With the threat of an unsecure retirement becoming increasingly more eminent as the oldest generation keeps getting older and the average time spent in retirement likewise increasing, many lose sight of the basics.

It is undeniable that retirement security funded solely from the government is likely to disappoint in the decades to come. However, prudent financial strategies can help combat the potential uncomfortable situation.

What Is The Social Security Situation Really?

As explained by Drew Desilver, Pew Research Center senior writer, the complexities of Social Security are innumerable (from a 29-page document in 1935 to the almost 2,600 page current law), but the growing fear is quite possibly more detrimental than the reality.

- The Inter-Generational Transfer: "The taxes paid by today's workers and their employers don't go into dedicated individual accounts […] Nor do Social Security checks represent a return on invested capital […] Rather, the benefits received by today's retirees are funded by the taxes paid by today's workers; when those workers retire, their benefits will be paid for by the next generation of workers' taxes."

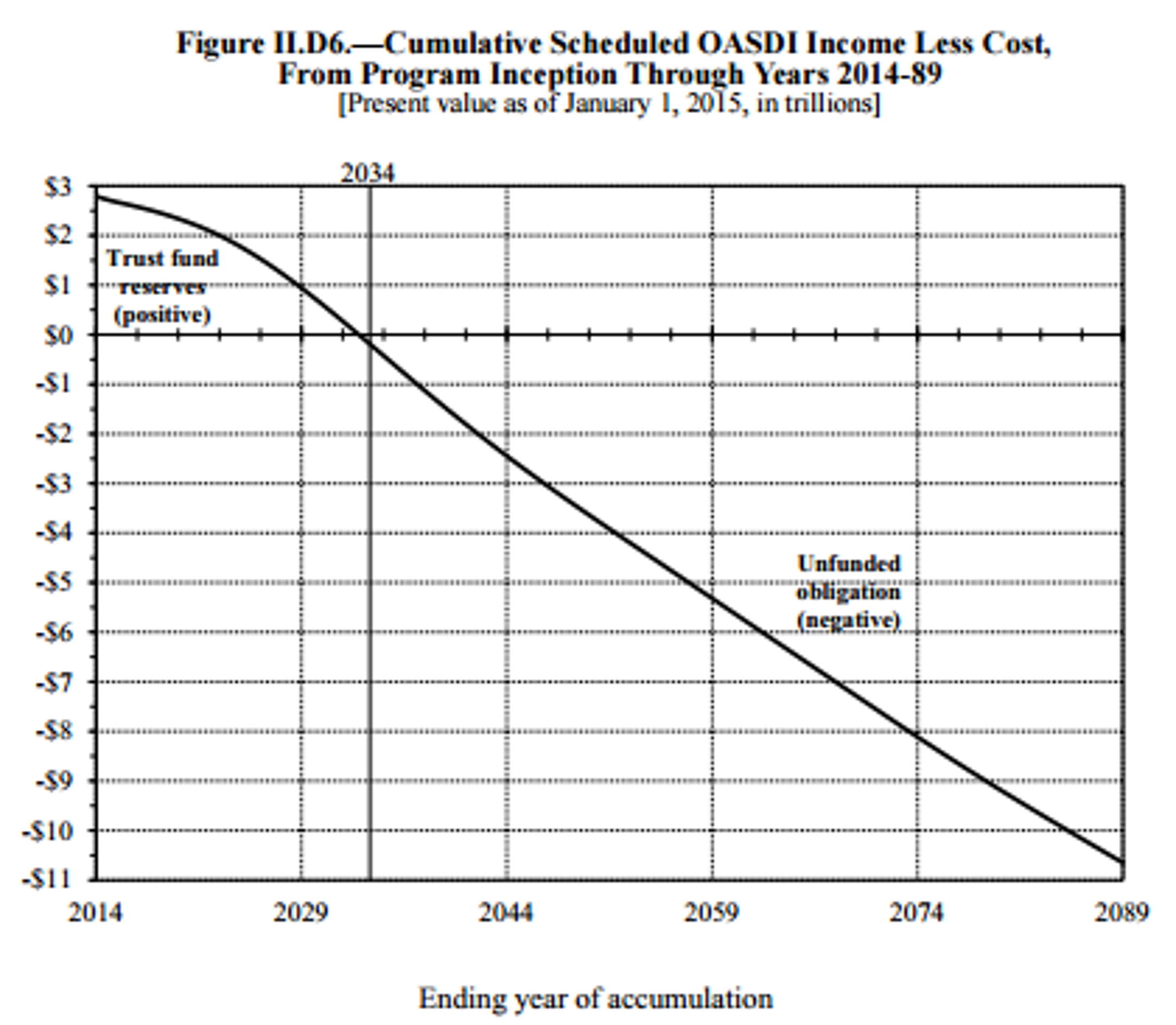

- Currently, SS Assets Are Comfortable: "Right now, Social Security has plenty of assets. For much of its history, Social Security was a strictly pay-as-you go system, with current tax receipts funding current benefits. That changed in 1983, when Congress (as part of a comprehensive overhaul of the program) raised the payroll taxes that provide the bulk of Social Security's revenue, to build up a cushion for the coming onslaught of Baby Boomer retirees. For nearly three decades, the system took in far more revenue than it paid out in benefits; the surplus was invested in special non-tradeable Treasury bonds, with interest credited to the system's two trust funds."

- In The Last 5 Years, The Expenses Have Gone Above The Cash Receipts: "Negative cash flow last year was about $74 billion […] and this year the gap is projected to be around $84 billion. While the credited interest on all those Treasuries is still more than enough to cover the shortfall, that will only be true until 2020. After that, Social Security will begin redeeming its hoard of Treasuries for cash to continue paying benefits – as was the plan all along."

- Reserves' Full Depletion By 2013: "The exact depletion dates depend, of course, on future demographic and economic trends. After the reserves are exhausted, the system still will be receiving tax revenue, but it will only be enough to pay about three quarters of scheduled benefits – unless Congress changes the benefit formulas, raises the payroll tax, or makes other changes such as raising the cap on taxable wage income."

So, What Is One To Do?

While it is highly probable that Congress will step in and make the necessary changes to the payroll tax, benefit formulas or other strategies to counter the depletion, there are things each individual can do before retirement to ensure that regardless of the government's involvement, those years after employment are well funded.

1. Take Advantage Of 401(k)s, Roth/Traditional IRAs Or EquivalentAbove all, remember that you are in control over your financial future. Do not wait to see if and how the government will provide for you in late-adulthood. Be proactive and embrace the fact that your financial security is ultimately your responsibility. Take control today and reach out to a financial advisor if you need assistance or guidance. Ultimately, it's up to you to take care of yourself.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.