This week’s economic spotlight shines on the highly anticipated release of the Personal Consumption Expenditure (PCE) price index for January, scheduled for Thursday. The significance of this index cannot be overstated, as it serves as the Federal Reserve’s preferred barometer for inflation.

Stock markets are approaching this pivotal event near their all-time highs, as evidenced by the S&P 500, Nasdaq 100, and Dow Jones indices, fueled by a remarkable rally that ignited in late October.

The forthcoming inflation report from the Bureau of Economic Analysis is keenly awaited by investors, given its pivotal influence on shaping the trajectory of interest rate expectations in the near term.

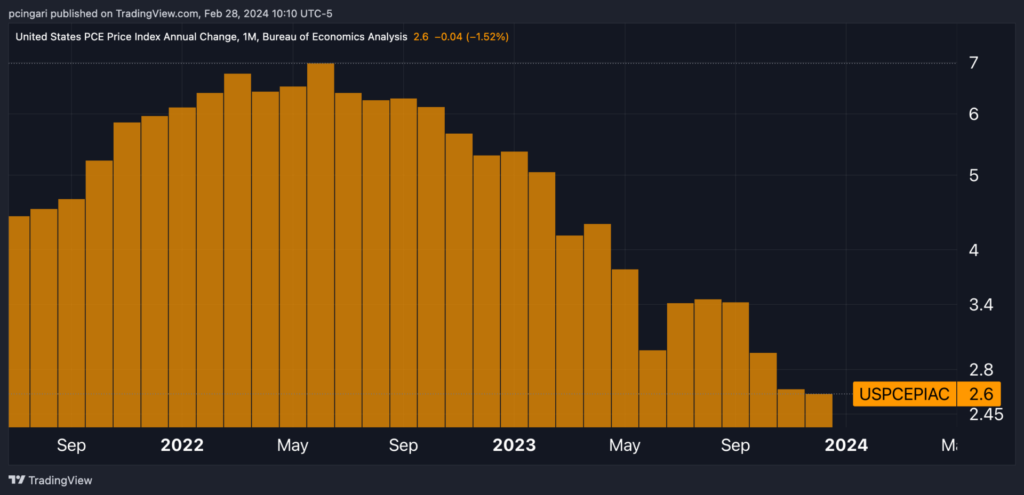

June 2022 saw the PCE reach a four-decade peak of 7%, but it has significantly retreated since, signaling a widespread disinflationary trend within the U.S. economy. In December 2023, the PCE price index rose by 2.6% year-over-year, a rate that remained unchanged from November and matched the lows of February 2021.

However, the journey to the Fed’s 2% target hinges on the data for January 2024 and beyond.

Chart: US Personal Consumption Expenditure Price Index (YoY Change)

January PCE Preview: What Do Economists Expect?

- Economists’ median consensus anticipates the PCE’s annual rate to dip from December 2023’s 2.6% to 2.4% in January 2024. Should these forecasts align with actual figures, it would mark the lowest annual PCE inflation rate since February 2021.

- On a month-to-month basis, the PCE price index is expected to see a 0.3% increase, up from the previous 0.2%.

- Excluding volatile components like energy and food, the core PCE inflation on an annual basis is anticipated to slightly decrease from 2.9% to 2.8% in January 2024, marking its lowest point since March 2021.

- The monthly core PCE price index is projected to rise by 0.4%, accelerating from December’s 0.2% increase.

- Earlier this month, the Consumer Price Index (CPI) inflation for January surprised to the upside, according to data from the Bureau of Labor Statistics. The annual CPI rate declined from 3.4% to 3.1% in January, exceeding the anticipated 2.9%. The core CPI annual rate remained steady at 3.9%, against expectations of a drop to 3.7%.

Potential Market Impacts

Currently, markets are pricing in a 63% chance of a Federal Reserve interest rate cut by June, with the likelihood increasing to 84% for a cut by July. Furthermore, there’s an anticipation of approximately 85 basis points in cumulative interest rate reductions by December 2024, suggesting the market expects slightly more than three 25 basis point cuts.

An unexpectedly high PCE report could decrease the odds of a June rate cut and potentially align market expectations more closely with the Federal Reserve’s projection of three rate cuts in 2024.

Conversely, a PCE report cooler than expected might revive speculation of a Fed rate cut by the end of the first half of the year, with forecasts possibly leaning towards a strategy of four rate cuts in 2024.

In the scenario of a stronger-than-anticipated PCE report, risk assets such as stocks could face pressure.

As the ongoing equity rally has largely been underpinned by the broader economy’s disinflationary trend, the prospect of a more stubborn decline towards the 2% target may prompt investors to reassess their positions, potentially leading to a reduction in their exposure. The SPDR S&P 500 ETF Trust SPY fell 1.4% following the January CPI’s hotter-than-expected surprise.

Following a higher-than-expected PCE report, traders should also brace for potentially hawkish comments from the Fed.

On the flip side, softer-than-expected data could offer equity markets a fresh impetus to retest their recent all-time highs.

Photo: Shutterstock

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.