A more dovish Federal Reserve tried to end July on a positive note than it had during previous rate decisions, helping extend the S&P 500® index (SPX) rally that began in June. However, inflation, the Fed’s greatest enemy, has yet to let up, much like the Russia-Ukraine war that sparked higher energy prices around the world and likely threatens more disruption in the coming months.

So, is August shaping up to be more of the same—or will the bulls finally charge?

Recession Debates

A big problem the bulls face is one of the strangest debates about recession in recent memory. U.S. gross domestic product (GDP) was down 0.9% in the second quarter, at least at the first print, which will likely be adjusted as complete data comes in. While this was better than what the Federal Reserve Bank of Atlanta’s GDPNow tool had projected at -1.6%, it made for two consecutive quarters of negative GDP, which many consider to be a recession.

However, the National Bureau of Economic Research, which gets the official say, considers whether an economic contraction is “prolonged, pronounced, and pervasive” as it deliberates. Because the labor market is still quite strong with the U.S. unemployment rate at 3.6% in June and with the economy still shifting from products to services in the third year of the pandemic, those arguing against the traditional “recession” label may have strong footing.

Whatever we’re willing to call the current state of the economy, July’s numbers indicate that it does appear to be weakening at a much faster pace than people expected. The latest GDP report showed that gross domestic purchases fell from Q1 to Q2 as consumers were spending more on services and less on goods.

But that’s not the only recession debate going on, and that’s whether the Unites States will be in a recession by this time next year. Currently, the market is projecting that the Fed will be cutting interest rates by July 2023—another way of saying that not long after the Fed finishes raising rates, recession may be the real catalyst for cutting them.

And then there’s what’s happening in the bond market. The yield curve, as measured by the 2s10s ratio, has become increasingly inverted, reaching levels we saw in 2006 just months before the Great Recession. Many investors see an inverted yield curve as a reliable indicator of recession because investors favor lower-paying bonds with higher maturities, not only for their safety but for anticipated rate cuts that will push bond prices higher.

The recession debate doesn’t stop at the U.S. border. On July 22, preliminary manufacturing PMI results for Australia, France, Germany, and Japan showed recession-level contractions in each country’s manufacturing sectors. Also, the International Monetary Fund’s “World Economic Outlook Update July 2022” described the global economic situation as “gloomy and more uncertain.”

The International Monetary Fund cited inflation, tighter monetary policies, ongoing lockdowns, a real estate crisis in China, and continuing spillover from the Russia-Ukraine war as reasons for the dour outlook.

Battle over Natural Gas

Speaking of the Russia-Ukraine war, the conflict has spun off a battle over natural gas between Russia and the European Union (EU). On July 20, the European Commission asked its 27 member nations to reduce their natural gas consumption by 15% between August and March 2023 in response to Russian energy giant Gazprom saying it cannot fulfill gas contracts with the EU.

Russia appears to be striking back against EU war sanctions by tightening gas exports. The commission said that Russian President Vladimir Putin is “blackmailing” EU members and “using energy as a weapon.”

On July 27, the EU nations agreed to restrict their gas consumption, and Gazprom responded that it plans to cut capacity of its Nord Stream 1 pipeline to Germany from 40% of capacity to just 20% due to a “turbine” problem.

The battle over natural gas has caused a lot of volatility in the futures market. U.S. natural gas prices have risen as much as 80% in July in response to the turmoil. However, the U.S. price for natural gas pales in comparison to Europe where Europeans are paying nine times what Americans are.

Earnings’ Early Returns

Higher natural gas and oil prices have also had an effect on Q2 corporate earnings. According to Refinitiv, of all the S&P 500 companies reporting so far, about 75% are beating analysts’ estimates, above the long-term average of 66% but lower than the previous four-quarter average of 80.6%. S&P 500 companies are on track for 6.2% year-over-year (YOY) earnings growth. However, when excluding energy, growth falls to -3.2%.

The energy sector has the highest earnings growth rate at a whopping 259.6% YOY. Industrials are second at 26%, and financials are the worst at -22.1%.

FactSet has found that S&P 500 companies are still reporting fewer and smaller earnings surprises compared to the last five-year average. The financials and communications sectors have had the greatest number of earnings misses. Utilities and health care have reported the highest number of earnings beats, while energy and industrials have reported the lowest. However, energy and industrials are also reporting a high number of earnings that are in line with analyst estimates.

With that said, during the last week of July, investors appeared to have changed their view on earnings as they brushed off bad reports from Microsoft (MSFT) and Alphabet (GOOGL) and chose to buy up the companies anyway.

Strong Dollar No Longer?

One more reason for the positivity could be that investors are expecting the Fed to slow future interest rate hikes, which should weaken the dollar. The strong dollar has been a drag on earnings for many multinational companies as they try to repatriate those earnings into dollars, finding the exchange rate is costing them. In fact, research from Morgan Stanley (MS) determined that on a year-over-year basis, every percentage point gain in the dollar results in about a half-point hit to earnings on the S&P 500.

