(Wednesday market open) The economy refuses to slow down, which could be good news for the market but presents more challenges for the Federal Reserve.

Today’s January Retail Sales report showed a massive spike of 3%, well above the 1.7% consensus. Even with the volatile auto sector stripped out, sales climbed 2.3% versus Wall Street’s expected 0.8%. Stock index futures slightly extended earlier losses after the data came out and Treasury yields jumped.

Inflation and rate concerns remain front and center after yesterday’s January Consumer Price Index (CPI) data and ahead of tomorrow’s Producer Price Index (PPI) report. Data out of the U.K. this morning showed mixed progress in that country’s inflation battle, with consumer prices still up by double-digits year over year but falling more than expected month over month in January.

Yesterday’s CPI data helped lead to a wild Tuesday on Wall Street that ended with the S&P 500® index (SPX) still just below recent highs. This puts stock valuations at relatively lofty levels versus where they’ve been the last six months and could mean choppy trading ahead. However, volatility was muted by Wednesday morning.

Just in

January’s sizzling Retail Sales report isn’t the kind of data you see in a cooling economy.

Some of the same “sticky” inflation categories that rose in yesterday’s CPI report were furnishings and meals outside of the home, and those powered January Retail Sales as well. This shows a very strong consumer out there, and suggests the Fed has a lot of work to do. Chances of a 50-basis point March hike initially ticked higher—to 12% from 9%—on the CME FedWatch Tool this morning.

Stock index futures haven’t slipped much on the news. That could be because there’s a pretty strong element out there that sees inflation coming down without a significant economic slowdown. This group of market participants is OK with strong economic data as long as inflation continues to moderate, which it did in a very slight way during January.

Morning rush

- The 10-year Treasury note yield (TNX) jumped 2 basis points to 3.78%.

- The U.S. Dollar Index ($DXY) jumped to 103.69.

- Cboe Volatility Index® (VIX) futures slipped to 19.09.

- WTI Crude Oil (/CL) traded slightly lower at $78.30 per barrel after a large increase in U.S. supply.

Stocks in spotlight

Cisco CSCO reports this afternoon. The digital communications company is normally a good bellwether for tech sector health in general, so its results and call need to be looked at closely. Investors reacted positively to CSCO’s most recent earnings report when it discussed job cuts and raised guidance. A potential tailwind in coming quarters could be easier comparisons to a relatively weak 2022.

If the economy can avoid a major recession, CSCO might face less risk of a slowdown in the enterprise infrastructure industry. Still, recent layoffs across tech speak to possible growth issues. It should be interesting to get CSCO executives’ take on demand for the networking, cloud, and cybersecurity products it offers.

Shopify SHOP is also expected to report this afternoon, and more big retail results are around the corner. In an interview on CNBC Tuesday morning, Bank of America BAC CEO Brian Moynihan was upbeat about consumer health, noting the strong labor market. Did that translate into better revenue for major retailers? Look below for more from BAC on consumer spending.

Airbnb ABNB results late Tuesday looked solid as the company beat analysts’ estimates on the top and bottom lines and delivered a strong Q1 revenue forecast. The company’s pricing power held and helped drive revenue gains, though there are signs of prices leveling off. Shares rose nearly 9% in premarket trading. Other travel firms appear to be getting a corresponding boost.

What to watch

The data keep on coming this week, most of it pertinent if you’re actively trading. You can rest over the three-day holiday weekend (markets are closed Monday for Presidents Day).

Tomorrow morning brings two important data markers: January Housing Starts and Building Permits and the January Producer Price Index (PPI). We’ll take one at a time.

January PPI: Back in December, PPI retreated dramatically, falling 0.5% from November. Much of that, however, was due to soft energy prices, something that wasn’t the case in January. The core December PPI that strips out food and energy rose 0.1%, led by large gains in unprocessed goods prices.

