Key Takeaways:

- Investors might closely watch how much banks put aside for possible credit defaults

- Heavy trading volume could help Q2 earnings for some banks, including MS

- Investors will be listening closely for executives’ latest economic outlooks

If the financial sector is one of the best barometers of investor sentiment regarding the economy, then it seems we’re far from out of the woods. That’s despite the broader market rally and strong trading activity the big banks likely pulled in this last quarter.

You can see that in the performance of Financials throughout Q2. After a brief flurry of buying in late May, the sector got the wind knocked out of it and trails the broad S&P 500 Index (SPX) dramatically over the last month. Financials inched up 9% over the last three months compared with nearly 20% gains for the SPX.

It’s also evident in analysts’ predictions for Q2 performance from some of the biggest banks reporting later this week. Estimates are down across the board for year-over-year earnings. Wednesday brings Goldman Sachs Group Inc GS, followed Thursday by Morgan Stanley MS and Bank of America Corp BAC.

So what’s happening? Well, partly it’s because investors have tied in the big banks’ fortunes with sagging Treasury yields. When yields had a brief rally in late May, it possibly raised hopes that banks could escape the world of low net interest margin they got thrown into when the Fed slashed rates to zero back in March. Those hopes didn’t last long, because a June swoon in the stock market was accompanied by 10-year yields scampering back down to near their 2020 lows, dashing any hopes that banks might see better profit margins anytime soon.

The 10-year Treasury yield recently traded near 0.65%, not far above the lows near 0.5% at the peak of the March market meltdown and well below the recent high of around 0.9% in early June. Low-interest rates tend to hurt banks’ profits.

The Fed itself might have poured salt on the industry’s wounds after its June meeting, when Fed Chairman Jerome Powell, in a press conference, said, “We’re not even thinking about thinking about raising rates.” Bank executives now are bracing for their margins to remain under pressure not only in 2020 and 2021 but possibly in 2022 as well, if the Fed’s forecasts end up being right.

All this—along with plenty of fundamental weakness we’ll get to below— is spinning through investors’ heads as they await earnings from the second troika of big banks reporting this week.

More Sector Suffering In Q2

Looking at the broader Financial sector beyond the biggest banks, most analysts predicted a rough Q2 and that looks like exactly what we’re going to get.

The Financials sector is expected to report the fourth largest year-over-year earnings decline of all 11 sectors in the S&P 500 at negative-51.5%, according to research firm FactSet. If earnings actually fall that steeply, it would be the worst performance for Financials since the bad old days of the financial crisis in late 2008.

The suffering isn’t necessarily spread through the Financial sector equally. Although all five industries in this sector are predicted to report a decline, FactSet predicts three of these five industries will report declines of more than 25%. These include consumer finance (-106%), banks (-69%), and insurance (-27%).

That parks banks right near the bottom, though the bank part of Financials isn’t monolithic. There are mega-banks like GS, MS, and BAC, and also smaller regional banks. The regionals have been hammered in trading lately, though a better mortgage environment might be helping ease the pain a little.

Trading Volume May Impress And IPOs Slowly Re-Emerge

Another thing that might ease the pain, at least for the biggest banks reporting this week, is trading volume. When markets rallied sharply from the late-March lows, it likely increased all sorts of market activity, including hedging and “buying the dip.” Several times in June, markets took a brief dive, only to see a flood of new buyers come in before any major damage could be done.

There was tremendous trading volume early in the rally for both fixed income and stocks, noted research firm Briefing.com, part of a “reflation trade” across capital markets. That, along with a lot of mortgage refinancing that accompanied lower rates, could have helped business for many of the big banks.

While volatility couldn’t sustain the crazy levels it reached during the market’s huge cratering in March, the Cboe Volatility Index (VIX) remained above 30 almost the entire Q2, suggesting that options markets were busy as investors anticipated more risk and choppiness ahead.

GS is second only to MS when it comes to the size of banks’ trading shops, so these two could be well-positioned. As was the case last quarter, investors should remember that If any bank misses on trading right now, their stock is likely to get decimated. However, trading isn’t monolithic. It’s possible some banks had good quarters in either stocks or fixed income, but not in both.

Also, while volatility can be good for banks’ trading desks, other business units tend to retract in times of market stress.

Another factor possibly in the banks’ favor this time around is a bit of an uptick recently in initial public offerings (IPO) and mergers and acquisitions (M&A) activity. Going into Q1 earnings season, this sort of business appeared locked down with the rest of the economy. As things started to reopen during Q2, companies started looking again at how to maximize their profits or at least stay above water with some of the activities like M&A that tend to help banks’ business.

