This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

In addition to private companies refusing to buy Russian oil, U.S. Secretary of State Antony Blinken said the United States and European allies were considering a ban on Russian oil. Previously, these groups have avoided bans on Russian commodities because of how these embargos could hurt consumers already struggling under the weight of pandemic-related inflation.

Government officials are hoping that reduced sanctions on Iran and Venezuela will get more oil supplies to market and help alleviate some of the price pressures. Additionally, Republicans are pressuring President Joe Biden to repeal some of his executive orders signed when he first came into office. These orders banned some offshore drilling as well as some drilling on public lands.

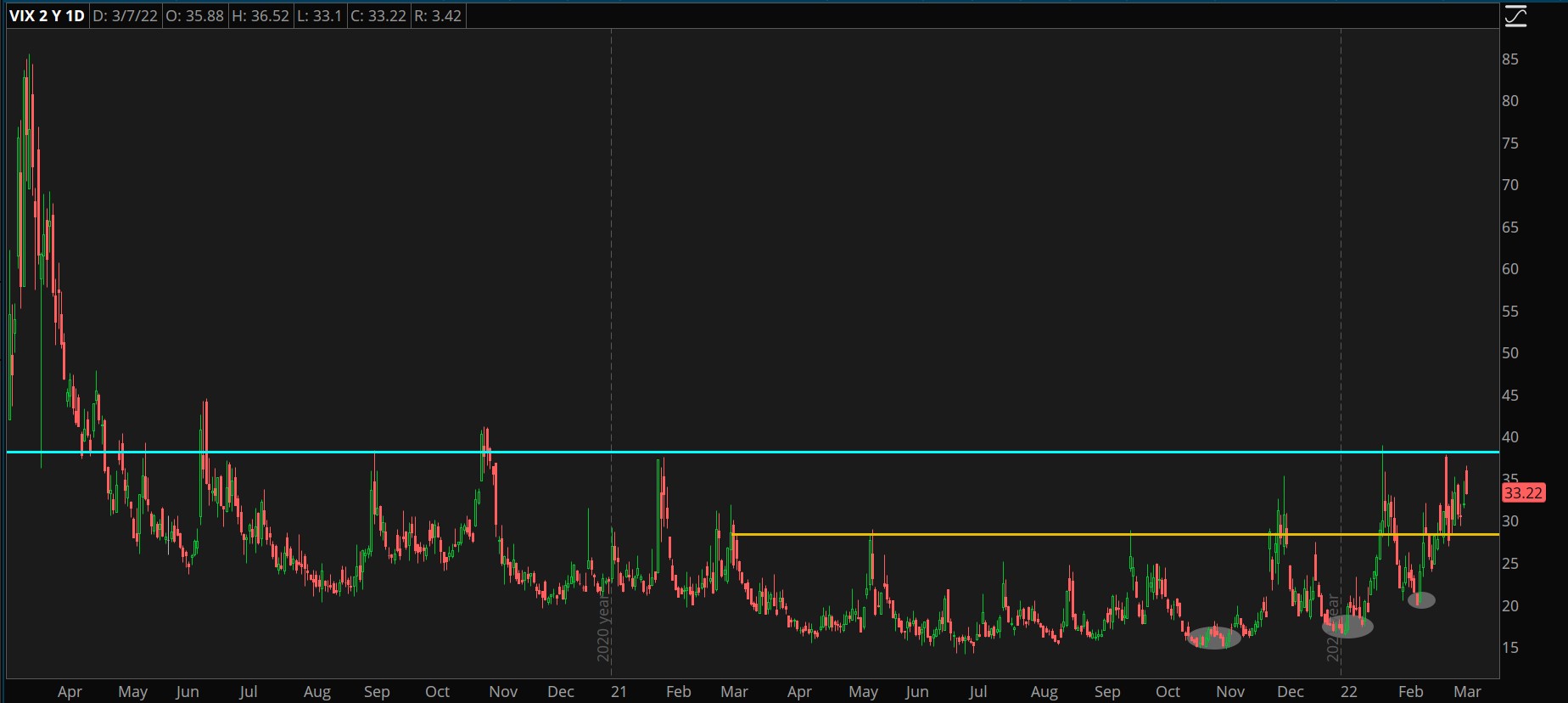

Ukraine continues to struggle as it fights back against the Russian invasion. Ukrainian President Volodymyr Zelensky is asking the Western allies to help by enforcing a no-fly zone over Ukraine. However, the allies have been unwilling to get directly involved in the conflict out of fear of escalation. The Cboe Market Volatility Index (VIX) spiked above 36 this morning and may not retreat without major improvement in Ukraine.

Interest in Rates

Also, Uber (NYSE:UBER) rose about 3% in premarket trading after the company adjusted its first quarter outlook. The company reported a faster-than-expected rebound from the Omicron-related slowdown and is now seeing a “significant” demand in rides.

Friday’s Action

Today’s strong sectors were energy, utilities, real estate, health care, and consumer staples. Weaker sectors were financials, information technology, and consumer discretionary.

The United States added 678,000 new jobs to the economy in February, and the unemployment rate fell to 3.8%. These were some great numbers compared to the expectation of 440,000 jobs and 3.9% on the jobless rate. This report confirms that the rampant Omicron variant spread during the winter had little impact and shows a big decrease from last February’s 6.2 % rate. In February 2020, prior to the coronavirus pandemic, the unemployment rate was 3.5%.

Increasing Geopolitical Risk

Earnings Update: According to Refinitiv, thus far, 493 companies in the S&P 500 have reported earnings with 76.5% beating analysts estimates. This is higher than the historical average of 65.9% but lower than the previous four-quarter average of 83.9%. The year-over-year earnings are on track for a 32% increase, but the energy sector continues to carry earnings. When energy is removed from the numbers, the growth is 23.4%.

FactSet is reporting that the S&P 500 has an estimated earnings growth rate of 4.8% for the quarter which is the lowest quarter since Q4 2020. Earnings estimates for the S&P 500 in Q1 have fallen 1.2% with eight of the 11 sectors decreasing forecasts. Only energy, real estate, and technology are expecting increases. Inflation concerns could continue to cut into these earnings estimates unless some relief is provided soon.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Pixabay

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.