Tomorrow’s report, due just before the open, is expected to show a 0.4% rise in headline PPI and a 0.3% increase in core PPI during January, according to consensus from Briefing.com. PPI data are worth watching to see if companies are getting any reprieve from high input costs. So from a corporate earnings perspective, a soft number would be seen as helpful.

January Housing Starts/Building Permits: Housing starts have declined every month since August. Permits began falling in September. The two metrics slipped 1.4% and 1.6% respectively in December.

The slide in permits is expected to end in January, with consensus from Briefing.com for a seasonally adjusted 1.35 million, up from December’s 1.33 million. But the skid in starts is forecast to continue, falling to a seasonally adjusted 1.355 million in January from 1.382 million in December.

Falling starts and permits could worsen a housing shortage that’s been felt hardest in lower-priced starter homes. With interest rates now up again and lumber prices recently rising fast, the housing industry could continue to struggle despite the healthy labor market.

Numbers to know

87.8%: The CME FedWatch Tool projects this probability of a quarter-point Fed rate hike in March, bringing the Fed’s target rate to between 4.75% and 5%. There’s now a 12% probability priced in that the Fed could go up 50 basis points in March. If the Fed starts hinting at a 50-basis-point rise, it could likely be a psychological blow for market participants who’ve built in expectations that the Fed will make smaller rate hikes after four consecutive 75-basis-point increases in 2022.

4.1%: The FedWatch Tool’s probability of rates pausing at 4.75% to 5%. Yesterday’s January CPI report and the January Nonfarm Payrolls data dashed any hopes that it’d be one more and then a pause from the Fed.

5.50% – 6%: Chances that the Fed’s target range could be this high as soon as its late July meeting. The tool puts odds around 20% of rates rising to these levels, far above the Fed’s current terminal, or peak, projection of between 5% and 5.25%.

After Tuesday’s CPI data, the first Fed officials to speak sounded resolute. Richmond Fed President Thomas Barkin told Bloomberg, “If inflation persists at levels well above our target, maybe we’ll have to do more.”

Dallas Fed President Lorie Logan said: “We must remain prepared to continue rate increases for a longer period than previously anticipated,” Bloomberg reported.

That wasn’t the final word from the Fed on Tuesday, and the market took note. Philadelphia President Patrick Harker said that policymakers were nearing the point where rates were restrictive enough: “In my view, we are not done yet … but we are likely close,” Bloomberg reported. That may have eased the market’s fears, helping lift indexes from lows.

Cleveland Fed President Loretta Mester speaks today. She’s generally considered one of the more hawkish Fed presidents.

Market minutes

Here’s how the major indexes performed Tuesday:

- The Dow Jones Industrial Average® ($DJI) fell 156 points, or 0.46%, to 34,089.

- The Nasdaq Composite® ($COMP) rose 0.57% to 11,960.

- The Russell 2000® (RUT) inched 0.13% higher to 1,944.

- The SPX barely moved, dropping 1 point, or 0.03%, to 4,136.

The $COMP’s rise and the SPX’s rebound from midday lows (see chart below) on Tuesday speak to continued market resilience.

- Despite rising Treasury yields and hawkish Fed talk following CPI, Tuesday turned into a risk-on day for stocks as investors generally embraced growth sectors like consumer discretionary and info tech. Defensive sectors like utilities and health care didn’t perform well. Consumer discretionary and tech continue to be the best-performing sectors so far in 2023, and consumer companies like Nike (NKE) and Visa (V) were among the $DJI leaders Tuesday.

- Mega-cap stocks continue to do well, perhaps helped by investors looking for big, familiar names in a time of caution about the rate picture. Travel stocks and semiconductors also had good days Tuesday.

Talking technicals: Tuesday saw the 10-year Treasury note yield (TNX) post its highest intraday level since December, closing in on 3.8%. The TNX recently pushed through a downtrending line on the charts, possibly providing a tailwind that could continue supporting this rally.

