The following was originally published in February 2015 on Motif Investing.

There are three main classes in most societies: the poor, the middle class, and the rich. In a recent survey, approximately 40% identify themselves as poor, about 44% label themselves as middle-class, and only about 15% consider themselves to be upper-class or rich. While some lack the necessary resources to become rich, many have the ability, but simply do not purchase assets that have the potential to appreciate in order to eventually make them rich. Instead, money is often spent as soon as it is earned for immediate need or gratification.

The average person might think the rich were born into their money, but studies have shown only 30% of billionaires actually inherited their wealth. Instead, many rich citizens have stemmed from humble middle-class families, and have simply learned what it takes to acquire wealth.

The Difference Between Good Assets And Bad Assets

When one learns basic accounting in college, professors explain that a balance sheet is made up of assets, liabilities, and equity. But, hardly ever is the student taught that there is a dramatic difference between good assets and bad assets, especially in the context of earning money.

In their most basic form, good assets earn a positive cash flow while bad assets end up costing you money (or at the very least constricting your cash flow). As an example, a car, based on accounting principles, is typically a bad asset. Once you buy a car, it tends to start depreciating in value, not to mention it also costs you money in insurance, gas, and maintenance. More importantly, it is unlikely to generate any cash flow, unless you rent it out in one of today’s many car-sharing businesses.

A rental property, however, can be a good asset because if rented to a responsible tenant, it will repeatedly put money in your pocket each month. Other possible examples of good assets are dividend paying stocks, bonds, and businesses because these assets have the potential to earn positive cash flow during the duration of ownership.

What Assets Does Each Class Typically Own

Although the ability to earn money and create wealth is not the same for everybody due to circumstance, America provides one of the greatest platforms for people to move forward. We’ve got a stable government, a working legal system, strong employee rights, and public infrastructure that enables people with enough determination to get ahead.

By their very definition, the poor have a limited ability to purchase assets due to most of their income going toward basic necessities. The difficulty of having to survive on a low income may tempt some to uproot themselves from poverty through get-rich actions like gambling or purchasing lottery tickets. Very few come out ahead this way and a great majority of those already in poverty may unfortunately stay in poverty. It can be a very vicious cycle that requires a confluence of education and time.

The middle-class tend to have jobs that are consistent and pay well from week to week or month to month, which gives them the ability to purchase assets. However, simply having an ability to purchase assets may not result in a sensible investment, especially if buyers spend beyond their means. Examples of waste include buying McMansions, expensive cars on payment plans, and boats. Unfortunately for such spenders, these types of assets aren’t going to earn them money. Instead, these items are likely eating away at their cash flow each month, especially if they are purchased on unfavorable credit terms. Without a healthy cash flow, it is difficult to acquire good assets, which can contribute to keeping the middle-class in their respective societal position for life.

The rich have an entirely different story. Instead of buying bad assets that generate no revenue, the rich have the opportunity to delay gratification and purchase assets that produce income or a higher principal value down the road, perhaps on more favorable terms. This process is repeated again and again, which, in an opportunistic situation can result in their asset income exceeding their work income. The rich may continue to get richer, and it may be because they are making timely investments in the proper assets.

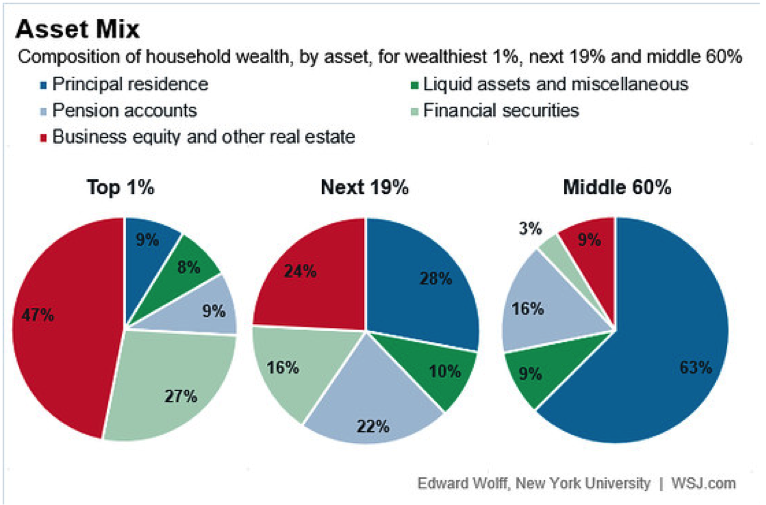

Asset Allocation Variances By Wealth

It is interesting to look at how asset composition varies amongst wealth classes. Notice how large the principal residence weighting is for the Middle 60% compared to the weighting for the Top 1% in the chart below. When the housing downturn hit in 2008-2010, the middle class got crushed in part because they lacked the diversification of income from good assets to be able to compensate for their short-term expenses.

How can the Middle 60% try to reduce their principal residence exposure to get more inline with the Next 19% and Top 1%? One possibility is purchasing smaller, more affordable homes to free up more funds for investing in financial securities. Another significantly lower weighted asset class for the Middle 60% is business equity and other real estate. This is likely a challenging category for the Middle 60% to expand due to greater difficulties obtaining loans to launch a company, buy a rental property, and come up with cash necessary to invest in private equity. Paying down debt to improve their debt to income ratio can help with their ability to be flexible with taking advantage of opportunities that arise, such as qualifying for a loan to acquire a rental property or new business endeavor.

Source: Wall Street Journal

The Process Of Becoming Rich

Discipline is a key word in becoming rich. There are countless examples of people making millions of dollars and ending up broke due to a lack of discipline. The temptation to spend is ubiquitous to the point of complete exhaustion. In order to start down the road to riches, consider some common examples from those who have already met their goal:

Motif Investing offers flexible investment products and services to prepare you for retirement and help you build your wealth. Select motifs that suit your investment needs and let Motif Investing help you achieve your financial goals.

- Maxing out your 401k and IRA.

- Saving an additional 20% or more of your after-retirement, after-tax income.

- Invest your additional savings in a portfolio of stocks and bonds appropriate to your risk tolerance and financial objectives.

- Accumulate real assets, such as real estate property, to further diversify your net worth

- Track your net worth so you know where your money is going.

- Do not let your spending increase faster than the rate of your income growth.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.