A more dovish Fed might help weaken the dollar. In July, the Federal Open Market Committee (FOMC) announced that it would raise the overnight rate by 75 basis points, in line with market expectations, but the Fed’s commentary around the decision expressed concern over the economy, which the markets appeared to view as signs the rate hikes were near the end. Higher rates tend to strengthen the dollar so the end of the rate hikes could cause the dollar to weaken some.

During the post-announcement press conference, Fed Chairman Jerome Powell said that the Fed’s June dot plot was still relevant and had showed the overnight rate topping out around 3.5% by the end of the year. If this is the case, then the September FOMC hike would likely be around 50 basis points and then 25-basis-point hikes would likely occur in November and December.

The stock market rallied big on the Fed’s change in tone and the dollar traded lower. However, Powell did warn that the central bank remains data-driven, and inflation surprises have occurred. This will likely make the July CPI report that comes out August 10 a pivotal data point for many investors.

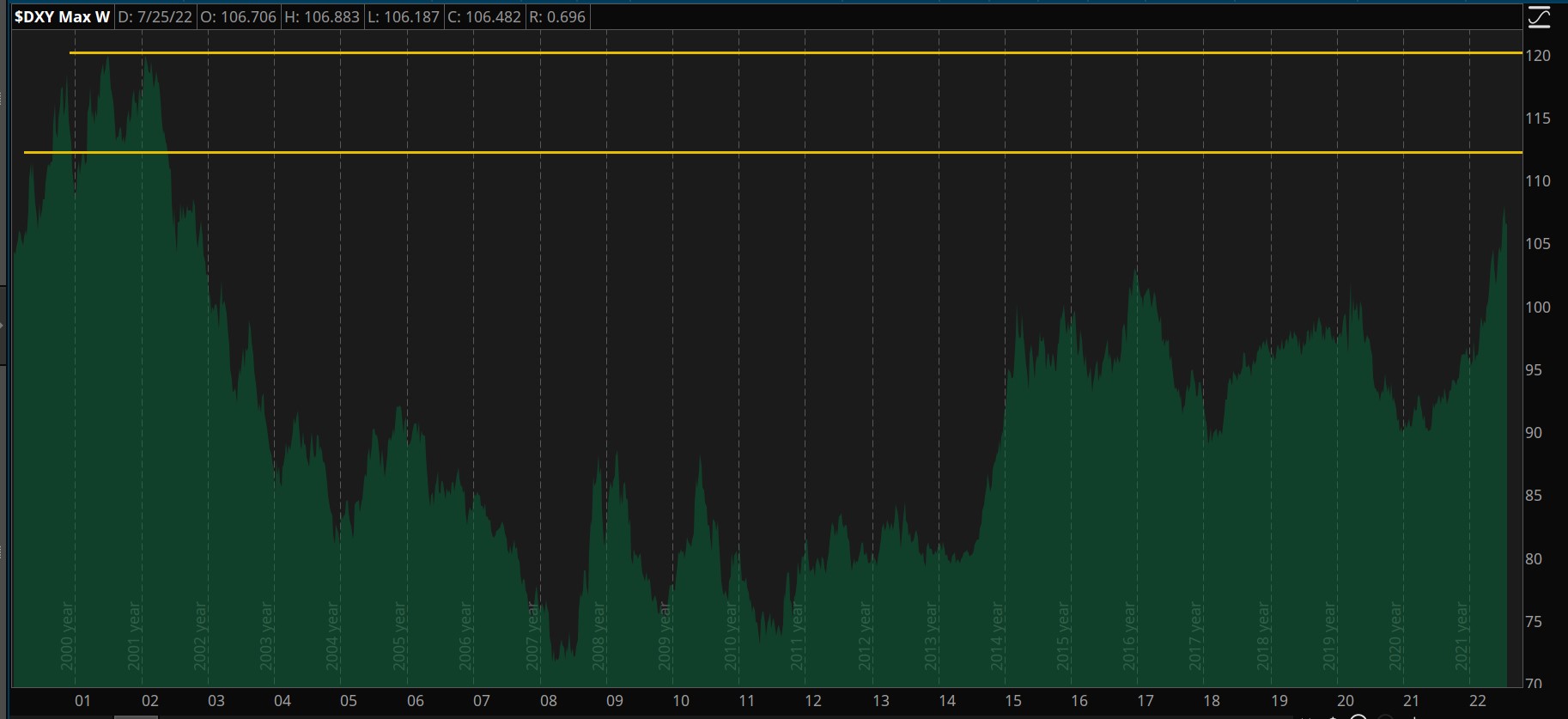

Figure 1: GREEN IS BACK. The U.S. Dollar Index ($XY—green) is trading at 2002 levels and has some room for growth before reaching late 2001 lows or 2002 highs. If the dollar returns to these levels, it could be because inflation isn’t slowing at the pace the Fed had hoped so it is continuing to raise rates. It could also mean that foreign investors are buying dollars due to global recession or turmoil. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Are Rate Hikes Working?