Geopolitics and the market: Does recent news about flying objects have you worried about the potential market impact? Charles Schwab’s Chief Global Investment Strategist Jeffrey Kleintop breaks down geopolitical risk factors in his latest report.

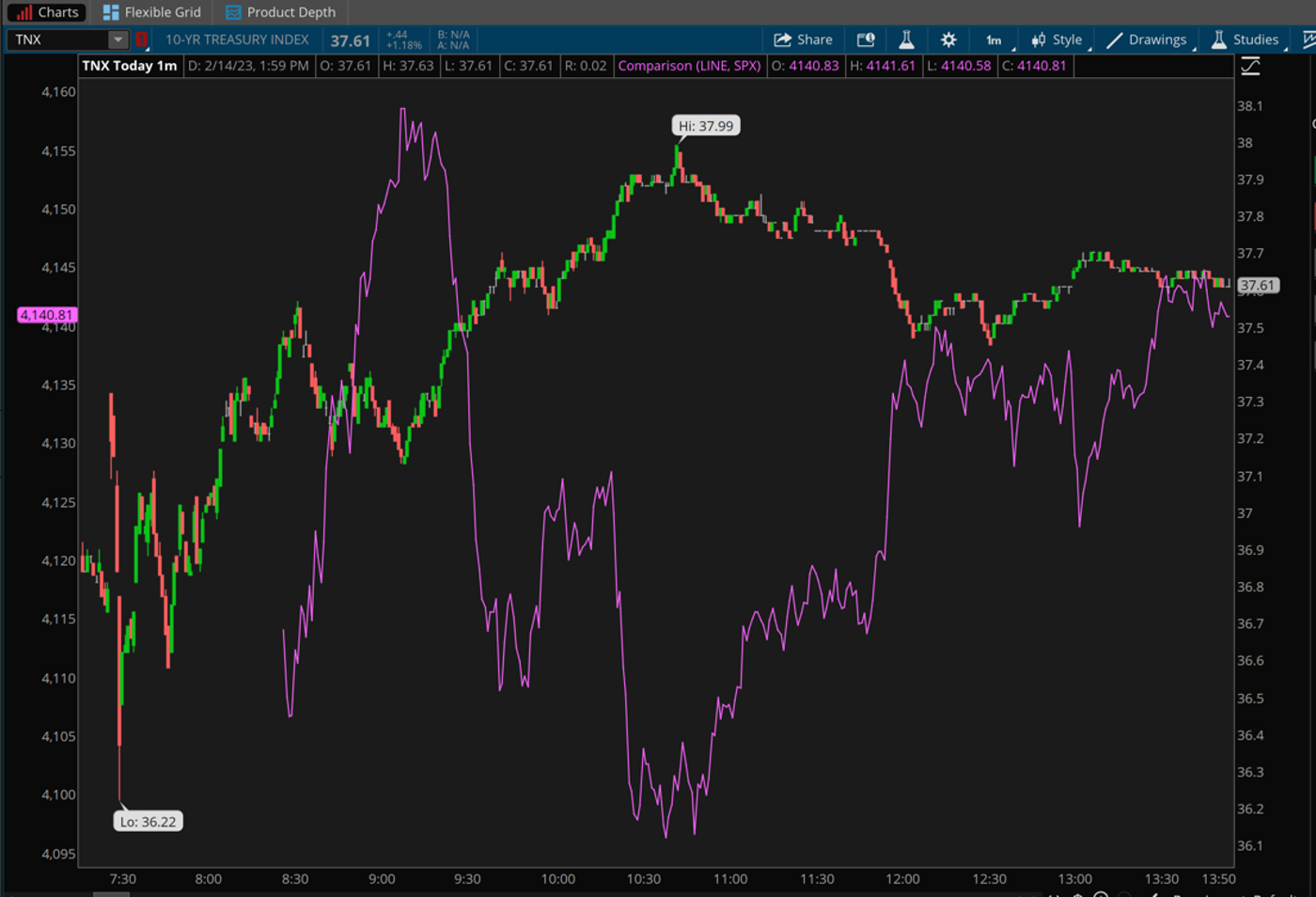

CHART OF THE DAY: WE MEET AGAIN. Yesterday’s action in the 10-year Treasury note yield (TNX—candlesticks) and S&P 500 index (SPX—purple line) was all over the place, but the two met at day’s end. When yields eased following Tuesday morning’s release of inflation data, the SPX rallied in relief. The rally faded when yields made an upward run, but the SPX eventually recovered. Data sources: S&P Dow Jones Indices, Cboe. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Thinking Cap

Turning down cash: There’s some head-scratching around weekly initial jobless claims data. It’s tracked near historic lows under 200,000 so far this year despite a flurry of layoff announcements from info tech. Many investors, and perhaps even the Fed, might wonder why the layoffs haven’t translated into more claims. Here’s one possible reason: Many layoffs were in high-paying sectors and involved mostly white-collar workers. Severance packages may have been generous, leading laid-off workers to delay filing for unemployment benefits because they’re taken care of for now. There’s also anecdotal evidence of companies like Deere (DE) and Caterpillar (CAT) bringing on tech personnel, some of whom might be ones recently laid off from big tech. Consensus for Thursday’s claims report is 200,000, according to Trading Economics.

A healthier consumer in January? We’re still waiting for plenty of last month’s economic data, but the Bank of America Institute just offered new consumer spending numbers for January that might be worth watching. BAC saw its credit and debit card spending per household rise 5.1% year over year in January compared to 2.2% in December. Granted, the pandemic’s Omicron variant dampened January spending a year ago, but the Institute said, “an increase in minimum wages and Social Security may be helping consumers, along with the stellar labor market.” The report also saw good news in month-to-month services spending in