This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

(Monday Market Open) Over the weekend, President Vladimir Putin put Russia’s nuclear forces on high alert as Ukraine sees increased military support from the North Atlantic Treaty Organization (NATO). Russia is also experiencing increased sanctions as a growing number of countries are blocking Russian banks and businesses from using the Society for Worldwide Interbank Financial Telecommunications (SWIFT), which makes it difficult for Russian companies to do business with foreign entities. However, according to Briefing.com, companies that deal in energy are not being removed.

Russia closed its stock market today after seeing large selling last week. The MOEX Russia Index lost about 1,000 points last week—nearly 30% of its value. Russian stocks aren’t the only things falling; the ruble fell hard last week too, causing the Bank of Russia to raise rates from 9.5% to 20% in an attempt to support the currency.

Russian and Ukrainian officials are meeting at the Belarus border today to start peace talks. Ukrainian President Volodymyr Zelensky said the next 24 hours would be crucial for the future of Ukraine. President Zelensky is looking for an immediate ceasefire and withdrawal of troops, but it’s difficult to project what might happen.

Crude oil futures were up big overnight in response to the developments between Russia and Ukraine, jumping more than 9%. However, they were well off their highs before the market open, trading 4.18% higher. As expected, the turmoil has heightened investor concern; the Cboe Market Volatility Index (VIX) rose nearly 18% before the open. The S&P 500 futures were down about 3% overnight but had cut those losses in half before the opening bell.

While Russia is causing a lot of concern for American investors, it’s another item on a long list of concerns that includes inflation and interest rates. This week, Fed Chair Jerome Powell will testify before Congress and will likely see pressure to reveal the Fed’s plans to curb faster-than-expected inflation.

Along with listening to Chairman Powell, investors will get several reports concerning the labor market this week. The big Employment Situation report comes out on Friday. The hot labor market is an area of strength for the United States economy and allows the Fed to be more aggressive in addressing inflation if they choose.

Looking more specifically at stocks, CEO of Berkshire Hathaway (BRK/A) and one of the richest people in the world, Warren Buffett, released his annual shareholder letter. In the letter, Mr. Buffett said he’s not finding good places to invest money because of poor long-term prospects.

Friday’s Action

Last week’s trading had more jumps and turns than a Russian ballet and ended a tragic week that included the bombing of Ukrainian facilities and cities with a surprising come back on Thursday and a rally on Friday. The Dow Jones Industrial Average ($DJI) saw the biggest gains, closing 2.51% higher on Friday. The S&P 500 (SPX) rallied 2.24%. And the Nasdaq Composite ($COMP) that led Thursday’s rally rose 1.64% on Friday.

Investors appeared to be satisfied with the response given by the North Atlantic Treaty Organization (NATO) had against Russia invading Ukraine because they weren’t afraid to hold positions through the weekend. The United States and NATO outlined a number of sanctions on Russian banks and elites but made sure to not hinder Russian commodities from going to market. While there’s a lot of uncertainty of what Russia may do next, investors appear to think that Russian President Vladimir Putin isn’t going to push much further into Ukraine.

The Cboe Market Volatility Index (VIX) dropped more than 9% as investors became less concerned about Russia and more willing to do some bargain hunting. Some investors left their safe havens by selling bonds, which pushed the 10-year Treasury yield (TNX) higher, and selling gold futures, causing it fall 1.86%.

Sector Cross Section

Every sector finished in the green on Friday with materials, consumer staples, and financials at the top. However, real estate was the week’s top-performing sector followed by health care. Utilities just barely edged out technology for third place. Seeing real estate, utilities, and technology lead the week, although a shortened week, suggests investors are expecting a more subdued Fed in the March meeting. In other words, investors are likely feeling more confident that the Fed will hike rates just a quarter of a percent.

Real estate could benefit from slower rate hikes because financing costs should remain relatively low for a longer time. Utilities offer high dividends that tend to compete with bond yields so a slower rise in yields will likely favor higher yield dividends. Finally, technology stocks have been hurt by the expectation of rising interest rates because of the role interest rates play in stock valuations.

While these one-week trends are interesting, if the February Consumer Price Index (CPI) is higher than anticipate on March 10, then interest rate sentiment may change. Or, if St. Louis Fed President James Bullard is more influential than expected, a nasty shock could come to these sectors. The month of February has been a testament to how quickly the market can change.

