing report might be overshadowed early Thursday by the January Producer Price Index (PPI). Then Friday morning provides a look into import/export prices and the Conference Board’s Leading Economic Indicators. With all this data and a still decent-sized menu of earnings, investors will probably want to stay on their toes all week.

Market minutes

Here’s how the major indexes performed Monday:

- The Dow Jones Industrial Average® ($DJI) climbed 376 points, or 1.11%, to 34,245.

- The Nasdaq Composite® ($COMP) rose 1.48% to 11,891.

- The Russell 2000® (RUT) climbed 1.16% to 1,941.

- The S&P 500 index (SPX) increased 46 points, or 1.14%, to 4,137.

Wall Street is knocking on the door of recent closing highs, except for the RUT. Its recent struggles put it about 3% below the early February peak.

- Major indexes strained the reins right out of the starting gate Monday and never slowed down. In fact, they closed near their highs for the day, led by mega-cap info tech companies like Microsoft (MSFT), Meta Platforms (META), Apple (AAPL), and Nvidia (NVDA). MSFT shares got a lift from an upgrade that followed a series of recent target-price increases in the wake of its artificial intelligence/search-related announcement from last week. META appeared to attract buyers with its recent cost-cutting moves.

- Big tech made a big splash Monday but didn’t stand alone. Homebuilder stocks, along with other home-related companies like Home Depot (HD) and Lowe’s (LOW), also pulled ahead. So did some consumer staples subsectors like personal care products. It was a broad-based rally that included every sector besides energy, but growth areas led the scorecard. It’s a bit odd to see housing-related stocks attract so much buying interest even as 30-year mortgage rates climb from recent lows.

- It also may seem odd that Wall Street put on its party hat Monday even though volatility initially climbed ahead of today’s CPI report. One idea could be that the bond market has now built in higher rates. Last week’s 1% SPX decline could’ve partly reflected bond yields catching up to Fed rate projections. Now that the Fed and the market are better aligned, perhaps some investors think that puts the market on better footing.

Talking technicals: Another explanation for Monday’s rally goes back to the technical situation we described yesterday morning. The SPX bounced off a support area between 4,075 and 4,080 on Friday after never really testing support below that near 4,050 during last week’s slide. The positive market action late Friday might’ve simply spilled into Monday and gained more traction when the SPX rallied past 4,100, which could’ve triggered the short covering. While that’s technically positive, recent attempts to climb above 4,150 have regularly failed. That area remains a tough resistance marker.