Higher interest rates are meant to slow economic growth by incentivizing people to save money instead of spending it. The change in consumer behavior generally lowers demand for goods and services, and that brings prices down. After the rate announcement, Powell said the FOMC sees slower sales in housing and automobiles as well as an uptick in unemployment but added that it could be seasonal.

However, recent CPI reports haven’t indicated any signs that inflation is waning and the PCE Price Index, which is the inflation report the Fed favors most, came out the last trading day of July and was hotter than expected. Mastercard (MA) said in its July 27 earnings report that the consumer remains strong because it hasn’t seen any signs of slowing in the level of spending. This makes it difficult to say so far rate hikes are working to slow inflation.

However, Walmart (WMT) and other retailers have warned investors that their apparel business has slowed with inventory buildups that would have to be sold at a discount. This at least one area that should be deflationary instead of inflationary.

The Fed’s hope is to slow inflation without sending the economy into a recession—an incredibly difficult feat. In the past, Fed members have expressed hope that as the country reopened from the pandemic, there would be less consumption of goods and more consumption of services. This could help prices of goods to come down.

The Fed still needs strong consumers to avoid going into a recession, but there’s no way for the Fed to direct consumers on what to buy. That’s just one more example of how difficult it is to slow inflation without causing recession.

The Next Shoe?

Critics of the Federal Reserve often point out that the Fed tends to create asset bubbles when it lowers rates and pops those bubbles when it raises them. While many would likely debate whether stocks or housing were or are in bubbles, the bursting of an asset bubble is commonly a precursor of deflation.

Meanwhile, stocks are already in a bear market, so the question may be, “Is the housing market the next shoe to drop?”

According to the June S&P Case-Shiller Housing Index, the “pandemic housing boom” pushed U.S. home prices up 42% in the last two years. But after experiencing a bear market in stocks through the first half of 2022, investors are becoming increasingly nervous about the housing market and the data is concerning.

- The June data that came out in July was particularly weak:

- The National Association of Home Builders reported that building permits fell 0.6% in June, the biggest drop ever recorded for that month.

- June new home sales fell 8.1%, according to the U.S. Department of Commerce, and are approaching 2020 pandemic lows ahead of the boom.

- The Mortgage Bankers Association (MBA) reported mortgage applications fell 6.3% the third week of July. Demand for mortgages is at its lowest level in over 20 years.

- The National Association of Realtors reported that existing home sales came in worse than expected in July, falling for the sixth week in a row.

Redfin (RDFN) reported that homes are taking longer to sell. The company said interest in homes has waned. Google searches of “homes for sale” fell 23% YOY by mid-July. The Redfin Homebuyer Demand Index, which measures such factors as requests for showings, was down 17% from a year ago.

A big problem for the housing market is that mortgage rates have gone up so much. On July 20, the MBA reported that the average 30-year mortgage rate was 5.82%. By comparison, the rate hit its all-time low in December 2020 at 2.85%. Today the rate is at 2008 levels, just before the credit crisis and Great Recession.

While the news for housing doesn’t look good, it certainly isn’t in a bear market, at least not yet. In June, existing home prices were still up 13.4% YOY, and sellers were averaging just two weeks to find a buyer.

The June S&P Case-Shiller Housing Index rose 1.3% and was up 18.3% YOY. Redfin had similar data, reporting that median home sales were still up 11% YOY in June and the median asking price for newly listed homes was up 14% YOY, although down 2.8% from its all-time high set back in May.

The housing market is obviously slowing and often a change in momentum signals a shift in direction, but that doesn’t mean the housing market will slide like it did back in 2008. Housing is likely to go through a price discovery process because interest rates will continue to affect demand for homes.

When it comes to mortgages as well as other loans, banks have been shoring up their balance sheets by raising loan loss provisions throughout their consumer and corporate businesses. This is money set aside in case of loan defaults. In Q1, the 18 banks in the S&P 500 set aside $1.4 billion for losses. FactSet projected that the number would grow to $4.5 billion in Q2.

While the final numbers aren’t in yet, Q2 bank earnings zeroed in on their reserves. The nation’s largest bank, JPMorgan Chase (JPM), said it set aside $1.1 billion in the quarter while Goldman Sachs (GS) provided $667 million for loss provisions, Wells Fargo (WFC) reserved $580 million, Bank of America (BAC) put aside $500 million, and U.S. Bank (USB) and Morgan Stanley (MS) reported reserves of $311 million and $101 million respectively.

However, banks usually have rules on how much money they set aside for potential losses that depend on the number of loans they’re carrying. None of these banks reported any increase in delinquencies or defaults on any types of loans. So, while the banks may be increasing loan provisions in preparation for a potential downturn in housing, they haven’t reported any concerns yet.

Conclusion

It’s difficult to predict where stocks could go in August because of so many unique global obstacles in the way. This is why timing the market can be so difficult. Often, the best approach is to remain invested in a diversified portfolio of stocks and bonds that meet your long-term goals and risk tolerance.

It’s important to stay informed. But unless you’re a short-term trader, it’s best not to get caught up in the day-to-day market gyrations that could keep you out of the markets.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.