This week sees earnings reports from Amazon.com Inc (NASDAQ:AMZN), Alphabet Inc (NASDAQ:GOOGL), Meta Platforms Inc (NASDAQ:META), and Match Group (NASDAQ:MTCH), the owner of Tinder. After a year-end rally that pushed stock valuations higher, the upcoming results might need to be pretty impressive to stir a rather subdued market.

Ahead of these earnings announcements, RBC Capital Markets analysts have highlighted Amazon and Meta as their preferred choices. They are focusing on whether artificial intelligence can keep sparking interest without boosting revenue, how China’s economic slowdown affects the market, and the extent of growth in the Cloud sector.

Delving into the insights of RBC Capital’s analysts, spearheaded by Brad Erickson, he said, “Given how the market has rebounded over the last few months, risk/rewards are more balanced, in our view, but with such strong fundamentals likely on the way, we stay the course on Amazon and Meta.”

Amazon

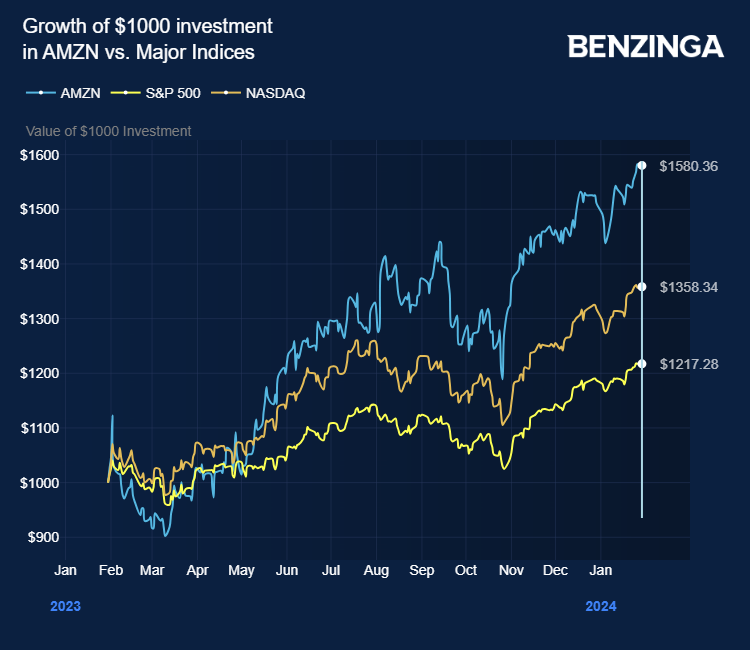

With an outperform rating and a $180 price target — both unchanged here — RBC expects Amazon to beat market expectations of fourth-quarter earnings per shares of 79 cents with year-on-year growth in revenues of 11.4% to $166.2 billion.

RBC is looking for acceleration in Amazon’s AWS cloud offering, saying the “bigger concern is whether Microsoft is gaining more meaningful market share.”

Erickson said: “We'd expect a continued narrative of operational and fulfilment improvements and efficiencies, and we believe expectations to achieve or beat through the year remain reasonable.”

Also Read: AI, Biotech, Energy Sectors Expect M&A Revival For 2024

Meta Platforms

RBC held its outperform rating and $400 price target and expects the Facebook owner to beat market expectations of $2.85 earnings per share, with annual revenue growth of 7% to $30.84 billion for the fourth quarter.

While Chinese e-commerce is a potential headwind, RBC expects that increasing adoption by advertisers of its Advantage+ offering to be a key driver.

Erickson said: “Given the consistent success we've heard with A+ in terms of conversion improvement, we believe this could actually be a potentially bigger tailwind than initial A+ adoption was in 2023.”

Alphabet

With an unchanged rating or outperform and price target of $155, RBC expects a slight earnings miss on expectations of fourth-quarter earnings per share of $1.60, which would be up 52.4% from the same quarter a year ago. RBC expects revenue growth of 12% to $70.7 billion in the quarter.

The main concern of RBC is the impact on margins of the company’s strategic headcount reductions last year. “Bulls are looking for signals of these being more material with more reductions to potentially come in 2024,” said Erickson.

“Setting aside generative AI search concerns, we'd think Google could ‘work’ in 2024 on the combo of upside from YouTube, Cloud, and overall margins,” he added.

Match Group

RBC holds an unchanged outperform rating and price target of $43 on Match Group and anticipates a miss on earnings expectations of 49 cents per share — which would represent growth of 63.3% on the fourth quarter of the previous year. The broker expects revenue growth of 10% to $862 million.

Erickson anticipated that the number of paying Tinder subscribers would present a headwind, but he also noted that Hinge’s strong performance might mitigate some of the negative impact from Tinder.

Now Read: Tesla’s Humanoid Robot ‘Was A Fake,’ Elon Musk ‘Doesn’t Deliver At All,’ Says Analyst

Photo: Shutterstock

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.