Thematic Investing

The S&P 500 approaching 5000 is something of a sideshow relative to the themes dominating the price action. The generative artificial intelligence boom garners the most attention, but the industrials sector, with the exception of the transportation & logistics industry, had a really strong quarter at least partially attributable to the renaissance of the US manufacturing and modern supply side economics (industrial policy). On the flip side, the deep inversion of the Treasury curve, which is the equivalent of the Fed dropping dynamite in the ocean, continues to cause ‘idiosyncratic’ whales to float to the surface. As we will discuss later, policymakers, regulators and some market participants are misdiagnosing the problem, it isn’t really about the quality of the assets, but rather the cost of financing them is prohibitive relative to the price they were purchased for. While all that was going on, the Treasury sold record amounts of 3s, 10s and 30s. While each auction appeared to go well, through Thursday’s close, the 5-day change for 2s was +23bp approaching 4.5%, 5s +28bp, 10s +26bp and 30s +23bp. The increase in the short end was split between the breakeven inflation and real rate components, in the long end the increase was almost exclusively real rates perhaps due to a rethink about the terminal policy rate, or more theoretically the natural rate (r*), an issue we are also addressing in this week’s note. Within the last of these four themes, a serious negative correlation has developed between the Treasury market and regional bank stocks, this is because the only plausible path to a March rate cut is an intensification of the regional bank stress. In addition to our analysis of the banking situation and the natural rate, we also cover the outlook for sustainable and broadening disinflation after the CPI revisions ahead of next week’s January report and some significant enhancements to our sector and asset allocation product.

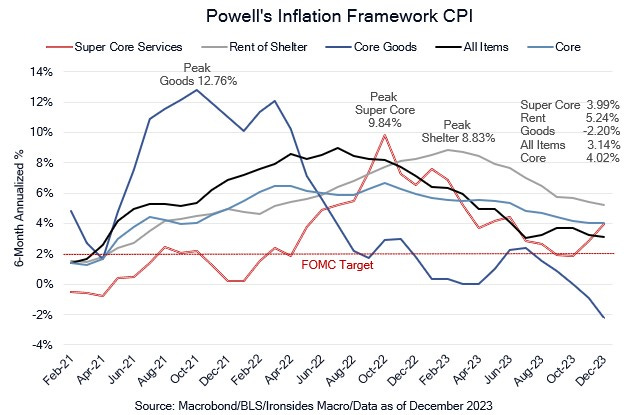

Figure 1: The CPI revisions were trivial for the 6-month annualized rate for all items and core, 3.14% from 3.12% and 4.02% from 3.99%. However, non-housing services was revised to 3.99% from 4.19%, rent of shelter was revised up to 5.24% from 5.08% and core goods deflation from -2.52% to -2.2%. On balance, the disinflation is moderately broader than the initial estimates, but the rent of shelter conundrum persists.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.