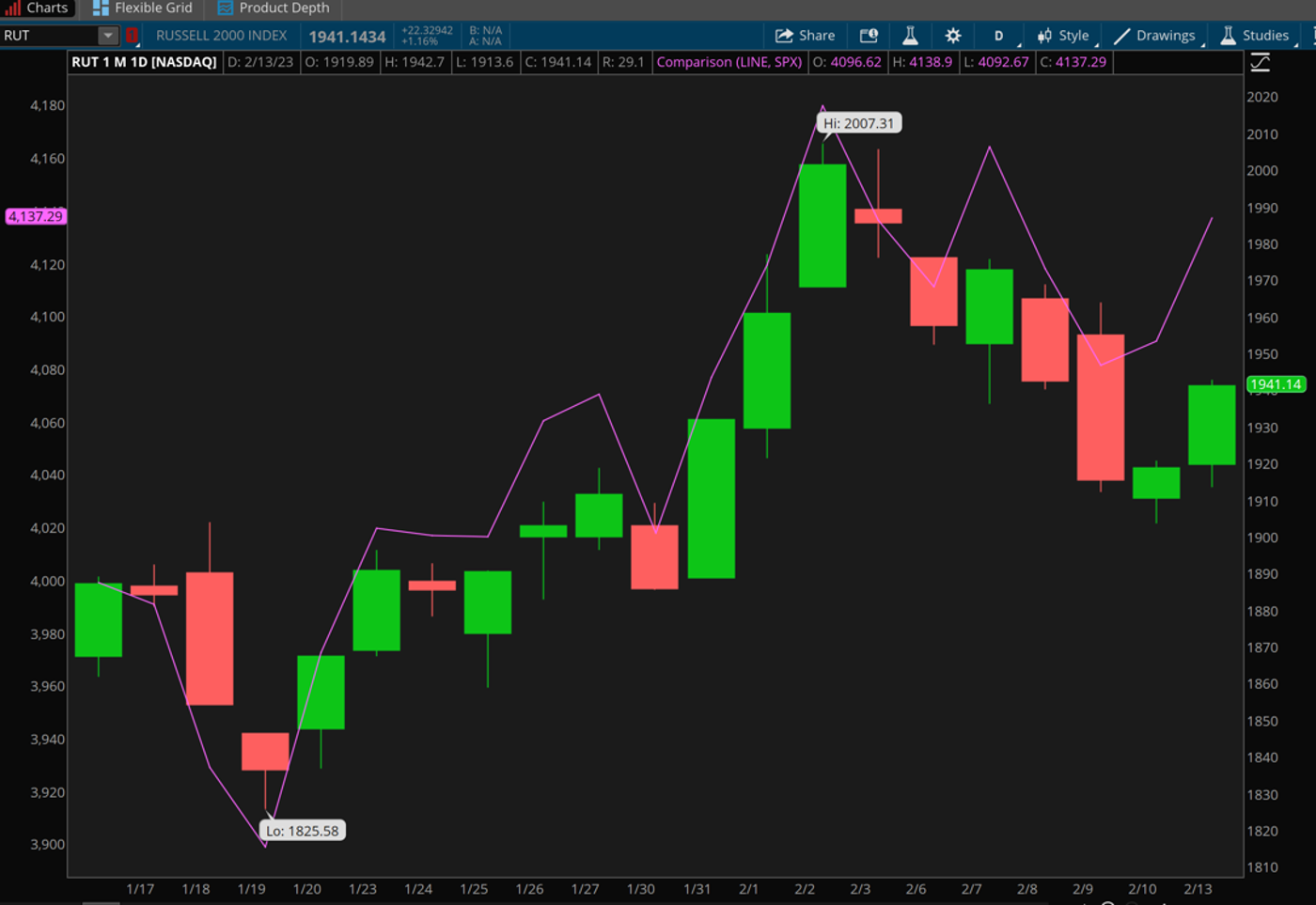

CHART OF THE DAY: LESS LOVE FOR SMALL-CAPS. As the market bounced back Monday from last week’s softness, the S&P 500 index (SPX—purple line) finished much closer to recent highs than the Russell 2000 (RUT—candlesticks). This is evidence that the rebound is being led by large-caps and that small-caps continue to struggle. Data sources: S&P Dow Jones Indices, FTSE Russell. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Thinking Cap

Room to rise: Today’s CPI data comes after a quick 30-basis-point rally in the 10-year Treasury yield over the last two weeks as market participants sensed more rate hikes ahead. That yield climb may not be over, especially if data continue suggesting the Fed has additional inflation fighting to do, wrote Charles Schwab Chief Fixed Income Strategist Kathy Jones. Treasuries rallied early this year and yields—which move the opposite direction—dove as investors anticipated slowing economic growth and progress with inflation. That helped lead to a major gap between where the Fed projected rates to go (quite a bit higher) and where the market saw rates heading (well below the Fed’s projection). Starting with a much better-than-expected January employment report, that idea began to lose credibility, and the gap between the market and the Fed pretty much closed. Jones sees “nominal” levels for the 10-year yield of between 3.75% and 4% and doesn’t think the Fed will get any more dovish with its projections at next month’s meeting. Does Monday’s Wall Street rally in the face of recent rising bond yields reflect a stock market that’s ready to take higher rates in stride? Too early to say.

Euro, pound keep pace: While the dollar has shown signs of strength recently, so have the euro and pound. This partly reflects ideas that the Bank of England (BoE) and European Central Bank (ECB) have been slow keeping up with the Fed’s rate hikes and may be under pressure to make more dramatic moves, Barron’s recently noted. Both the BoE and the ECB raised rates by a half-point in February, and the ECB has promised another bigger-than-usual move in March. Strength in European currencies, of course, implies more robust economies across the pond, as European stocks so far this year are up nearly 8% versus only 6.5% for the SPX. The euro recently hit $1.08 after sinking to parity with the dollar, and the pound is above $1.20 after its recent multi-year lows near $1.03.

European vacation: Continued European currency strength remains a bit dependent on the Fed lifting the brake pedal a bit in coming months, Barron’s added. Even if the Fed remains aggressive, however, the forex situation might have some investors seeking U.S. stocks with exposure to Europe. That’s ironic considering just a year ago—when Russia invaded Ukraine and energy prices soared—investors were contemplating how to avoid European risk. If you’re wondering which U.S. industries have heavy European exposure, think travel, cosmetics, agricultural, and food processing. Obviously, anyone who’s really bullish about Europe could simply buy European stocks or funds that invest in Europe. However, before taking a trip across the Atlantic, keep in mind the risks that remain. They include the ongoing war in Ukraine, rising European rates, and any potential challenges China encounters as it reopens. Europe’s economy has heavy export exposure to China, particularly in manufacturing. A speed bump in China—whether it’s political or pandemic-related—could mean a potential stall for economies like Germany and the U.K.

Notable calendar items

Feb. 15: January Retail Sales, January Capacity Utilization and Industrial Production, and expected earnings from Biogen (BIIB), Cisco (CSCO), and Kraft Heinz (KHC)

Feb. 16: January Housing Starts and Building Permits, January Producer Price Index (PPI), and expected earnings from Entergy (ETR), Hasbro (HAS), and Hyatt Hotels (H)

Feb. 17: January Import and Export Prices, January Leading Indicators, and expected earnings from Deere (DE)

Feb. 20: Presidents Day (market holiday)

Feb. 21: January Existing Home Sales and expected earnings from Home Depot (HD) and Medtronic (MDT)

Feb. 22: MBA Weekly Mortgage Applications Index and expected earnings from TJX (TJX) and Baidu (BIDU)

Feb. 23: Q4 Gross Domestic Product (GDP) second estimate and expected earnings from Alibaba (BABA) and PG&E (PCE)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.