Grocery company Albertsons Companies Inc ACI recently conducted an IPO and is now trading. So is Technology firm Accolade Inc ACCD and financial firm Lemonade Inc LMND. It’s good for the banks to see the ice melting a little in this part of their world. One thing to potentially listen for on their calls is how they see IPOs and M&A activity advancing from here, particularly with worries about more shutdowns in some states as COVID-19 cases grow.

With Businesses Still Suffering, Pressure Stays High

While trading is big for GS and MS, the heart of many banks is lending money and making a profit from the interest.

This bread and butter business might continue to struggle. Brooks Brothers just declared bankruptcy after more than 200 years in business. United Airlines Holdings UAL last week announced that 36,000 employees might have to be furloughed by Oct. 1 as demand remains low. Bed, Bath & Beyond Inc BBBY recently announced plans to close 200 stores. Everyone’s already heard about struggles in the cruise line industry, and other airlines also continue to suffer.

All this could spell trouble for banks, which took large provisions in Q1 against possible credit losses. One question heading into Q2 is whether they’ll expand these provisions as the economy keeps struggling. A big expansion of banks’ defense against possible losses might signal that they see more trouble ahead.

Another trouble spot could be the credit card and auto loan businesses, where banks might face many customers unable to pay their bills. “We expect there will be spikes in delinquencies and charge-offs that will eventually exceed the highs of the previous recession and that investors are not pricing in enough provision expenses,” research firm CFRA said in a recent note.

Also worth keeping an eye on is how the banks see their cash positions now and in the future. Laws passed in the wake of the 2008 financial crisis force banks to keep more money on hand than they used to, which might have helped this time around.

Despite so much weakness around the economy, GS, MS, and BAC passed their recent Fed “stress tests” with flying colors, and said they’ll maintain their current dividends. That was probably a relief for a lot of investors who may have had doubts about the dividends back when the crisis first hit.

However, another tool the banks use to keep investors happy is stock buybacks, and those have kind of gone out of style this year. With so many people out of work, it’s seen as politically unfeasible by many businesses, both in and out of the Financial industry, to use money for that or for executive bonuses. Although unlike back in the financial crisis, no one is blaming banks for the economy’s battering this time around, banks are probably going to be careful on the public relations front.

As BAC put it after the stress test: “Bank of America is committed to returning capital to shareholders over time, in excess of what is needed across economic cycles to grow the company and support clients, communities and the global economy.”

MS and GS both said after the stress tests that they remain strongly positioned financially and can afford to maintain their current dividend payouts.