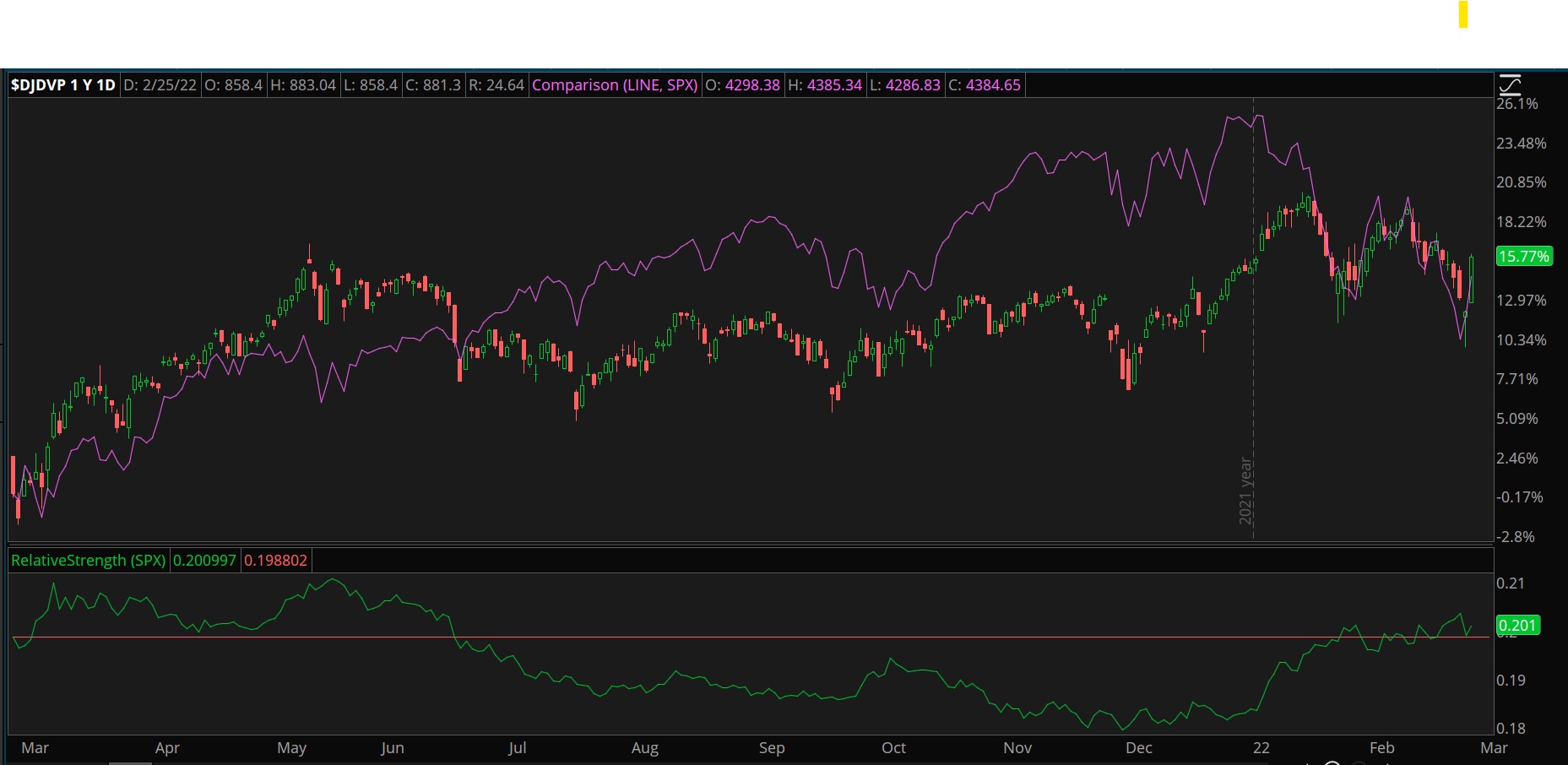

CHART OF THE DAY: DIVIDEND DIVIDE. The Dow Jones U.S. Select Dividend Index ($DJDVP—left) underperformed the S&P 500 (SPX—pink) most of 2021 but has exhibited relative strength (green) against the S&P 500 so far in 2022. Data Sources: ICE, S&P Dow Jones Indices. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Odd Man Out: Often the debate between growth investing and value investing ignores another important style, which is income investing. Investors tend to think of bonds when they think of income, but stocks that pay dividends or higher-than-average dividends are often attractive investment choices. Dividends just aren’t sexy. They only seem to matter when interest rates are rising, and investors are forced to re-evaluate stock valuations. The income investing strategy is rarely a market leader except during bear markets.

With that said, income can be a stabilizing influence on a portfolio and can help reduce volatility. While retirees are more often concerned about stability and income, dividends can be easily reinvested to buy more shares and create compounding interest. Many companies understand the importance of dividends and work really hard to consistently pay and raise their dividends each year. In fact, they’ll often work hard to remain on lists like the Dividend Aristocrats.

While stocks for income may not be appropriate for all portfolios, stocks for growth and income can usually find a place in most portfolios. These types of stocks may not have really big dividend yields and adding a dividend may reduce some of the growth potential, but they can provide a balance that allows investors to share in earnings and company growth.

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Flickr

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.