January, up 3.5% on airlines and 1.8% in restaurants and bars and added that some consumers may have held on to their wallets until January to get the most out of holiday discounts. Finally, the Institute noted that savings rates have fallen from high pandemic levels, but that they’re still above 2019 levels even after adjusting for inflation, “suggesting (consumers) have not yet reached their financial limits.”

Invisible but industrious: Hear about all the jobs growth at dry cleaners and auto repair shops recently? Probably not, but it’s helping support the labor market. “Employers in industries like health care, education, leisure and hospitality, and other services, such as dry cleaning and automotive repair, account for 36% of all private-sector payrolls,” The Wall Street Journal recently noted. “Together, those service industries added 1.19 million jobs over the past six months, accounting for 63% of all private-sector job gains during that time. By comparison, the tech-heavy information sector, which has shed jobs for two straight months, makes up 2% of all private-sector jobs.” Of course, jobs in daycare and nursing homes don’t pay Amazon (AMZN) and Microsoft (MSFT) salaries, raising questions about the effect on consumer spending if jobs growth remains concentrated in lower-paying sectors.

Notable calendar items

Feb. 16: January Housing Starts and Building Permits, January Producer Price Index (PPI), and expected earnings from Entergy (ETR), Hasbro (HAS), and Hyatt Hotels (H)

Feb. 17: January Import and Export Prices, January Leading Indicators, and expected earnings from Deere (DE)

Feb. 20: Presidents Day (market holiday)

Feb. 21: January Existing Home Sales and expected earnings from Home Depot (HD) and Medtronic (MDT)

Feb. 22: MBA Weekly Mortgage Applications Index and expected earnings from TJX (TJX) and Baidu (BIDU)

Feb. 23: Q4 Gross Domestic Product (GDP) second estimate and expected earnings from Alibaba (BABA) and PG&E (PCE)

Feb. 24: January Personal Consumption Expenditure (PCE) Prices, January Personal Income and Personal Spending, January New Home Sales, and final February University of Michigan Consumer Sentiment

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.