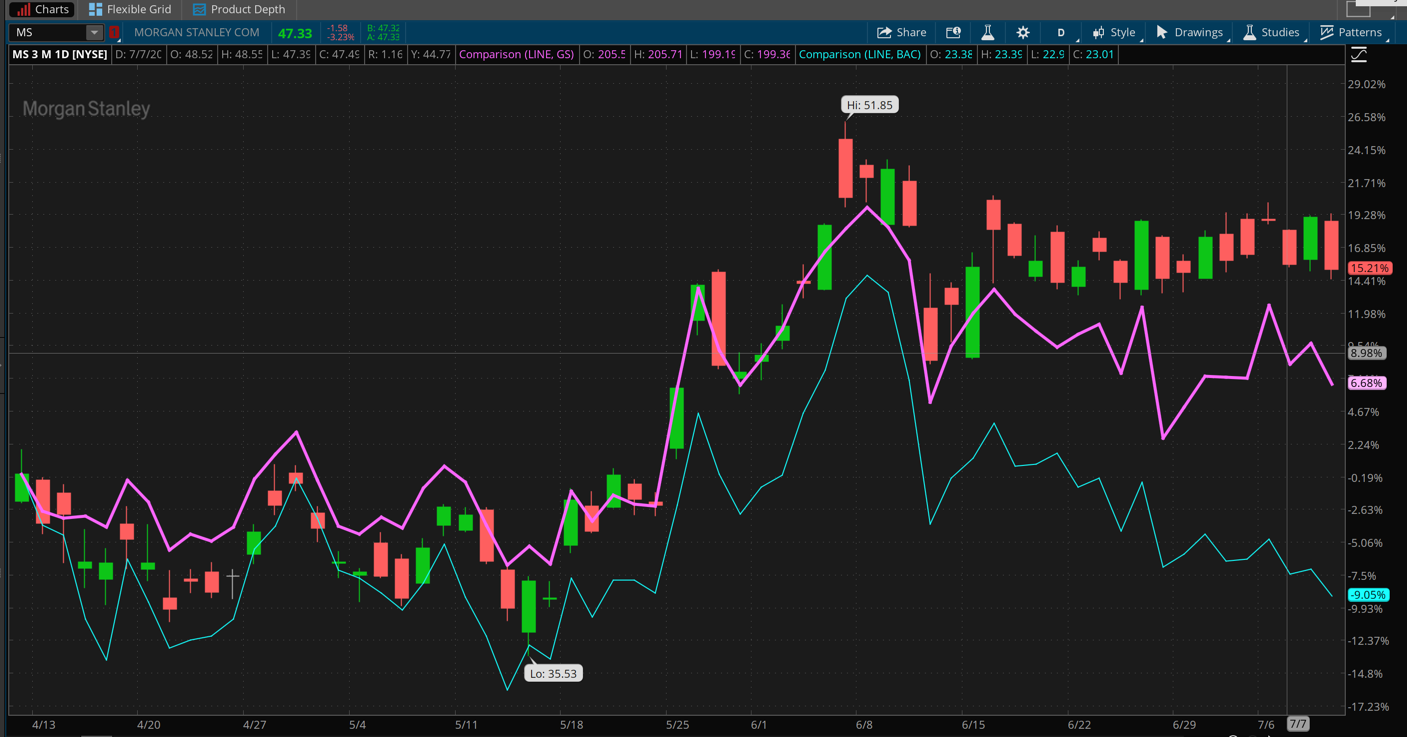

FIGURE 1: FLATTENING OUT. Shares of Morgan Stanley (MS—candlestick) and Goldman Sachs (GS—purple line) have been holding relatively flat recently as these traditional big trading shops might benefit from all the volume of the last quarter. Bank of America shares (BAC—blue line), have been losing ground lately, maybe on worries about how its biggest division, consumer banking, might be positioned as the pandemic unfolds. Data source: NYSE. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

BAC has a huge consumer banking business, which might have gotten some traction in May and early June as the economy began reopening. It’s only in the last few weeks when things started to go backward in some states, meaning it’s possible the pressure won’t show up until the Q3 books get opened. However, shares have been lagging lately, maybe amid fears of how consumers are situated as unemployment and new jobless claims both remain high.

Wealth management is a key business for MS, and while many investors probably got hit hard by the March market crisis, they may have been feeling more enthusiastic by late in Q2 as the stock market revived. Also, anytime you have big market swings, it tends to get people more nervous, potentially leading to more demand for wealth management services.

With MS, it’s important to keep a close eye on trading results, and also to see if the company feels it’s making strides in its growing IPO business.

GS, like MS, has a huge trading business. We’ll be looking for results out of that and for any different outcomes between the fixed income and equity sides of the quarter.

Bank Of America Earnings And Options Activity

When BAC releases results, it is expected to report adjusted EPS of $0.27, vs. $0.74 in the prior-year quarter, on revenue of $22.01 billion, according to third-party consensus analyst estimates. Revenue is expected to drop 5.3% year-over-year.

Options traders have priced in a 4.7% stock move in either direction around the upcoming earnings release, according to the Market Maker Move indicator on the thinkorswim® platform from TD Ameritrade. Implied volatility was at the 25th percentile as of Tuesday morning.

Looking at the July 17 options expiration, there’s been a bit of activity to the downside, particularly at the 22 and 22.5 strikes. But a lot of the activity has been to the upside, with concentrations in the 25- and 26-strike calls.

Note: Call options represent the right, but not the obligation, to buy the underlying security at a predetermined price over a set period of time. Put options represent the right, but not the obligation to sell the underlying security at a predetermined price over a set period of time.

Goldman Sachs Earnings And Options Activity

GS is expected to report adjusted EPS of $3.70, vs. $5.81 in the prior-year quarter, on revenue of $9.73 billion, according to third-party consensus analyst estimates. Revenue is expected to be up 2.9% year-over-year.

Options traders have priced in a 5.3% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator on the thinkorswim platform. Implied volatility was at the 28th percentile as of Tuesday morning.

Looking at the July 17 expiration, put activity has been light overall, with some activity at the 190 and 195 strikes. Calls have seen more activity, with concentrations at the 220 and 225 strikes.

Morgan Stanley Earnings And Options Activity

MS is expected to report adjusted EPS of $1.10 vs. $1.23 in the prior-year quarter, on revenue of $10.31 billion, according to third-party consensus analyst estimates. Revenue is expected to be roughly flat year-over-year.

Options traders have priced in a 4.6% stock move in either direction around the coming earnings release, according to the Market Maker Move indicator. Implied volatility was at the 28th percentile as of Tuesday morning.

Recent call activity has been noted at the 52 strike, while puts have been active at the 46 and 50 strikes.

TD Ameritrade® commentary for educational purposes only. Member SIPC. Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options.

Photo by Getty Images.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.